A copper market awash with metal sours traders’ bullish mood

A bearish mood is sweeping through the physical copper market.

Even before the war in Iran triggered widespread concerns over a potential hit to global growth, copper sellers were struggling to offload cargoes as demand slumps in China and traders wind down deals to ship copper to the US ahead of potential tariffs.

Now copper is caught in a jarring disconnect: the real-world metal market looks increasingly oversupplied, yet futures prices remain at near-record levels thanks to demand from bullish investors. But with excess supplies stacking up in the physical industry and worries over growth building, the crucial question is: how long can it continue?

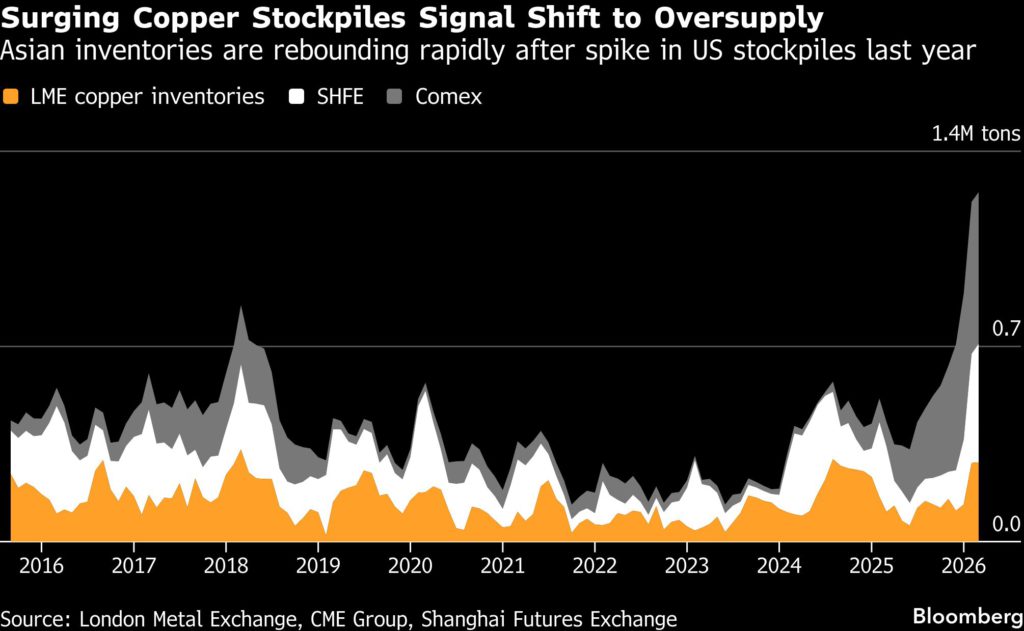

Several traders and producers have moved to offload copper into the spot market in recent weeks, a sharp contrast from just a few months ago when they were paying huge incentives to snap up cargoes. Metal is piling up fast in warehouses around the world — with Shanghai Futures Exchange inventories hitting a record on Friday — as traders and fabricators say demand has weakened noticeably, particularly in key buyer China.

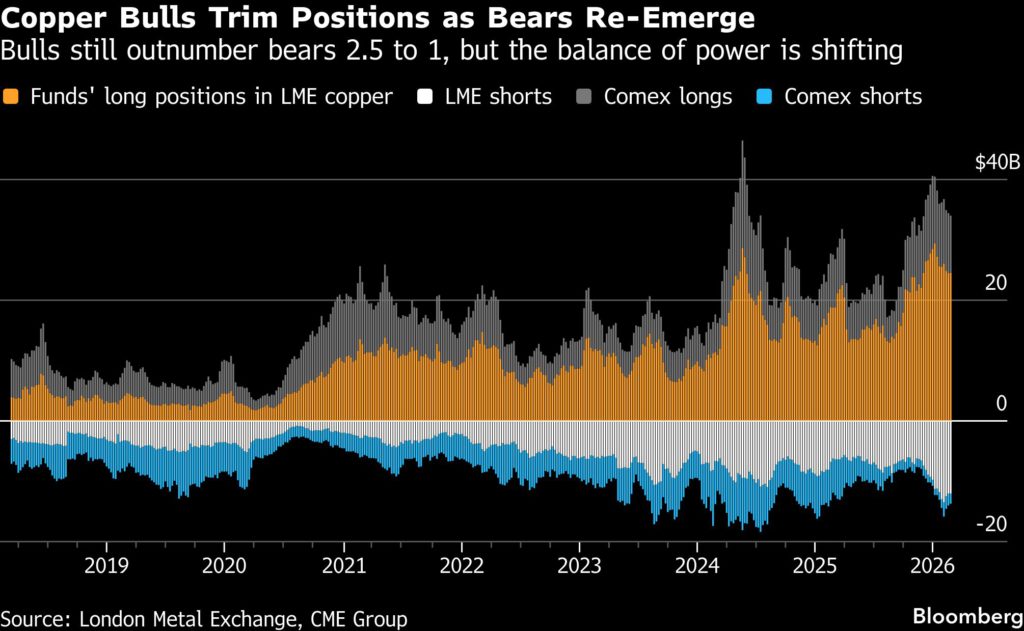

And while bulls still outnumber bears by more than two to one on exchanges in London and New York, the balance of power is starting to shift as some funds build short positions and others trim their bullish wagers after the surge in prices.

Copper is heading for a 3.7% weekly drop on the London Metal Exchange, hit by both the growing turmoil in the Middle East and a surge in deliveries into exchange warehouses that’s lifted LME stockpiles to the highest in nearly 17 months. Collectively, inventories at the world’s main exchanges have risen by more than 500,000 tons since the start of the year.

“As much as copper is a critically important industry and there is well documented underinvestment in new supply, we are in thin air right now,” said Mark Hansen, chief executive of trading house Concord Resources Ltd. “Unfortunately, any disappointments set copper up for a bear trade.”

The past year in the copper market has been one of the most turbulent in recent memory. For much of 2025, the threat of tariffs by President Donald Trump spurred a hugely lucrative arbitrage trade that drew massive volumes of metal into the US, where prices had surged far above the rest of the world.

The tariff trade has been a core driver in copper’s push to all-time highs, with prices ratcheting steadily higher as supplies outside the US have dwindled and manufacturers have been drawn into an unprecedented bidding war as cargoes have gravitated towards American ports.

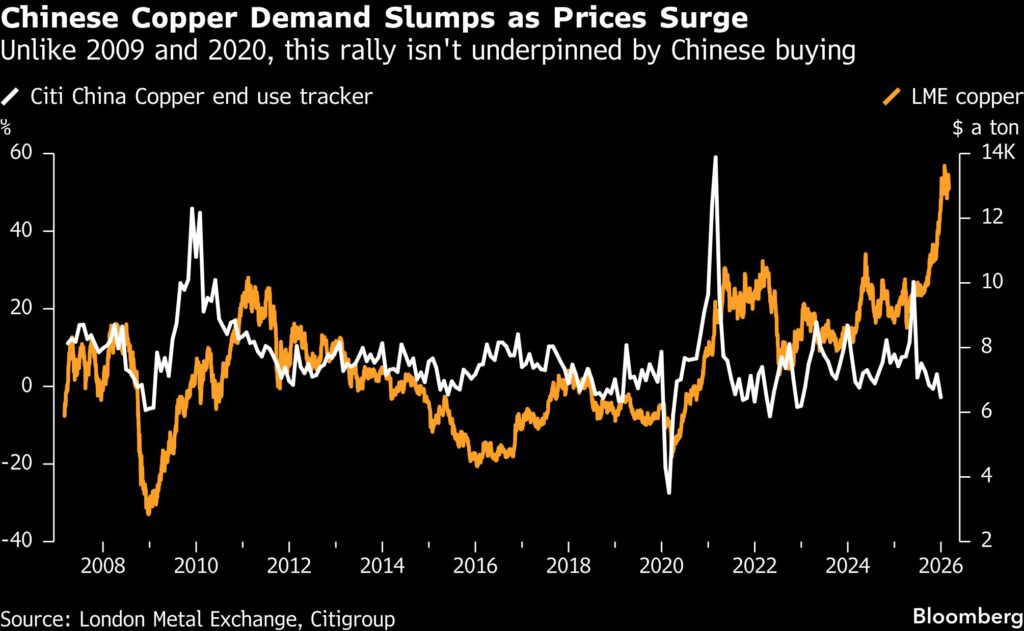

Copper bulls argued that the tariff trade would leave the rest of the world short of metal just as global supply has been squeezed by a series of mine disruptions, while also pointing to a bright long-term outlook for demand. In recent months, the price rally was supercharged by a rush into metals by Chinese investors.

Now, the economics of the US tariff trade appear to have unraveled. The premiums for US copper futures disappeared, with spot copper contracts on the LME trading roughly on par with New York’s Comex — removing the incentive to source new cargoes to ship to the US.

While Trump may yet push ahead with a plan to impose tariffs from next year, the collapse in the price arbitrage signals that a growing cohort of investors are betting he won’t — particularly after his administration in January opted not to impose broad tariffs on critical minerals.

The growing weakness in copper’s short-term fundamentals can be seen in a spike in global inventories. Privately held stockpiles in China have surged to the highest since 2016, while those on global exchanges reached the highest in more than two decades.

Mercuria Energy Group, a major actor in the tariff trade that last year predicted it would drive prices to record levels, is among the traders who have been delivering cargoes on to the LME in recent weeks, according to people familiar with the matter.

To be sure, large volumes of copper are still flowing into US ports for now, with some traders able to lock in profits under annual supply deals for this year before the arbitrage window closed. But a steep drop in the premiums that traders and manufacturers are paying to secure new tonnages reveals how the tariff trade’s magnetic pull on global supplies is ending, and negotiating power is shifting back in buyers’ favor, even as sky-high prices continue to work against them.

Adding to the strain, manufacturers in China are fighting back against the rally by curtailing purchases and seeking substitutes for the bellwether industrial metal. Simultaneously, production from the country’s vast copper smelting industry is surging, leaving sellers facing some of the toughest market conditions in decades.

And in the Democratic Republic of Congo — the top supplier behind Chile — some traders have canceled or postponed annual deals because they no longer want to pay hefty prices for them, according to Chinese consultancy Shanghai Metals Market. With producers seeking alternative buyers, their so-called equivalent-quality cargoes are selling at growing discounts to LME prices in the African market, according to people familiar with the matter.

Cutting purchases

The flurry of offers are putting significant additional strain on the global market at a time of seasonally weak demand. Last year traders including Mercuria, IXM and Trafigura diverted large volumes of African copper to the US, but now miners are returning to traditional buyers in China and Europe, where many manufacturers are cutting purchases as prices trade near record highs.

Buyers in China — which consumes half of the world’s copper — pushed back strongly as the tariff trade gathered steam and producers sought to hike their premiums to record levels in annual supply deals. Some key clients of Codelco, have turned down their $350-a-ton offer for 2026 supply to China, and several sellers have described this year’s negotiations with Chinese buyers as the hardest in decades. One top copper trader said that the spot market supply-demand balance was one of the worst he had ever seen.

“There has been more African EQ material available on the market,” said Ni Hongyan, vice general manager of Shanghai-based metals trading house Eagle Metal International Pte. “This means supply will increase, and if consumption can’t keep up, domestic discounts will widen further.”

Major fabricating mills in China, which process copper into wires, cables and rods, are trying to keep minimal inventories — citing exposure to prices and premium risks, as well as fear of weaker orders, according to people familiar with the matter. Some already saw 10% to 20% declines in orders for their products in the first quarter, with the recent surge in prices exacerbating a seasonal slump in demand seen in the run-up to Chinese New Year.

Some of their clients have also substituted copper with cheaper aluminum, most recently in the air conditioner industry, where copper can account for a third of production costs. In December, Wanbao Air Conditioning launched China’s first model of air-conditioner that does not use any copper, with the cooling tubes replaced with an aluminum-zinc alloy. Its retail price is as low as 999 yuan ($146), at least 20% cheaper than its peers.

As Chinese fabricators return from the week-long Lunar New Year holiday, demand has begun to gradually return but remains tepid, traders said, arguing that a meaningful increase would only come with significantly lower prices.

Up to now, the downturn in Chinese demand has done little to spoil the upbeat mood, with many investors and analysts betting that the mining industry’s chronic supply constraints and surging demand in data centers, electric vehicles and renewables will keep driving prices higher.

But copper bulls are now facing challenges on multiple fronts: At the macroeconomic level, the dollar is rallying and stock markets are tumbling as the Iran war intensifies, while a selloff in bond market exemplifies the growing worry that the conflict will fuel a sharp bout of inflation that will necessitate aggressive interest rate hikes. And with spot supply rising fast in the physical market, there are growing doubts about whether copper prices can hold their ground near $13,000 a ton.

“Amid higher prices, copper fundamentals have weakened with visible stocks growing as Chinese demand has gone cold,” JPMorgan analysts led by Gregory Shearer said in an emailed note last week. While the analysts said they remain positive on copper, “our conviction in a bullish trajectory for copper has taken a hit.”

Read More: China’s metals association calls for expanded copper stockpile

More News

Gold trims weekly loss as US jobs data raises Fed rate cut bets

March 06, 2026 | 01:53 pm

Peru taps fuel reserves to combat worst energy crunch in two decades

March 06, 2026 | 01:44 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments