Rare earth metals production is no longer monopolized by China

Rare Earth Elements: The Technology Metals

In the midst of our daily hustle and bustle, we often don’t notice the raw materials that go into the technologies we rely on.

Rare earth metals, also known as rare earth elements or simply “rare earths”, are one such group of raw materials. From this group of 17 minerals, many are found in a range of technologies—from our smartphones and laptops to electric vehicles and wind turbines.

Rare Earth Metals Production Over the Years

Despite the relative abundance of rare earth deposits, extracting them from the ground is difficult, and preparing them for usage entails significant environmental risks.

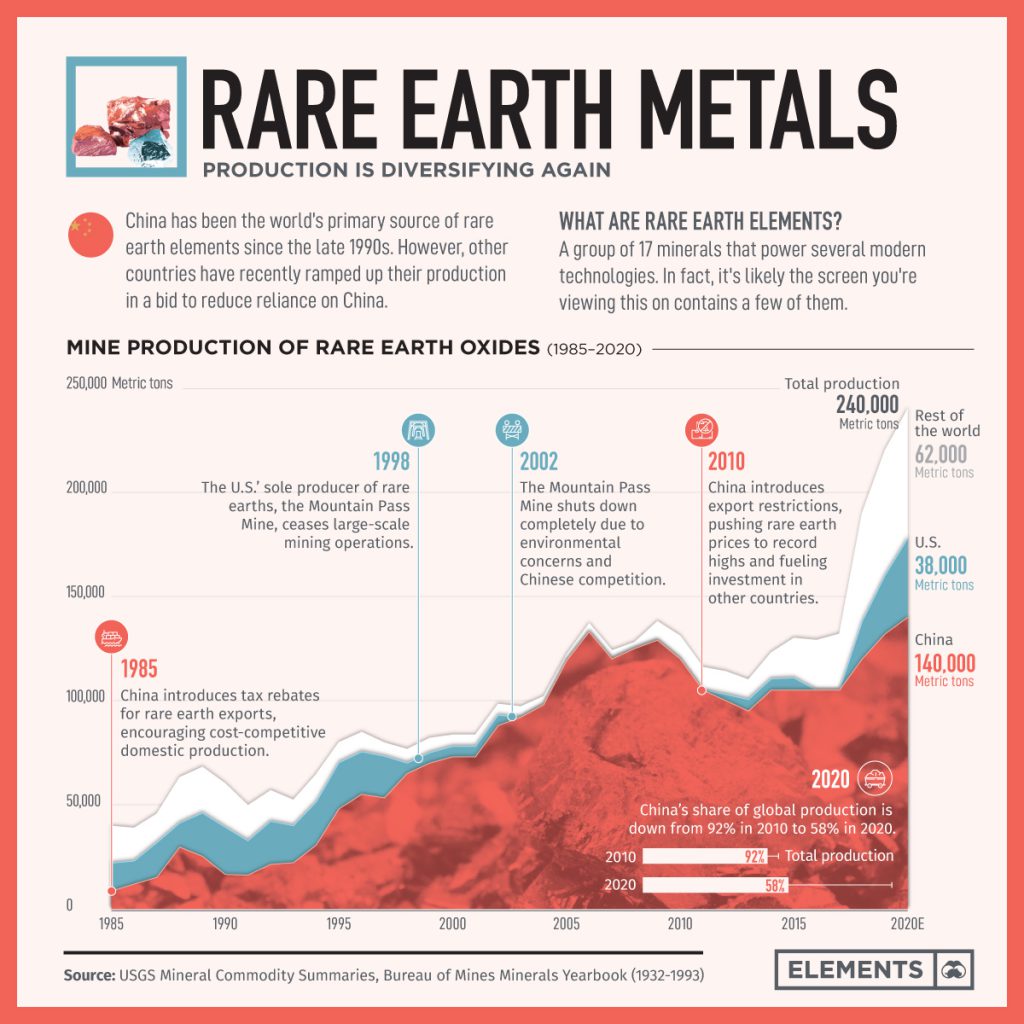

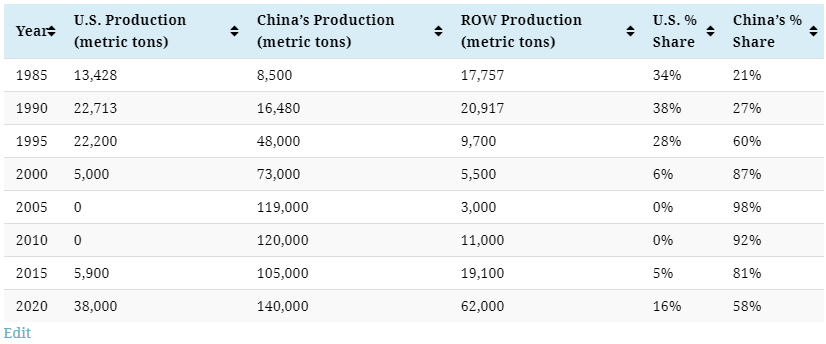

The U.S. was the world’s leading producer of rare earth metals from the 1960s to the 1980s. However, China took the helm in the 1990s and has been the dominant producer ever since.

In 1985, China introduced a policy that partially refunded the taxes paid by domestic producers of rare earths, which lowered costs for Chinese mining companies. This, in addition to lax environmental regulations and cheap labor, made China’s rare earth industry increasingly competitive. In fact, its production increased 464% between 1985 and 1995.

Meanwhile, in California, the Mountain Pass Mine struggled to compete with Chinese producers while facing stringent environmental regulations. Therefore, the U.S. share of production declined from 34% in 1985 to 6% in 2000 before ceasing completely in 2002.

Putting Rare Earths in Different Baskets

In 2010, China slashed its rare earth export quotas by 37%, pushing rare earth prices to all-time highs. This, in turn, fueled an influx of capital into the rare earth mining industry and kickstarted mining in other countries.

Namely, Australia saw a 672% increase in rare earth production over the last decade, and more recently, Myanmar entered the mix—producing 30,000 metric tons of rare earths in 2020. Additionally, the Mountain Pass Mine is undergoing a revival following an investment from MP Materials in 2018. As a result, the U.S. share of production is growing again.

While the mining of rare earth metals is diversifying, 80% of refining still occurs in China. With the demand for rare earths projected to double by 2030, building both mining and refining capacity overseas may prove key in reducing reliance on China.

More News

Column: Battery metals recovery runs into stop-start EV market

Prices of lithium, cobalt and nickel have all recovered from their 2024-2025 lows.

July 05, 2026 | 10:09 am

Zimbabwe lab sees regional gold hunt accelerate as prices soar

July 03, 2026 | 11:49 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments