Cobalt supply chain: China and DRC to maintain dominance, growth potential in Australia– report

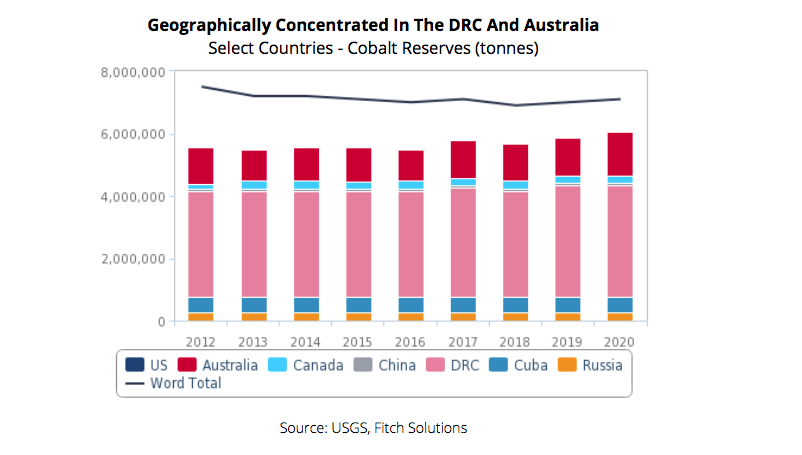

The global cobalt supply chain is set to remain highly geographically concentrated in the coming years — in the DRC for mine production and China for refining — which will likely pose procurement challenges for battery manufacturers, market analyst Fitch Solutions finds in its latest industry report.

However, there is currently a solid global project pipeline, due to the rise in cobalt prices and the expected demand boom amidst the proliferation of battery manufacturing projects, which will aim to diversify to some extent production channels, Fitch says.

The global cobalt industry is set to receive a significant boost from the worldwide shift to a green economy, as the ferromagnetic blue metal is a key component of rechargeable batteries and valued for its stability, hardness, anti-corrosion and high-temperature resistance characteristics.

Used historically as a pigment, due to its luminous blue colour, the metal’s main use today is in the precursors and cathodes of rechargeable batteries (56% of total consumption as of 2021). Employing cobalt as the cathode of rechargeable batteries efficiently improves their energy density, power, and performance as compared to batteries that lack cobalt, Fitch notes.

The end use of cobalt is primarily in portable electronics (36.3% of global consumption), such as smartphones and laptops, while automotive applications also account for a major share (23%) and Fitch expects the latter to drive cobalt demand in the coming decades.

Cobalt refining is also highly concentrated in a single country, China, which will broadly remain the case, Fitch reports, noting there are new cobalt refining projects underway globally which will work to reduce China’s market share to a limited extent.

China accounts for 66% of global refined cobalt output, followed by Finland (10%). Both countries rely on imported feedstock from the DRC for their refining operations. Global production of refined cobalt totalled 132kt in 2020, down 5% from 2019 levels. Cobalt recycling (mainly from the recycling of batteries) is also a fast-growing and important source of cobalt feedstock to the supply chain.

In Fitch’s view, the main impediments to a smooth supply chain dynamic for cobalt is the lack of transparency in the cobalt market, and limited refining capacity outside China, which will continue to pose challenges for a time to come even if actual global supply is sufficient.

Australia holds significant growth potential in the cobalt producing landscape with multiple integrated cobalt projects in the pipeline. Fitch sees limited production growth in Europe and North America in the coming years due to the lack of resources and projects.

Cobalt refining is also highly concentrated in a single country, China, which will broadly remain the case, Fitch says, while noting are new cobalt refining projects underway globally which will work to reduce China’s market share to a limited extent.

The cobalt supply chain is increasingly mired with ongoing concerns over environmental, social and governance (ESG) risks. In recent years, battery makers have strived to reduce the cobalt content in batteries due to supply issues and ESG concerns, instead using nickel-rich cathode chemistries. In late 2020, Tesla also announced that it would move to a cobalt-free battery, although no time frame was given.

Despite these issues, Fitch says, substitution for cobalt could result in a loss in product performance or an increase in cost, both of which will continue to bolster cobalt demand, prices and thus supply.

(Read the full report here)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments