Graphite’s dominance of anode market likely to continue in the mid-term – report

A recent report by IDTechEx forecasts that graphite will remain the most widely used anode material in lithium-ion batteries through the medium term with demand growing considerably and exceeding 2 million tonnes by 2029.

The market analyst explains that two broad types of graphite are used for Li-ion anodes, natural and synthetic (or artificial), each with its own advantages and disadvantages. Natural graphite is generally a lower-cost option than synthetic. It can also offer a slightly higher initial capacity but also tends to have a lower cycle life, C-rate capability, and initial coulombic efficiency.

In contrast, synthetic graphite is more expensive than natural graphite due to the higher energy requirements for graphitization, as well as being more difficult to mill into spherical particles, but it also tends to offer longer cycle life and marginally higher initial coulombic efficiency.

IDTechEx notes that there can be an overlap in the performance and cost of these two types of graphite, and the differences between them have also been closing. Beyond just the type of graphite, various cell design factors such as cathode choice, electrolyte additives, coatings, particle size and distribution, electrode balance, as well as the specification and quality of the graphite product will have a significant impact on eventual cell performance, cost, and cycle life.

“Both synthetic and natural graphite continue to be used with blends widely utilized. IDTechEx estimates that there is a roughly even split, by kt sales, between synthetic graphite and natural graphite. However, there has been a slight shift toward natural graphite over the past few years due to cost pressures and high energy prices,” the report reads.

Despite this shift, the firm’s data show that increasing the output of natural graphite to keep up with the rapidly growing demand for Li-ion batteries has proven challenging.

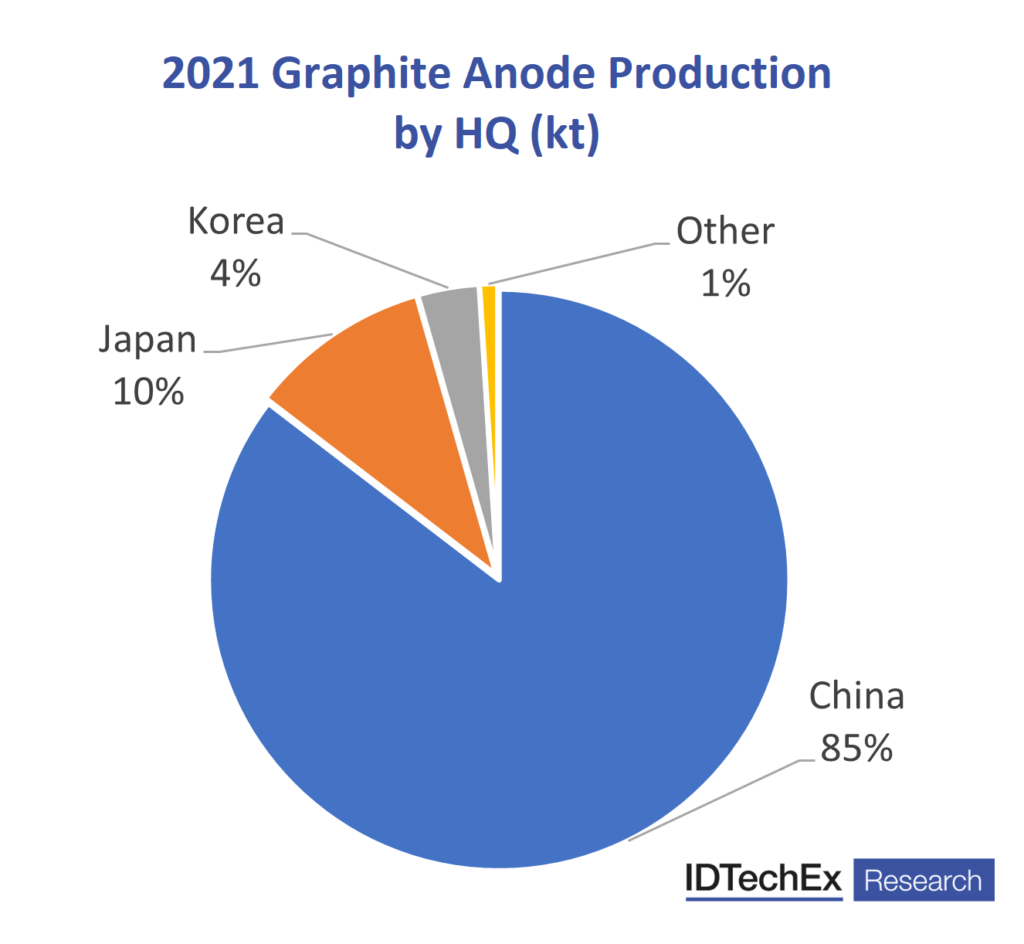

“The US DoE and the European Commission have included natural graphite in their latest critical raw materials/minerals lists due in part to Li-ion batteries’ important role in transport electrification and stationary storage applications. China’s dominance of graphite anode production also presents a supply risk, though Li-ion graphite anode production outside of China is starting to develop from players such as Syrah Resources, Northern Graphite, and Nouveau Monde in North America, or Talga Resources, SGL Carbon and Vianode (synthetic) in Europe, amongst others,” the dossier states.

In IDTechEx’s view, in addition to diversifying material supply, improved sustainability and ESG metrics will be important factors for new graphite production.

“Lower energy consumption and embedded emissions will become an increasingly important metric. This is especially true in Europe, with the European Battery Regulation set to implement carbon footprint labels and declarations for Li-ion batteries above 2 kWh in size. This may favour natural graphite and its lower energy consumption, though particulate emissions and acid waste streams from the purification process also need to be carefully managed,” the document points out.

For the market researcher, lower cost and low carbon energy from renewable sources could help improve the competitiveness of synthetic graphite in this respect, though it will still be reliant on fossil feedstock.

“Ultimately, the dynamic Li-ion graphite anode market and high growth rate in Li-ion demand will ensure ongoing demand for both synthetic and natural graphite anode materials,” the report concludes.

More News

Congo plans first stock market as AI mineral boom draws interest

July 02, 2026 | 06:49 am

Agnico Eagle suspends Quebec pit mining, flags production hit

July 02, 2026 | 06:29 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments