Glencore strategy to underpin cobalt prices post covid-19

A year ago Glencore announced it was halting operations at its Mutanda copper-cobalt mine in the Congo, breathing life into a market that was trading at levels 70% below its peak, hit 18 months before.

Given that Mutanda is the world’s largest cobalt mine and responsible for around a fifth of global output in a market of just 135kt per year, market reaction was muted. Congo dominates world cobalt production and Mutanda was responsible for 60% of the Swiss commodities giant’s annual output.

Glencore has placed a strategic focus on forward selling its built-up hydroxide stocks

While mine output has been largely undisturbed in the Congo during covid-19, most of the material is shipped through the South African port of Durban, which had been in lockdown for extended periods earlier this year.

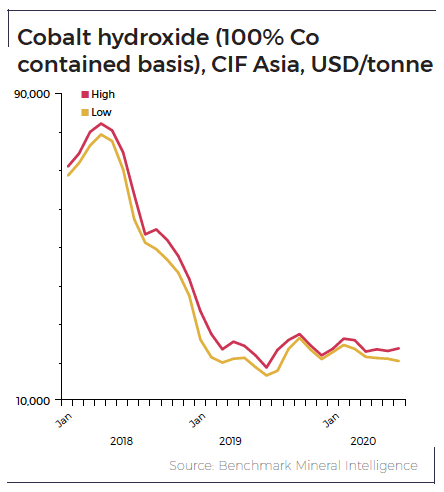

Benchmark Mineral Intelligence, a battery supply chain and price discovery agency, reports cobalt hydroxide (crystalline form produced at mines containing 20–40% cobalt) prices averaged $21,475 a tonne (100% Co, CIF Asia) in July, up 26% from the same month last year.

RELATED: Chinese battery breakthrough needn’t worry cobalt bulls

Benchmark says ongoing logistics problems led to a lack of material on the spot market in China. That caused a jump in payables and prices north of $23,000 a tonne for immediate delivery of cobalt going into August.

While disruptions along the Congo-South Africa-China route may ease over the rest of the year and more abundant supply could put pressure on prices again, a new report suggests Glencore’s strategy (similarly employed in the zinc market where the company also holds sway over a chunk of the market) could underpin cobalt prices over the medium term.

Roskill, a London-based metal and mineral research firm, says Glencore has signed several agreements with downstream lithium-ion cathode, cell and original equipment manufacturers customers, including Tesla, Korean giants Samsung and SK Innovation, and European battery manufacturer Umicore.

Glencore has placed a strategic focus on forward selling its built-up hydroxide stocks, as well as future production from Katanga in the DRC (which is still operating) and cobalt metal from Murrin Murrin in Australia (which is destined for BMW).

Roskill expects that Mutanda, in the south of the country near the Zambian border, will remain under care and maintenance for the next two years at least. This will allow Glencore to complete optimisation studies around the transition from oxide to sulphide ore and provide enough time for the market to recover.

Mutanda also produces around 200,000 tonnes of copper per year and when cobalt was trading at its highs in 2018, the battery raw material accounted for around half of the revenues from the operation.

RELATED: BMW avoids Congo cobalt conundrum – for now

More News

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

Japan buyers agree on higher aluminum fees Due to war disruption

July 03, 2026 | 09:04 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments