US copper tariffs less likely after critical minerals decision: Macquarie

US tariffs on copper look increasingly unlikely after Washington opted to prioritize supply negotiations over trade penalties for processed critical minerals, Macquarie said, a stance that could eventually unwind stockpiles built on fears of import restrictions.

Earlier this month, the White House concluded a Section 232 investigation into imports of processed critical minerals and their derivative products by directing the Commerce Department to pursue supply agreements, while keeping tariffs as a future option if talks fail.

This decision, according to Macquarie commodities strategists led by Alice Fox, “significantly weakens the case for copper tariffs,” although it cannot be ruled out entirely.

For the time being, the US is likely to maintain “status quo” and postpone its decision on copper tariffs, the analysts wrote in a note published last week.

Cautionary signal

While copper is subject to its own Section 232 review, Macquarie said the fallout from the broader critical minerals decision — and its impact on silver markets — offers a cautionary signal.

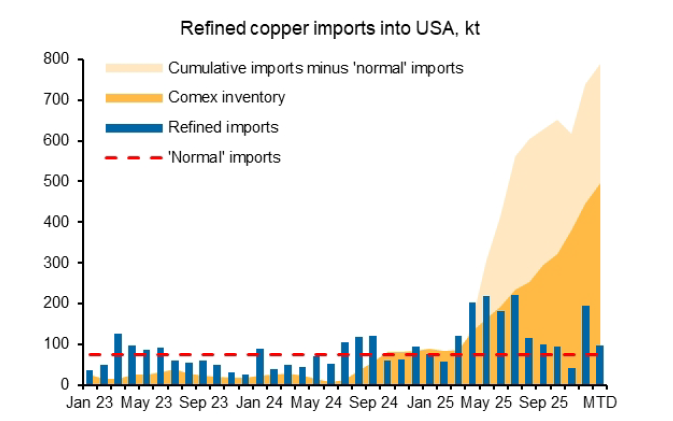

Last year, concerns over potential US tariffs led to a sharp build in Comex silver inventories, tightening liquidity on the London Bullion Market Association (LBMA) and pushing lease rates sharply higher. That dislocation drove metal flows from New York to London as price arbitrage between exchanges reversed.

A similar dynamic is emerging in copper, Macquarie noted. Comex copper inventories have risen by about 412,000 tonnes since December 2024, with an estimated additional 375,000 tonnes held off-exchange. At the same time, the CME-LME arbitrage for January through March has fallen to zero or turned negative, reducing incentives for further US-bound arbitrage trades in the first quarter.

Instead, the negative arbitrage has begun to draw metal out of US warehouses, with London Metal Exchange stocks in New Orleans and Baltimore rising by 8,700 tonnes in the past week. Elevated premiums in Europe are also attracting contract metal that had been scheduled for delivery to the US, the Macquarie strategists said.

While copper already held in the US is not yet sufficiently incentivized to be re-exported, those stocks could become available if markets outside China tighten, as occurred in silver, the bank added.

Supply agreements

Despite minimal progress on rebuilding the US domestic copper production, Macquarie pointed to improvements in supply security through recent international agreements, such as the joint venture between the Democratic Republic and trading house Mercuria being backed by the US International Development Finance Corporation.

Under that deal, US end-users will have rights of first refusal on output, with Mercuria estimating annual sales of about 500,000 tonnes of copper and 40,000 tonnes of cobalt — equivalent to nearly 70% of US net refined copper imports in 2024.

Macquarie’s strategists concluded that the US could still delay a final tariff decision until the end of the year while negotiations continue, a scenario that would preserve the current market structure, with imports diverted and US-held stocks effectively sidelined.

However, if tariffs are ultimately ruled out, the copper arbitrage trade would likely reverse, releasing accumulated US inventories back into the market and potentially triggering a sharp correction in prices, they added.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments