Tin price surge to subside by end of year – report

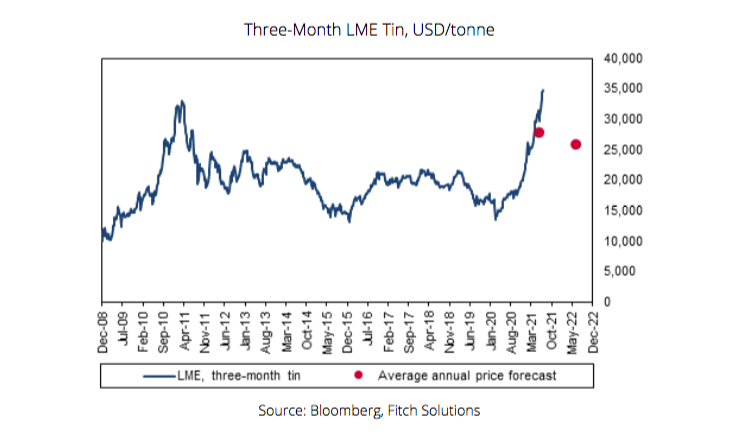

In its latest industry report, market analyst Fitch Solutions revised up its average tin price forecast for 2021 from $23,000/tonne to $28,000/tonne to account for the surge in prices to record highs during the year-to-date. The tin market has outperformed all other base metals in the first half of this year.

The slow pace at which global tin supply has recovered from the covid-19 pandemic has been outstripped by the rapid recovery in demand, Fitch says.

Short term outlook

The resulting reduction of global refined tin stockpiles has forced prices higher and Fitch expects that limited supply growth will persist through Q321.

This is due to lockdown restrictions that have been implemented in Indonesia (since July) and Malaysia (since May), which are disrupting the reopening of tin mine and smelting capacity in the two countries. Indonesia and Malaysia accounted for a combined 30% of global refined tin production in 2020.

Market tightness should begin to ease by the end of 2021 and this should start to drag prices lower. As a result, Fitch forecasts tin prices to peak before the end of the year.

On the demand side, record high prices for refined tin will start to result in rationing of demand by electronics manufacturers as they struggle to pass on higher input costs to end users.

On the supply side, the eventual relaxation of lockdown restrictions in Indonesia and Malaysia will boost global refined tin exports, Fitch says. Major producers such as Indonesian state-miner PT Timah will eventually reverse the significant production cuts enacted during 2020, encouraged by high prices.

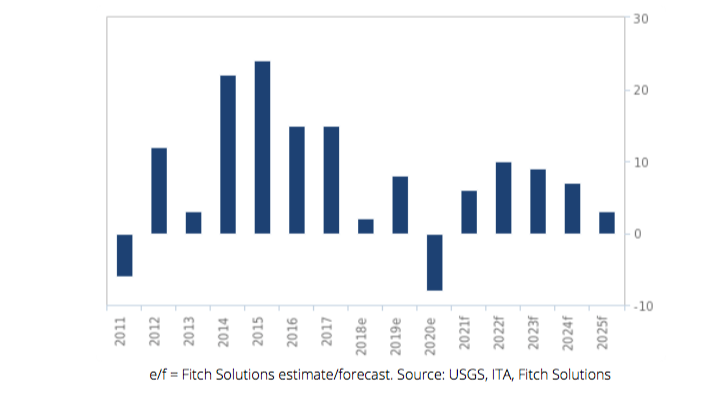

At the same time, new projects will come online such as in Malaysia, where Malaysian Smelting Corp expects to commission its new Pulau Indah plant in 2021. Overall, Fitch forecasts global refined tin production to grow by 12.5% y-o-y. This growth rate significantly exceeds the 10-year average growth rate of 0.2% y-o-y.

Long-term outlook

Fitch expects the global refined tin market to move into surplus by the end of 2021 and to continue posting annual surpluses through to 2025. As a result, Fitch forecasts prices to edge lower over the coming years to trough at an average of $21,000/tonne in 2024. While lower than $28,000/tonne in 2021, this would still be above the 2016-2020 average of $18,729/tonne.

Surplus in 2021 as supply loosens market

Over the second half of the decade, Fitch says prices will begin to strengthen again as global demand increasingly outstrips supply.

Fitch forecasts prices to average $20,000/tonne over 2026-2030 compared to $23,800/tonne over 2021-2025, a shift that will be driven by the erosion of global market oversupply.

The analyst forecasts an average annual global production surplus of 7,700 tonnes to flip to an average deficit of 9,000 tonnes over 2026-2030. Refined tin supply growth is expected to slow considerably and average just 0.3% annually over the second-half of the decade.

A thin pipeline of tin mining projects will tighten the tin concentrate market, leading to increased competition among smelters and constrained ore feed for refined output growth. Ultimately, this will allow the market to tighten and return to a production balance deficit by 2026, Fitch says, adding that prices will rise accordingly as demand growth outstrips the constrained growth in refined tin supply.

Over the second half of the decade, Fitch says, prices will begin to strengthen again as global demand increasingly outstrips supply.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

Jeffrey Sawicki

LOL! 15 month price is 32k per tonne, cash price is 36.4k/tonne.

What kind of crack are you smoking?

This semiconductor shortage is actually a maximum semiconductor output period. The fabs keep increasing their capacity and every single chip maker is building new fabs that will be operational with in 2 years. That’s a lot of soldering driving the tin demand.

Don’t forget tin anodes in Lithium batteries and tin based peroskite crystals (solar power) on the horizon.

Tin to 50k by end of year, peace out newbs

Benny Boy

Yeah and all stockpiles are empty, except in China. Even if they manage to produce more then whats used it will just go to try and restore empty warehouses.