Anglo faces headwinds in keeping restructuring on track

Anglo has been forced to accelerate its restructuring after successfully holding off a bid from BHP, the world’s biggest miner.

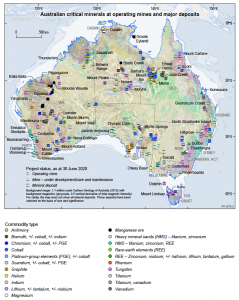

The Australian Trade and Investment Commission (Austrade) in collaboration with Geoscience Australia and the Department of Industry, Science, Energy and Resources recently published the second edition of the Australian Critical Minerals Prospectus, a document aimed at highlighting the country’s position on critical materials supply.

To prepare the report, the Australian government examined lists of critical minerals published in markets such as the United States, the European Union and Japan, and matched those against Australia’s known geological endowment.

The result is a list of 24 critical minerals that are either being produced or could be produced in Australia. The list was first identified in Australia’s Critical Minerals Strategy 2019 and includes antimony, beryllium, bismuth, chromium, cobalt, gallium, germanium, graphite, hafnium, helium, indium, lithium, magnesium, manganese, niobium, PGMs, REEs, rhenium, scandium, tantalum, titanium, tungsten, vanadium, and zirconium.

According to Geoscience Australia, these metals, non-metals and minerals are considered vital for the economic well-being of the world’s major and emerging economies, as they are key for developments in renewable energy, aerospace, defence technologies, automotive and in particular electric vehicles, telecommunications, and agri-tech. However, the supply of these materials may be at risk due to geological scarcity, geopolitical issues, trade policy or other factors.

Thus, the Prospectus seeks to identify Australia’s broader geological potential in critical minerals. It doesn’t, however, cover minerals processing, nor does it include overseas resources in which Australian companies may have a development or investment interest.

“Australia has the world’s sixth-largest rare-earth element resource base and is one of the few sources of dysprosium outside of China,” the document reads. “Australia’s rare-earth element production includes neodymium, praseodymium and dysprosium, which are important for permanent magnet production.”

The review also states that Australia is the world’s largest producer of lithium and a top-five producer of cobalt, manganese ore, antimony, zirconium and titanium mineral sands. The country also hosts some of the largest recoverable resources of tantalum, tungsten, vanadium, and niobium.

“With demand forecast to rise over the medium term, Australia has a commercial opportunity to build competitive critical minerals export markets, and to improve the domestic and global strategic supply of critical minerals,” the report says.

This last assertion -says market analyst Roskill – is the key driver behind the publication of the Prospectus.

In Roskill’s view, Australia is making sure to bring to the forefront that it is open for business to prospective end-users of critical materials, particularly in Europe where the critical materials debate has started to hit up with a particular focus on import dependence and concerns over the security of supply.