India rises as China slows in mineral demand shift

Vale’s (NYSE: VALE) push to expand iron ore shipments into India signals a deeper structural shift in demand, highlighting how one of the world’s largest producers is positioning for a changing market.

Media reports point that Vale is targeting a stronger foothold in one of the fastest-growing steel markets, underscoring a broader rebalancing away from China’s once-dominant role in driving seaborne iron ore demand.

Recent commentary from major miners reinforces that trend. Vale’s chief executive said in November that India’s steel production could double by the end of the decade, while China’s output has plateaued at roughly 1 billion tonnes annually. BHP (ASX: BHP) echoed that view in February, noting that while Chinese demand remains resilient, structural weakness in real estate persists.

Demand to level off

Growth in India and other emerging Asian economies is increasingly offsetting softer Chinese demand, with seaborne iron ore consumption expected to level off as a result.

The shift extends beyond steel. India’s electricity demand is projected to grow 6.4% annually through 2030, according to the International Energy Agency, adding more than 570 TWh over five years.

That expansion points to rising demand not only for iron ore, but also for copper, aluminium and battery metals as electrification accelerates across transport, industry and power systems.

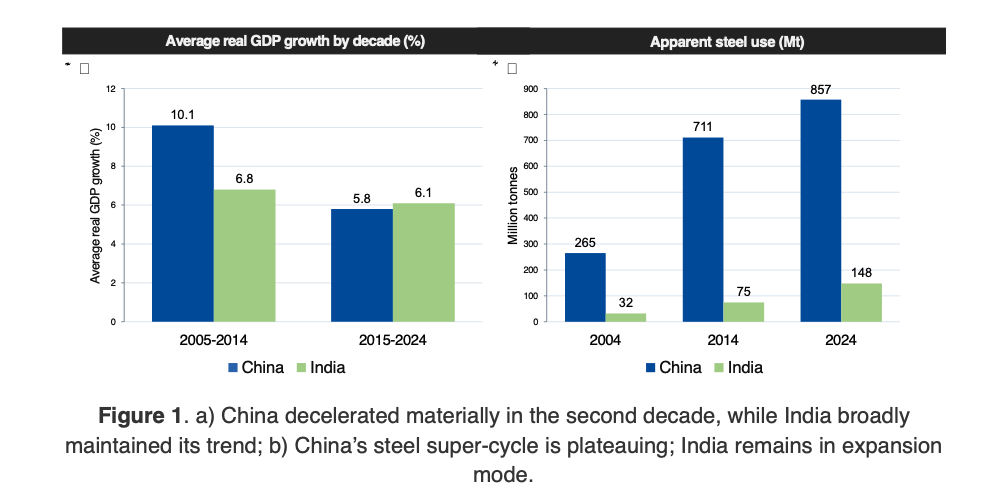

Over the past two decades, China and India have followed diverging growth paths. China’s real GDP growth slowed from an average of about 10.1% between 2005 and 2014 to roughly 5.8% from 2015 to 2024, based on IMF and World Bank data. India, by contrast, maintained more stable growth, averaging about 6.8% and 6.1% over the same periods. While China remains far larger in both economic scale and mineral consumption, its growth has decelerated sharply from the super-cycle era, while India continues to expand from a much larger base than it did twenty years ago.

Differences in development stage are equally important. China’s GDP per capita reached about $13,300 in 2024, compared with roughly $2,700 in India. That gap reflects China’s transition into a more mature phase, where housing saturation, slower construction growth and increased scrap availability reduce the metal intensity of economic expansion. India, by contrast, remains in a build-out phase, with significant room for growth in urban housing, infrastructure, logistics and manufacturing.

Steel demand illustrates the contrast most clearly. China’s apparent steel use surged from 265 million tonnes in 2004 to more than 1 billion tonnes at its peak in 2020, before easing to about 857 million tonnes in 2024. India’s demand climbed steadily from 32 million tonnes in 2004 to 148 million tonnes in 2024 and continues to rise. While China’s scale remains unmatched, its demand has likely peaked, whereas India’s remains firmly in expansion mode.

Markets reshape

This divergence is beginning to reshape iron ore markets. For years, China’s construction boom drove global demand. That influence remains significant, but incremental growth is now increasingly coming from India and a broader group of emerging Asian economies rather than from further expansion in Chinese real estate.

Looking ahead, long-term demand forecasts remain uncertain, but broad growth ranges offer guidance. China’s GDP growth is likely to settle in the mid-3% to high-4% range over the next decade, supported by investment in grids, electric vehicles and advanced manufacturing even as property weakens. India, meanwhile, is expected to grow in the mid-5% to low-7% range, driven by infrastructure expansion, urbanization and electrification.

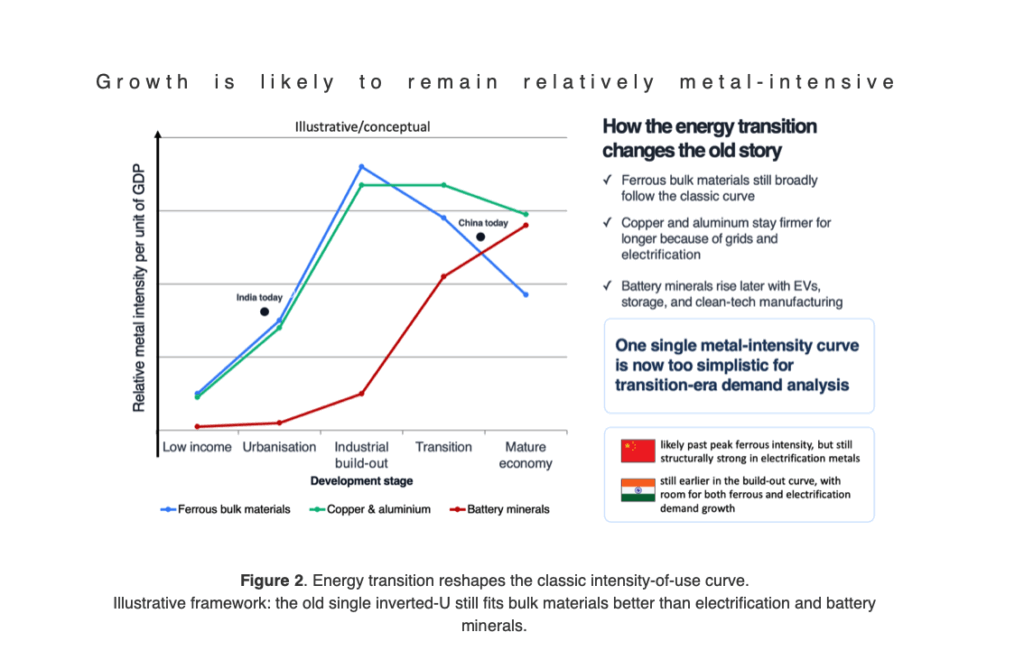

These dynamics align with the well-established intensity-of-use framework, where metal demand rises rapidly during industrialization before tapering as economies mature. China’s slowdown in metal intensity reflects structural factors including demographic shifts, a larger housing stock and a transition toward services and higher-value manufacturing. Demand is not collapsing but shifting toward electrification-related sectors such as grids, batteries and machinery.

India appears to be entering the more metal-intensive phase of that curve. Lower income levels, limited infrastructure and ongoing urbanization suggest sustained demand growth across a range of commodities. However, its development path is likely to be more diversified and electricity-driven than China’s earlier property-led expansion.

The global demand map is therefore broadening rather than simply shifting. China is expected to remain the largest single consumer of most industrial metals for decades, particularly in copper and nickel, supported by its scale and dominance in manufacturing and clean energy supply chains.

What is changing is the source of marginal growth. In ferrous markets, including iron ore and metallurgical coal, India and other emerging Asian economies are becoming the primary drivers of new demand. That trend underpins strategic moves by producers such as Vale and BHP, as India’s steel ambitions and infrastructure expansion position it as a central growth engine.

In electrification metals, the outlook is more balanced. China’s demand will remain strong due to its leadership in electric vehicles, grid infrastructure and battery manufacturing, while India’s consumption is expected to rise तेजी from a smaller base as it expands its energy and industrial systems.

The emerging pattern is not one of replacement but diversification. China will remain the anchor of global mineral demand, while India is set to become the most important source of incremental growth.

For miners, the implications are clear: China will continue to shape prices, but long-term growth increasingly depends on positioning for India’s sustained and infrastructure-heavy expansion.

* Patricio Faúndez is GEM Consuling’s economics leader.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments