Cobalt tops Critical Materials Risk Index

The global supply chain of cobalt is the most at risk among the critical materials needed for the energy transition, a recent report by market intelligence provider Project Blue shows.

According to the firm’s Critical Materials Risk Index 2022, cobalt scored highly in terms of supply risk due to several reasons, the main one being that it is extracted mostly as a by-product and that most mines and refineries are concentrated in the Democratic Republic of Congo and China, respectively, with the bulk of the supply coming from a small number of consolidated producers.

Cobalt leads the index also because its extraction is linked to ongoing social issues in Central Africa, which raises ESG concerns among battery makers as the metal plays a key role in lithium-ion batteries, aerospace, and other critical applications.

The Risk Index examines 40 critical metals and minerals against variables selected to quantify supply risk, ESG risk, and economic importance. The data are normalized and weighted to produce three sub-indices which are then used to calculate a material’s overall rank.

The second spot, right after cobalt, is occupied by heavy rare earths such as europium and dysprosium, which are mostly refined in China with only one plant outside the Asian giant located in Malaysia. For this reason, REEs supply risk is actually higher than that of cobalt but since their economic importance and ESG risks are a little bit lower, they didn’t rank as high as the silver-grey metal.

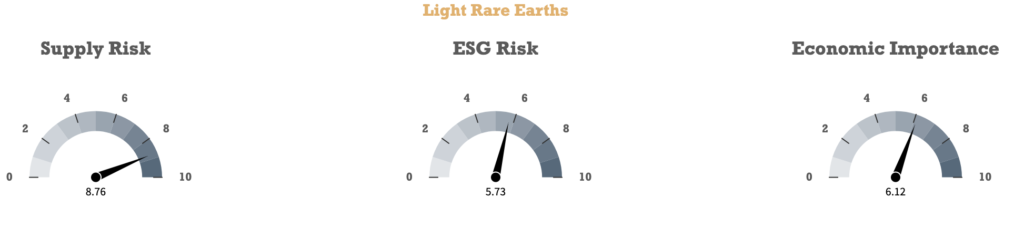

Since similar circumstances apply to niobium and light rare earths, they occupy the third and fifth spots in the Index with very high supply risks and lower ESG-associated risks, as well as not so high economic importance.

In the middle of these is magnesium, a material needed to harden aluminum alloys used to make automobiles and building supplies. Supply risks, mainly linked to China and Russia being the largest global producers of the element, place it in the fourth spot of the Risk Index.

Graphite, chromium, antimony, and vanadium complete the top 10, most of them scoring high due to the risks associated with their respective supply chains, with aluminum being the only outlier in its sixth spot and scoring high due to its economic importance.

“While it’s no surprise that cobalt, rare earths, and niobium top the global list, it’s important to remember that what makes a material critical is very much subjective, and depends on your position in the value chain,” Jack Bedder, co-founder of Project Blue, said in a media statement.

More News

Column: Copper price soars but smelters can’t bank on it to survive

June 30, 2026 | 04:01 pm

South32 sells nearly all its aluminum business to Alcoa for $5.6B

June 30, 2026 | 03:45 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Łukasz

Europium and dysprosium are not heavy REEs but middle REEs