Vale after NYC real estate moguls for Simandou compensation

Brazil’s Vale (NYSE: VALE), the world’s no. 1 iron ore miner, has launched a legal action in New York to determine whether funds paid to BSG Resources within the framework of their former Simandou partnership in Guinea were used for property investments in the United States.

The Rio de Janeiro-based mining giant alleges that BSGR, diamond tycoon Beny Steinmetz’s mining arm, fraudulently funneled $500 million into Manhattan real estate’s magnates Aby Rosen and René Benko, Africa Intelligence reported.

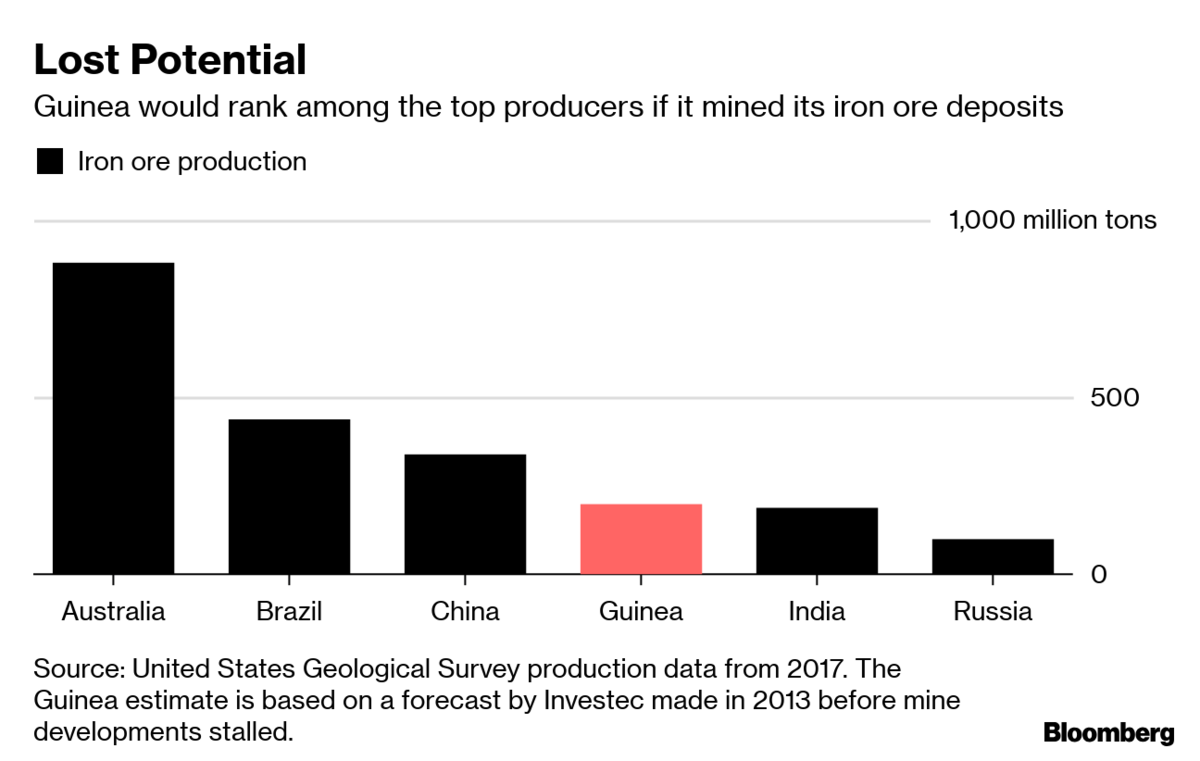

At two billion tonnes with some of the highest grades in the industry, Simandou is one of the world’s biggest and richest reserves of iron ore.

The case is the latest in a series of efforts Vale has made to have BSGR pay a $2 billion arbitration award. The amount was granted to the Brazilian miner on the grounds of “fraud and breaches of warranty” when included in the Simandou iron ore joint venture.

At two billion tonnes of iron ore with some of the highest grades in the industry, Simandou is one of the world’s biggest and richest reserves of the steelmaking material, but it has a controversial past.

For more than a decade, it was the centre of a bitter dispute that involved Rio Tinto, Vale and BSGR.

It began in 2008, when one of Guinea’s former dictators stripped Rio’s rights over two of the four blocks the deposit had been divided on and handed them BSGR. Rio was able keep the two southern blocks, but only after paying $700 million to the government in 2011. The deal guaranteed the miner tenure for the lifetime of the Simandou mine.

Vale steps in

Vale came into the picture when it acquired a 51% stake in the northern half of Simandou from BSGR for $2.5 billion. Later, Guinea revoked BSGR’s project rights due allegations of bribery and corruption surrounding the deal to acquire the rights.

BSGR and Steinmetz were able to put an end to the series of issues stemming from Simandou in February last year, through a deal with Guinean President Alpha Conde.

As part of the agreement with Guinea, BSGR agreed to walk away from blocks one and two of the Simandou project. The move paved the way for Niron Metals to acquired the rights to the smaller Zogota deposit, part of BSRG’s relinquished assets.

A few weeks later, a London arbitral court ordered BSGR to pay $1.2 billion to Vale. The judge based its decision partly on the fact that the government revoked the concession in 2014 after finding that BSGR had obtained it by bribing officials.

In November 2019, Steinmetz’s company lost an appeal to overturn the arbitration award it was ordered to pay Vale.

Simandou today

Rio Tinto currently holds a 45% stake in blocks three and four of Simandou, which it is actively planning to develop. China-controlled Chinalco owns 40% and the Guinea government 15%.

Both companies are said to be trying to persuade authorities to let them use ArcelorMittal’s railway to a port in neighbouring Liberia.

A joint venture between Guinea’s Société Miniere de Boke (SMB) and Singapore’s Winning International Group is close to securing approval from Beijing to start developing Simandou’s northern blocks.

China’s resource dependence on Guinea has increased in recent years. In 2017, Beijing agreed to loan President Condé’s administration $20 billion over almost 20 years in exchange for bauxite concessions.

Analysts say Guinea’s population has so far seen little benefit from Chinese investment.

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments