Rio Tinto looks at developing Simandou again — report

Rio Tinto (ASX, LON: RIO) is mulling options to develop the giant Simandou iron ore deposit in Guinea, which almost sold last year to its partner in the project Aluminium Corp of China, or Chinalco, as it is known.

People familiar with the matter told Bloomberg on Thursday that the world’s No. 2 miner has rehired consultants to work with its own team on how it would be possible to export ore, should the mine be developed.

Guinea has always said that Simandou’s output would have to be shipped via the country’s own ports. This means that the project would have to include a 650km trans-Guinean railway line and a port, which could push the total investment needed to a whopping $23 billion.

Rio is said to have rehired consultants to work with its own team on how it would be possible to export ore, should the mine be developed

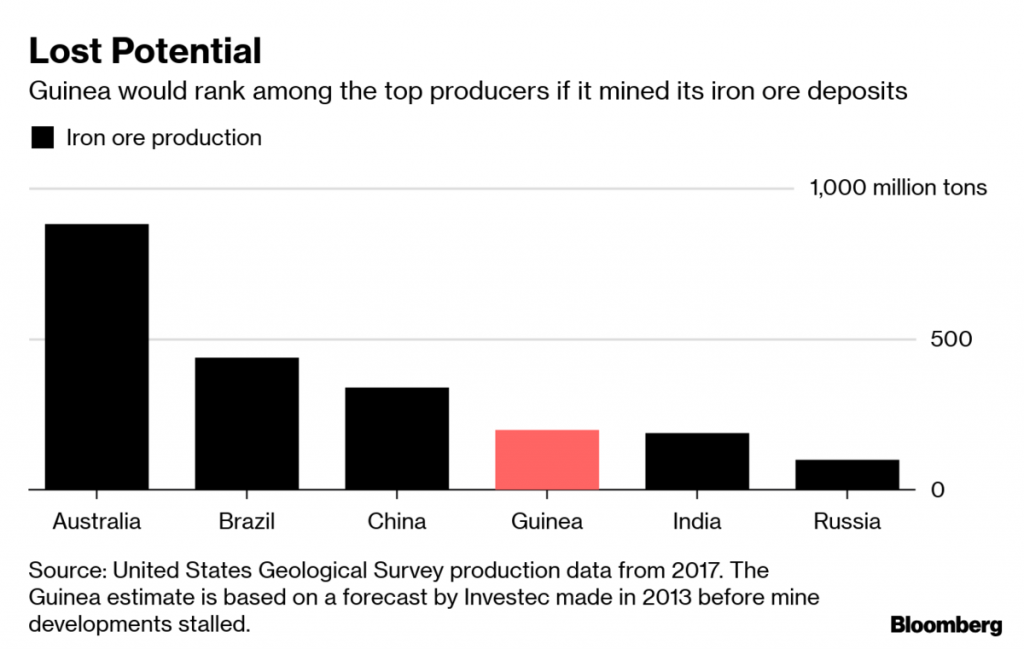

Simandou is one of the world’s richest reserves of high-grade iron ore, holding an estimated 2 billion tonnes of the steelmaking ingredient. It’s also one of the most easily exploitable iron ore fields outside of Australia’s Pilbara region and top producer Vale’s Brazilian home base.

At full production, the concession would export up to 100 million tonnes per year – that’s a third of Rio’s total capacity at the moment – and would catapult the company past Vale as world number one iron ore miner.

Simandou would by itself be the world’s fifth-largest producer behind Australia’s Fortescue Metals and BHP.

The asset, however, has been a source of headaches for Rio since it was first granted rights to start prospecting for iron ore two decades ago.

In 2008, one of Guinea’s former dictators stripped Rio’s rights over two of the four blocks and handed them to BSG Resources, the mining arm of Israeli diamond billionaire Beny Steinmetz. Rio was able keep to the two southern blocks but only after paying $700 million to the government in 2011, which guaranteed the miner tenure for the lifetime of the Simandou mine.

That deal came under scrutiny in 2016, forcing Rio to fire two senior managers over a questionable $10.5 million payment made to a consultant who helped the company secure the two blocks and alerted authorities, including the US Department of Justice and the UK’s Serious Fraud Office.

BSG Resources and Steinmetz were also subject of several investigations over bribery and corruption accusations, but it was able to put an end to and to all that in February this year, through a deal with Guinean President Alpha Conde.

Such agreement removes a key obstacle for Simandou to move forward. Rio holds a 45% stake in two of the four blocks that make up the giant Simandou deposit, while state-controlled Chinalco owns 40% and the Guinea government 15%.

More News

GreenMet plans $150M rare earth processing hub in West Virginia

July 01, 2026 | 09:36 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments