Gold price back below $1,700 despite surge in ETF buying

Investment inflows helped push the gold price to a seven-year high during Q1, as global gold demand in value terms reached $55 billion – the highest since Q2 2013.

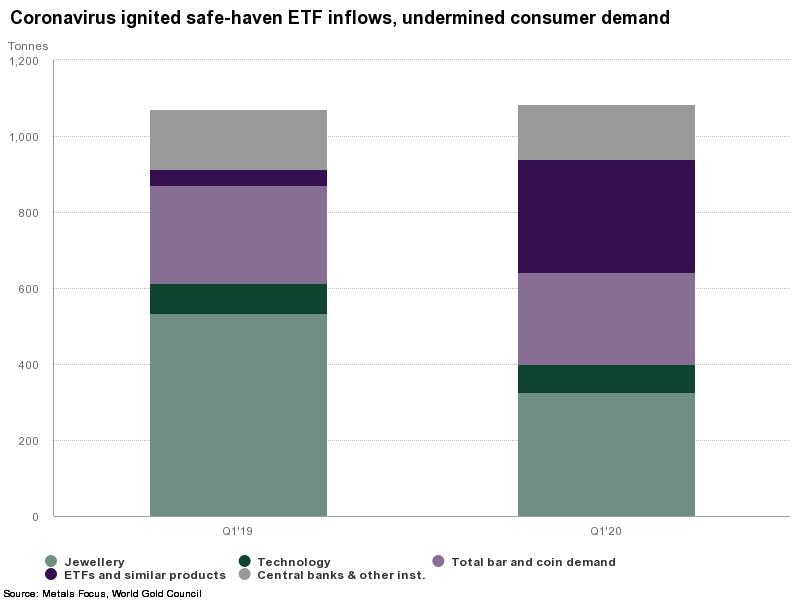

In the first quarter, global demand for the yellow metal inched up 1% year-on-year to 1,083.8 tonnes, in large part due to an 80% surge in total investment demand (to 539.6 tonnes) as investors look to safe-haven assets.

But spot gold is back below the $1,700/oz mark, down nearly 2% to $1,686.80 as of 1 p.m. EST Thursday. Gold futures for June delivery dropped 1% to $1,694.90 on the Comex. However, the metal is still on course for its best month in almost a year.

Gold-backed ETFs attracted huge inflows with 298 tonnes added, which pushed global holdings to a new record high of 3,185 tonnes, the Council said. Amid the economic uncertainty and financial market volatility, this was the highest quarterly inflow in four years.

Massive stockpiling of gold by investors during the covid-19 pandemic kept global demand stable for the first three months of 2020, offsetting marked weakness in consumer-focused sectors of the market, the World Gold Council reported on Thursday.

Lockdown measures around the world shuttered the two biggest consumer markets in China and India, causing a 39% decline in jewellery demand to 325.8 tonnes – the lowest in at least a decade.

“This is the biggest change to the market that I can remember,” said John Reade, the WGC’s chief market strategist, commenting on the current shift in gold demand trends.

“There’s a lot of potential for investment demand to be strong,” Reade added. “Whether it turns out to be big enough to compensate … remains to be seen.”

Bar and coin investment fell 6% to 241.6 tonnes, as a 19% drop in bar demand (to 150.4 tonnes) overpowered a sharp jump in demand for gold coins, up 36% to 76.9 tonnes, as a result of safe-haven buying by Western retail investors.

Technology demand also fell 8% to 73.4 tonnes, the lowest level recorded since WGC began collecting data.

Central banks continued to amass gold, although at a lower rate compared to Q1 2019, and the Council expects net buying to slow sharply. Russia announced that it would suspend long-term buying from April, signalling a sharp slowdown in global net buying.

Total supply of gold decreased to 1,066.2 tonnes, down 4% from 2019, as lockdowns around the world hit mine production and gold recycling, the WGC added.

More News

Antofagasta agrees spot-indexed copper ore sales with some Chinese smelters, SMM says

The reported deal would mark a break with a decades-old practice.

July 01, 2026 | 08:15 am

Eni and Mercuria agree to join forces in commodity trading

July 01, 2026 | 08:05 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments