Iron ore price rout hacks $160 billion off Top 50 mining stocks

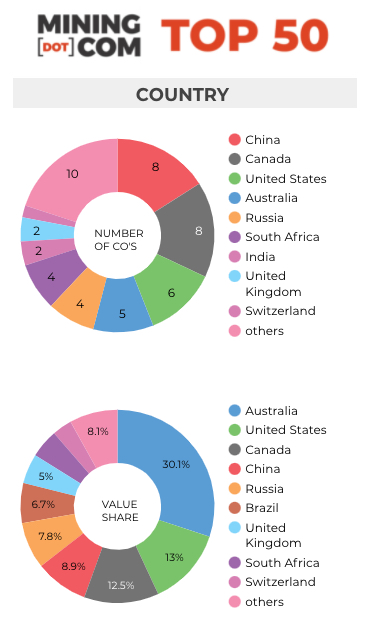

At just over $1.3 trillion, the MINING.COM Top 50* most valuable mining companies lost a combined $158.5 billion in market capitalization over the three months to end September, as iron ore’s plunge and copper’s lacklustre performance prompted a sell-off in the sector’s largest names.

Steel blues

The top five iron ore producers – Rio Tinto, Vale, BHP, Fortescue and Anglo American – were responsible for virtually all the losses and strong gains in lithium, coal and uranium stocks further down the ranking were unable to stem the tide of negative sentiment over the quarter.

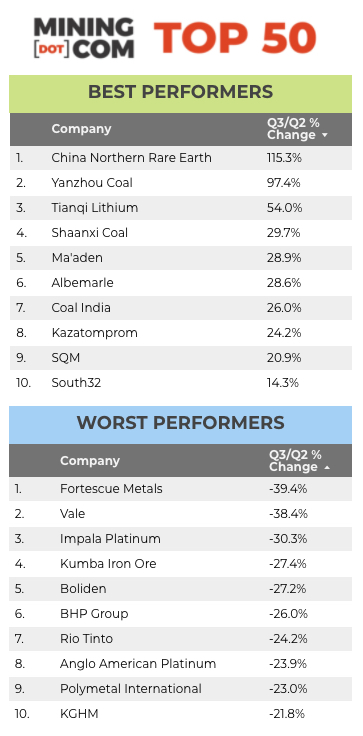

The Q3 sell-off dragged the Big 3 deep into negative territory for the year and Fortescue’s efforts at diversifying its portfolio can not come soon enough – the world’s number four producer of the steelmaking raw material was the worst performer of the quarter, with a 39% decline.

Among the top decliners, Fortescue is closely followed closely by Vale, which over and above its iron ore woes is contending with a fire at its flagship copper mine and is suspending operations at its Brazil nickel mine in a dispute over its licence.

With the iron ore market in full retreat, Brazil’s CSN Mineração, one of the biggest mining IPOs since Glencore in 2011 when it debuted in Q1, falls out of the top 50, but thanks to still robust US steel prices, Cleveland-Cliffs looks secure in the top 50 for now after spending years in the wilderness.

Energized

With no exposure to iron ore other than trading, Glencore bucked the trend during Q3 and the Swiss commodities giant is up by nearly half so far this year. Glencore has not abandoned coal mining, like its peers and its coal, gas and oil trading arm is benefiting from sky high prices for energy.

Evidence of the volatility of commodities markets is the spectacular performance of coal miners during the quarter; a sector that this time last year looked set to disappear from the ranking altogether.

The value of the three remaining coal companies (the ranking excludes power utilities such as Shenhua Energy that operate their own mines) surged and Coal India finally arrested its decline, leaping nine positions to spot number 25. Four years ago the world’s largest coal miner made it to number 4.

Nuclear option

Thanks to a rally in nuclear fuel a decade in the making since the Fukushima disaster, uranium stocks rejoin the top 50 ranking for the first time in many years.

The value of Kazakhstan’s Kazatomprom, which has expanded its exchange listings well beyond Almaty, more than doubled this year, while Cameco entered at position 47 from a ranking at number 60 at the end of last year.

Last month, Saskatoon-based Cameco signed an MOU for what uranium bulls hope would be the first of many supply deals for a potential fleet of small modular reactors (SMR). SMRs are seen as a potential replacement for diesel at mines and communities in remote locations.

Lithium lifted

Lithium prices have extended their year long rally as electric car demand motors along and the three producers in the top 50 now have a collective value of nearly $64 billion after adding $16.5 billion during the quarter.

Tianqi Lithium briefly fell out of the ranking at the end of 2019 as its market value fell below $5 billion, but the Shenzhen-listed producer has now pierced the top 20, surpassing SQM in the process, with a value of more than $23 billion.

The world number one producer Albemarle, up 50% since the start of the year, said last week it is buying a Chinese lithium processor in an effort to expand downstream.

Rare rally

The top performer for the quarter is also benefiting from rising EV demand and the world’s top rare earth producer (as a byproduct of iron ore) China Northern Rare Earth doubled in value over the three months to end September.

So far this year the Shanghai-listed company is up 230% and now occupies the 16th spot, from 48th at the end of 2019. China, responsible for nearly four-fifths of global rare earth production, is reportedly further consolidating its domestic industry into just two firms – one in southern China to oversee medium-to-heavy rare earths, and the other in the north which will control light rare earth extraction.

Click on image for full-size table:

*NOTES:

Source: MINING.COM, Miningintelligence, Morningstar, GoogleFinance, company reports. Trading data from primary-listed exchange where applicable at close Sept. 30, currency cross-rates Oct. 1 2021.

Percentage change based on US$ market cap difference, not share price in local currency.

Market capitalization calculated at primary exchange, where applicable, from total shares outstanding, not only free-floating shares.

As with any ranking, criteria for inclusion are contentious issues. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining, which owns the world’s largest gold mine, Eurochem, a major potash firm, Singapore-based trader Trafigura, and a number of entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or warrant a seat on the board?

This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialized financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals.

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy where power, ports and railways make up a large portion of revenues pose a problem, as do diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat in the ranking as well as Kumba Iron Ore.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology.

More News

Agnico Eagle suspends Quebec pit mining, flags production hit

July 02, 2026 | 06:29 am

Emirates Global Aluminium sees faster progress restoring Al Taweelah

July 02, 2026 | 06:23 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments