Junior financing evaporates as cobalt, lithium prices slump

In the second quarter this year, cobalt and lithium prices dropped to the lowest point in more than two years, driven by short-term oversupply which is taking longer than anticipated to correct.

Mining Intelligence analysed the effect of the lithium and cobalt price decline and the flow of investments into exploration campaigns and development programs.

Both indicators suggest that future supplies of primary battery metals required to meet rising demand from EV manufacturers and other industries will not be met if the market stays in a slump.

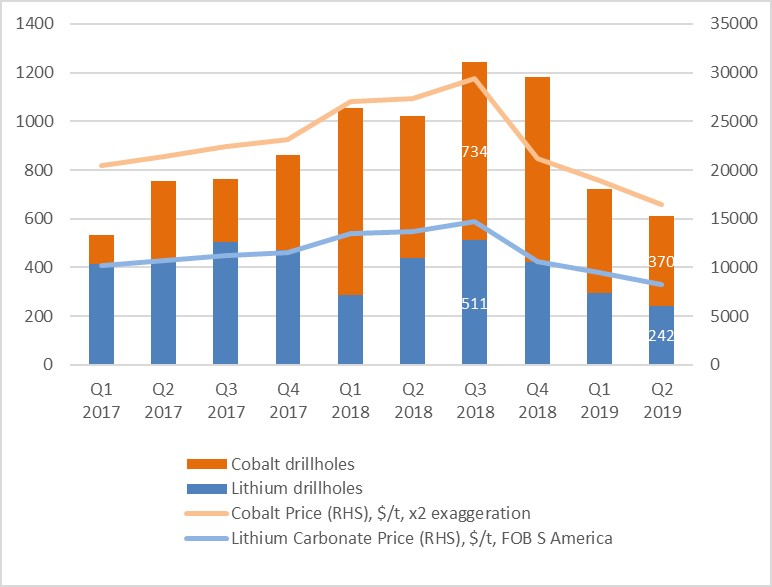

The Mining Intelligence Data Application reveals that in Q2 2019, drilling activities focused on exploration and resource evaluation of lithium and cobalt deposits, dropped to the lowest level in two years. Number of completed drillholes dwindled by more than 50% from the peak reached during Q3 2018.

Companies reacted quickly to the deteriorating market conditions and curtailed drilling operatively to prevent excessive cash burn.

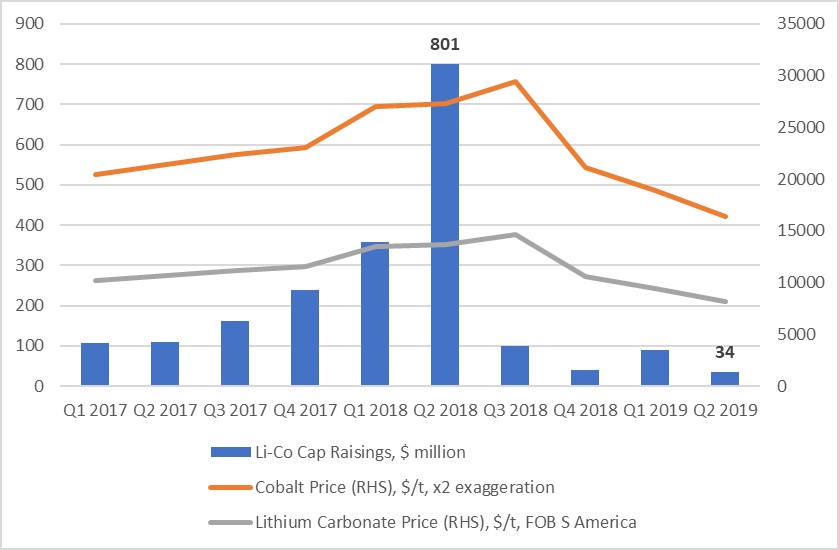

Another important indicator is capital raisings, which is a barometer of investor confidence. The amount of capital raised through equity placement reflects the sentiment in the mining industry, as this capital is the main source of liquidity to finance exploration and development activities by juniors and emerging producers.

This indicator shows that investors lost confidence in battery metal sector. In Q2 2019, capital raised on stock exchanges by lithium and cobalt players dropped sharply from the stunning $801 million raised in Q2 2018 to a record-low level of $34 million in Q2 2019.

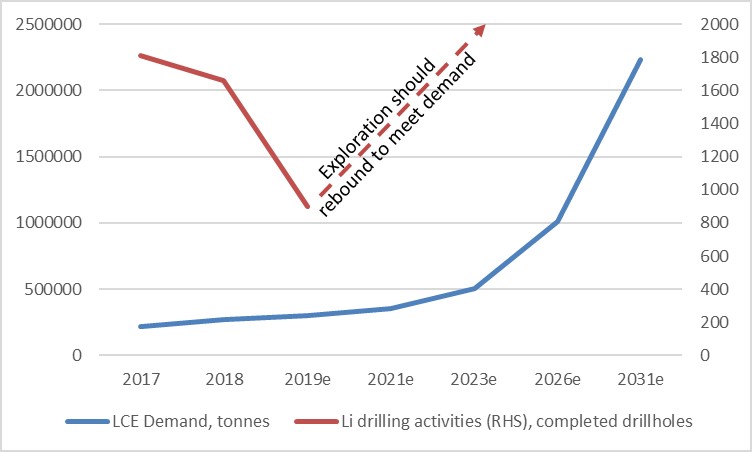

Despite recent softness in the lithium and cobalt markets, an industry consensus is that long-term demand fundamentals are strong. Projected lithium demand will grow approximately ten-fold by 2031 from the current level (Figure 3).

Though miners will have to increase drilling activities soon to keep pace with demand, there is no indication of that on the horizon.

Figure 3. LCE projected demand and Li drilling activities. Source: Consolidated industry forecasts, Mining Intelligence data.

Map of major producing mines and mine development projects of minerals used in Lithium Ion Batteries. Commodities include Lithium, Graphite and Cobalt. Map includes locations of 240+ producing mines, 45 development projects, 110+ projects in economic assessment, and 40 suspended mines.

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments