Lithium prices to remain low as “hype” meets “reality” — CRU

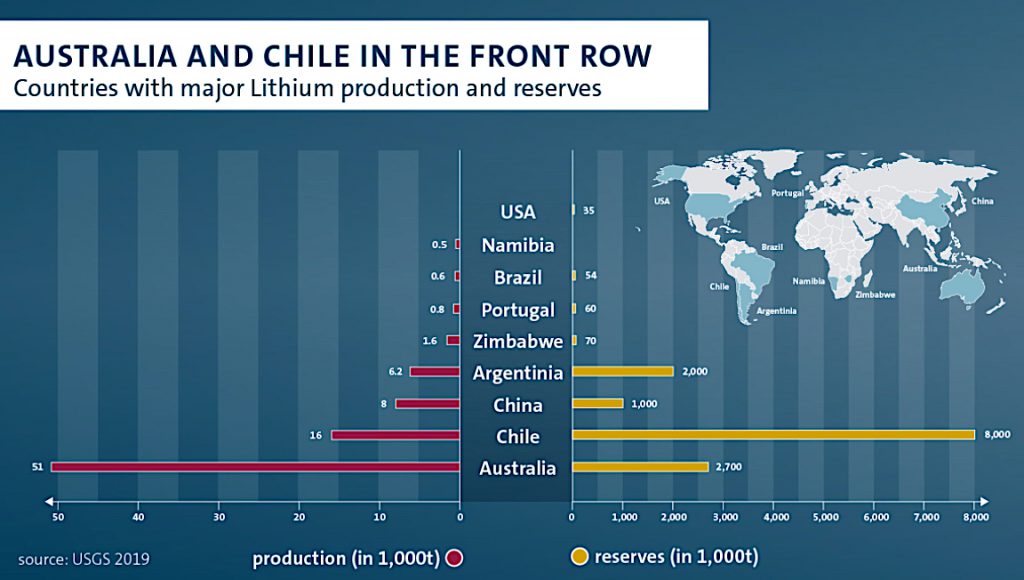

An ongoing avalanche of lithium supply, coming mostly from Australia, as well as cuts to China’s electric-vehicles (EVs) subsidies, is set to keep prices for the coveted battery metal in the single digits for longer than expected, analysts at commodity research group CRU warn.

Prices for lithium carbonate, the most common type used in the batteries that power electric cars, doubled over 2016 and 2017, but have fallen by more than 40% over the past year, crashing through the $10/kg mark at the end of July.

While many market players continue to forecast long-run prices in the mid-teens, based on bullish forecasts for sales of EVs and energy storage systems, CRU analysts remain unconvinced.

Based on previous experience in other commodities, the experts believe that “hype” has met “reality,” adding that refinery bottlenecks and the potential for ramp-up delays in the mining and refining sectors are not enough reasons to forecast a quick price recovery.

CRU says that lithium prices will continue to be governed by cost fundamentals, which will keep them in the single-figures. “This is the same message we have continually conveyed to CRU clients since November 2017,” analysts say.

Cutbacks

The analysts’ view seems to be backed by the main producers. Earlier this month, Albemarle Corp (NYSE: ALB), the world’s No. 1 lithium miner, postponed plans to add about 125,000 tonnes of processing capacity due to oversupply.

The company has also revised a deal to buy into Australia’s Mineral Resources’ (ASX: MIN) Wodgina lithium mine and said it would delay building 75,000 tonnes of processing capacity at Kemerton, also in Australia.

Map of major producing mines and mine development projects of minerals used in Lithium Ion Batteries. Commodities include Lithium, Graphite and Cobalt. Map includes locations of 240+ producing mines, 45 development projects, 110+ projects in economic assessment, and 40 suspended mines.

In November, the miner put plans on the back burner to increase output capacity at its operations in Chile beyond 2021. That project would have produced lithium carbonate.

Chile’s Chemical and Mining Society (SQM), the world’s second largest lithium producer, foresees strong long-term demand for the white metal, but has said it expected sales volume this year to rise slightly from 2018.

“It is very difficult to predict our sales volume for 2019 and 2020, it depends on supply and demand equilibrium,” the company’s new chief executive, Ricardo Ramos, said in February.

“The timing of the start and the ramp-up of new projects is also difficult to assess,” he noted.

Earlier this year, the Santiago-based company pushed back a key expansion at its Atacama salt flat operations from the end of 2020 to late 2021.

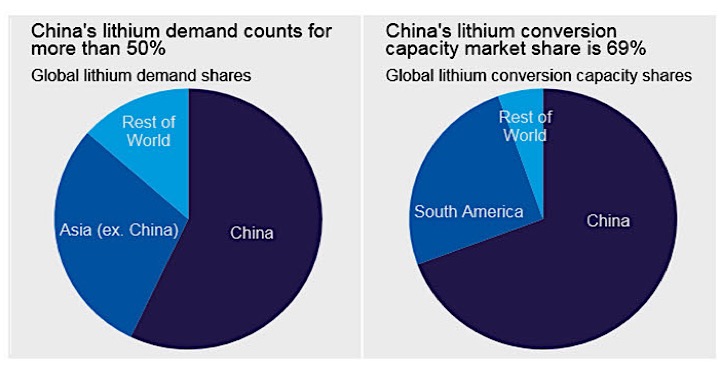

Lithium carbonate prices in China, the world’s top consumer, have dropped by nearly 20% since the beginning of 2019 to RMB 65,000/t, equivalent to $9.25/kg lithium carbonate equivalent (LCE), according to CRU’s price estimates. Lithium hydroxide has fallen by 30% to RMB 74,500/t.

China is also the biggest supplier of lithium converted products.

“Many market players look to nation’s lithium spot prices as a bellwether of market health and therefore the continued decline of lithium prices has put mounting pressure on the global lithium market,” CRU concludes.

More News

Antofagasta agrees spot-indexed copper ore sales with some Chinese smelters, SMM says

The reported deal would mark a break with a decades-old practice.

July 01, 2026 | 08:15 am

Eni and Mercuria agree to join forces in commodity trading

July 01, 2026 | 08:05 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments