Op-Ed: Sodium-ion batteries are not the end of lithium, but they may be the end of something else

For the better part of a decade, the energy transition has rested on the simple geological assumption that electrification would always need enormous quantities of lithium, and whoever secured lithium supply would secure industrial advantage.

That idea has shaped everything. Governments rushed to publish critical minerals strategies. Vehicle manufacturers scrambled into offtake agreements. Mining companies pivoted overnight into “future-facing battery materials”. Investors poured money into anything remotely connected to spodumene, salars, or direct lithium extraction.

But there was logic behind the excitement. Lithium solved a very real problem, offering energy density high enough to make modern portable electronics and electric vehicles commercially viable. Entire industrial systems were built around that advantage. Without lithium-ion batteries, the modern EV sector would undoubtedly be far less developed than it is now, if at all.

But the battery conversation is beginning to change. Not dramatically, and certainly not overnight, but enough that a structural shift is becoming impossible for the mining sector to ignore.

The myth of total substitution

The significance of sodium-ion batteries is not that they suddenly outperform lithium-ion. They do not. Nobody is putting sodium-ion batteries into a high-performance sports car anytime soon. Energy density still matters enormously in applications where weight and range define competitiveness.

Instead, the real significance is structural. Sodium-ion batteries are positioned to fundamentally alter what parts of the supply chain matter most. It is less about elemental substitution and more about a geopolitical re-mapping.

One of the biggest misunderstandings in public discussions around critical minerals is the tendency to treat supply chains as purely industrial systems. Long before a battery reaches a factory floor, its supply chain is already shaped by economic geology. Lithium is not particularly rare in the Earth’s crust, but economically recoverable lithium is geologically selective. Commercial deposits require a strict chain of geological anomalies to form, namely through either the rare fractional crystallization of granitic melts (LCT pegmatites) or the long-term chemical enrichment of closed basins.

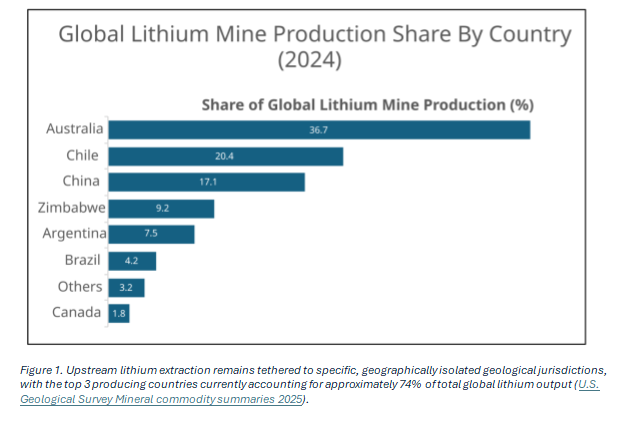

This geological selectivity has created a highly concentrated, delicate supply chain for the modern battery economy. Upstream lithium extraction is heavily tethered to specific, isolated regions (Figure 1). Hard-rock pegmatite deposits have allowed Australia to dominate global mining with a 36.7% market share, driven by major operations like Greenbushes and Pilgangoora. Meanwhile, the “Lithium Triangle” of Chile (20.4%) and Argentina (7.5%) remains strategically central due to its naturally concentrated salar brines.

However, raw extraction is only half the story. Whilst China accounts for just 17.1% of global mine production, it has masterfully capitalised on this geographic fragmentation by aggressively locking down midstream refining and chemical conversion capacity. It should come as no surprise at this point that, by controlling this critical processing bottleneck, Beijing has established enormous geopolitical leverage, effectively acting as the mandatory gateway connecting distant raw resources to the global battery factory floor.

The result was a supply chain built around relatively narrow geological and industrial choke points. The more electrification accelerated, the more governments realised they were exposed to a remarkably small number of upstream dependencies.

At one point, it genuinely felt like half the junior mining industry had opened an ore deposits textbook, found the word “pegmatite,” and decided it was now an energy transition specialist.

The Power of the Geologically Boring

Dependence creates pressure. And with the price of lithium behaving less like an industrial commodity and more like a memecoin running entirely on caffeine and panic, industrial systems will eventually try to reduce that pressure wherever possible. That is where sodium-ion becomes interesting. It is not because sodium is technologically miraculous, quite the opposite. Sodium’s greatest advantage is almost boringly simple. It is everywhere.

Unlike lithium, sodium (making up 2.3% of the Earth’s crust) is geologically abundant to the point of near irrelevance. It requires no extreme magmatic differentiation or rare tectonic settings. It is quite literally salt, existing in enormous quantities across global oceans and massive inland deposits. Countries with no realistic lithium potential still possess virtually infinite sodium resources.

Now here’s the key: With lithium, the primary bottleneck is upstream scarcity, but with sodium, the problem shifts entirely to downstream industrial execution. This distinction is quietly reshaping the geography of battery supply chains. Mass production is no longer a futuristic promise, it has arrived. Industry giants like CATL have already moved mass-produced sodium-ion passenger vehicles to dealerships, whilst grid-scale utility energy storage systems are clearing the 1 GWh threshold.

But if lithium-ion were genuinely being displaced outright, market leaders like CATL and BYD would effectively be undermining their own multi-billion-dollar dominance. That is not what is happening. Instead, the battery market is fragmenting into a “dual-chemistry” reality based on specific application tiers. Whilst premium mobility still relies on lithium to maximise energy density, mass-market applications are increasingly prioritising the cost stability, safety, and cold-weather capacity retention of sodium.

The paradox of Western strategy

For years, the battery industry largely accepted lithium dependency as the unavoidable cost of electrification. Sodium-ion shifts some of that strategic pressure downstream. Once sodium-ion batteries become commercially viable at scale for stationary storage,

lower-cost urban EVs, grid balancing systems, or industrial energy storage, then part of the battery economy moves from a geology-constrained model to a manufacturing-constrained one.

Ironically, this shifts the geopolitical advantage further toward China, running directly counter to Western policy objectives.

A lot of Western commentary assumes sodium-ion reduces strategic dependency because raw sodium is globally abundant and naturally “Foreign Entity of Concern (FEOC) compliant.” But abundance alone does not redistribute industrial power. CATL’s massive production scaling underscores a harsher reality. China currently controls over 90% of the installed and announced global sodium-ion manufacturing capacity.

This reveals a profound (and glaringly ironic) paradox for Western policymakers. Simply put, by removing the geographical constraint of the mine, you remove the one area where the West could potentially compete by simply finding and permitting a world-class asset.

If the resource is ubiquitous, competitive advantage transfers entirely to the players who master midstream chemical processing and downstream manufacturing economics. Crucially, the prize shifts to regions with cheap power, integrated industrial coordination, and sheer manufacturing speed, the exact domains where China is exceptionally dominant.

The shift in mining choke points

For Western policymakers who have framed critical minerals strategy strictly as a mining problem, this is an uncomfortable reality. Sodium-ion introduces a paradigm shift. It proves that the next major bottleneck in the energy transition isn’t the mine at all. It is the factory floor, the power grid, and the industrial capacity to build them, suggesting that the end of the lithium monopoly may well mean the beginning of an unassailable manufacturing one.

It is a transition that forces a stark moment of self-reflection. Once again, Western industrial policy is playing reactive catch-up to a trend Beijing mapped out decades ago. Whilst the West builds bureaucratic frameworks to secure today’s lithium mines, China has already spent a generation anticipating tomorrow’s sodium bottlenecks.

By removing the geographical constraints of the mine, the strategic equation is thrown entirely into the hands of those who command midstream chemical processing and downstream factory scale.

It is a reminder that the culture that birthed classical long-term statecraft still views the global resource map through a completely different generational lens, playing a multi-decade game of industrial chess whilst the rest of the world is still trying to read the board.

Dr. Nicholas Vafeas is an economic geologist specializing in critical raw materials, mineral supply chains, and energy policy.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments