Op-Ed: Copper rally masks smelting power shift

Copper has rarely looked stronger.

Prices are hovering near record levels, buoyed by electrification, artificial intelligence-driven demand expectations, and a constrained pipeline of new mine supply. For producers and financial markets, the story is clear: copper is structurally bullish.

But beneath that headline narrative, a different reality is unfolding. We are witnessing a structural shift in bargaining power that is quietly reshaping the industry.

Upstream, producers and investors are focused on strong prices driven by electrification, AI demand and constrained mine supply, while midstream smelters face the sharpest collapse in treatment and refining charges in modern history, with benchmarks falling from $80/t and 8.0 c/lb in 2024 to effectively zero by 2026 and spot terms remaining negative through 2025. This divergence is not a contradiction; smelters buy concentrate, not headline LME prices, and their economics depend on TC/RCs, by-product credits and regional premiums. When concentrate is scarce, high copper prices do not translate into healthy margins for processors.

Governments and industry players increasingly recognize this as a strategic issue, not a cyclical anomaly. China has framed the problem around raw-material security and disorderly capacity growth, pushing for more disciplined smelting expansion and long-term procurement structures. Japan is consolidating concentrate purchasing through Pan Pacific Copper, while European observers describe a “silent crisis” in smelting.

Australia’s A$600 million support package for Mount Isa and Townsville underscores a broader shift: copper smelting is now viewed as critical infrastructure tied to industrial resilience, not just another cyclical business.

The likely outcomes of prolonged fee compression are already visible — closures, subsidies and coordination — and each carries implications for market structure. Custom smelters outside China remain the most vulnerable due to higher costs and lack of captive supply, while Chinese operators have delayed the impact through by-product credits such as sulphuric acid, gold and silver. But these buffers do not resolve the underlying imbalance. Instead, they buy time for consolidation.

This matters as much for miners as for smelters. A more concentrated processing sector would leave producers dependent on fewer counterparties for both offtake and financing, fundamentally altering negotiation dynamics. Copper can remain bullish at the metal level while the midstream becomes more fragile, more politicized and increasingly shaped by state-backed strategies.

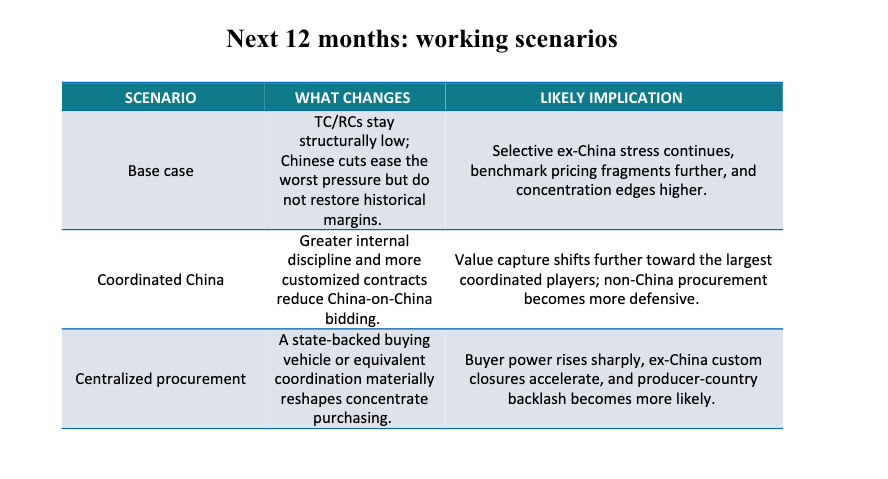

The direction of travel points toward greater buyer coordination, particularly in China, which already accounts for roughly half of global smelting capacity. A shift toward centralized, state-backed concentrate procurement would not necessarily lower copper prices immediately, but it would redefine how value is distributed. Negotiations could move toward longer-term contracts, customized supply terms, tighter blending rules and broader use of RMB settlement, while access to feedstock for non-Chinese smelters would tighten further.

Timing will be critical. Such a system would exert maximum influence not during acute concentrate shortages, when miners retain leverage, but when supply disruptions ease and availability improves. In that environment, coordinated buying could reset TC/RCs on China’s terms and accelerate consolidation across the global smelting landscape.

For the mining industry, the key question is no longer whether copper fundamentals are strong, but how the midstream will rebalance. Record prices can obscure the risk. If by-product credits weaken while fees remain depressed, closures will accelerate. If buyer coordination rises at the same time, the industry could move from a fee crisis to a structural shift in bargaining power.

The most important signals over the next year will not come from the copper price itself, but from indicators of midstream stress and coordination: smelter discipline in China, recovery in mine supply, the trajectory of by-product credits and the growing share of customized, non-benchmark contracts.

The strategic risk for miners is not simply China’s scale, but the possibility that prolonged fee compression transforms that scale into organized buyer power. As alternative smelting options disappear through closures and consolidation, dependence rises; even without a formal monopsony. That makes copper smelting a market-structure and public-affairs risk, not just a commercial negotiation.

For producer countries, the implication is clear: diversifying processing capacity and counterparties is becoming nearly as important as expanding mine output. A market that looks strong at the headline level can still become more concentrated, more political and harder to navigate from the seller’s side.

____________________

* Juan Ignacio Guzmán is the CEO of GEM Mining Consulting

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments