Back at it again: An interview with Peter Breese

Legendary investor, Warren Buffett says “if a business does well, the stock eventually follows.” It is on this theme that mining executive Peter Breese has built his career.

This career which has encompassed over three decades includes the $6.8 billion and $1 billion sales of LionOre Mining and Mantra Resources, respectively.

The Zimbabwe native got his start in the mining industry working in his home country at Union Carbide (now Dow Chemical Company) where he was part of a team that helped to improve operations at one of the world’s largest ferrochrome smelting complexes and ensured some of the largest platinum mines outside of South Africa were built on time and budget.

It was during his time at Union Carbide that Breese would eventually meet his long time business partner, Colin Steyn.

After a deadly industrial disaster in India forced Union Carbide to sell its Zimbabwean mining business (Zimasco Ltd.), a group of London-based mining entrepreneurs would buy them. This group included Colin Steyn.

So Breese and Steyn’s business partnership was born.

With a successfully turned around Zimbabwean mining house formed, Steyn and Breese set out to build an international mining company. Steyn joined LionOre Mining International in 1996, raising $20 million to acquire nickel assets in Botswana and Australia. Breese stayed in Zimbabwe to finish the operational overhaul there. He would join LionOre in 2004 and help Steyn grow the company into a top 10 nickel producer, a growth trajectory which saw the company’s market cap increase from a roughly $100 million in the late 1990’s to $6.8 billion by 2007 when it was sold to Norilsk Nickel.

A 6,700% return.

Breese contended that their business model is somewhat counter intuitive, but is entirely logical.

They don’t go after the best-in-class assets. Instead they looked for mid-tier assets with conventional operating processes that have the potential to be value re-engineered into highly efficient, low cost operations.

It’s a formula that has been proven fruitful for Breese.

“Nobody sells a great asset for cheap,” he told me while he was visiting Asanko’s Vancouver office (Breese and the Asanko operations executives are based in Johannesburg).

“We look for assets we know we can implement our systems and make the operations better than the previous team was capable of doing.”

The ‘system’ Breese is referring to is a combination of Stratified Systems Theory (SST) and a clear, long term strategic plan which he claims is the key to all of their successes.

SST is an in depth “business process re-engineering methodology” that Breese says aligns the design of the core business of mining to the identified strategy.

By combining SST with under achieving mining assets, Breese and his team have been able to turn mining operations into cash cows. Time and time again.

“We’ve never really had a winning formula, we just use SST and strategic planning to unlock value by focusing on the process and realizing if you do that, success will follow.”

It was this process that led to LionOre’s success.

After a back and forth bidding war between Russian nickel behemoth Norilsk and Zug-based Xstrata that started with Xstrata in March 2007 bidding $18.50 per share and ending in May 2007 with Norilsk at $27.50, LionOre was sold for $6.8 billion cash.

“There’s nothing like competition to create a good deal,” he told me.

Prior to the initial offer, LionOre shares were trading just above $11.00 per share.

As part of the deal, Breese would join to Norilsk (the world’s largest producer of nickel and palladium) for a minimum 12 month stint as CEO of Norilsk Nickel International.

“At the end of the day it’s not good business to sell something and run. You have to standby what people are paying a lot of money for and $6.8 billion is a lot of money.”

Taking their windfall from LionOre, Breese and Steyn (and a few other investors) created Highland Park S.A. which is their investment vehicle. They quickly took control of Mantra Resources – an African uranium explorer – with a $24 million investment by Highland Park.

Shortly thereafter, Breese and Steyn implemented their SST and strategic planning processes to fast-track the development of Mantra’s Tanzanian uranium project (Mkuju River).

In 2010, just months before Fukishima, ARMZ (Russia’s nuclear holding company) came knocking with a $1.16 billion cash offer.

The board agreed and had the support of its largest shareholder; Highland Park (which owned 13.5% of Mantra).

Clean and simple, right? Not quite.

Just months after announcing their bid, ARMZ would withdraw it citing the material adverse change clause was triggered given the disaster at Fukishima. Shares in Mantra dropped over 30%.

Quickly the two parties agreed to a revised offer which would see ARMZ lower their bid to $1 billion.

It hasn’t been all roses for Highland Park however. They passively invested, in a big way, in two companies (Mirabela Nickel and Coalspur Mines) where the timing of their entrance turned out to be all wrong.

I asked him how those were different.

“There were two factors there. Firstly the commodity prices turned against us. Secondly, we didn’t run those companies, we were simply investors. You won’t see us do that again, we won’t invest unless we actively participate in running the business,” he explained.

Their next iteration is Asanko Gold. (Disclosure: I am a shareholder of Asanko).

In October 2012, Highland Park invested $32.5 million in Asanko (then Keegan) at $3.44/share. Breese was announced as President and CEO, with Steyn joining the Board who now acts as Chairman. (Mr. Steyn pictured below).

Keegan’s Esaase project was once the darling of the junior gold market. However, it fell from grace when Keegan published a 2011 pre-feasibility study showing high capex and operating costs at a time when the market was collapsing and investors were shying away from large capex spends. The stock fell from over $8.80 to $2.80 per share (70% decline) in just over 12 months. That’s roughly when Breese and Steyn came in for a 10% stake.

“Keegan was out of favour from an investor perspective, but the Company had over $200 million in the bank and a large gold resource. We did some initial value re-engineering and came up with a plan for it,” Breese said.

Immediately he and his team went to work.

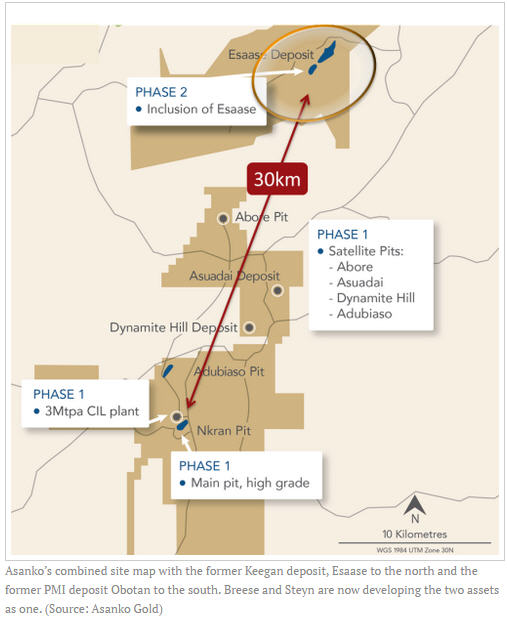

Their vision for the deposit was twofold. Firstly they reviewed the geological and mine plans and decided the deposit could be mined more selectively at a higher grade. Secondly they revisited the metallurgical flow sheet and identified capex and opex savings there too. They also identified a further opportunity, which could be a real company transformer – the acquisition of the neighbouring PMI Gold asset, Obotan, which was at the same stage of development as Esaase.

As Breese points out: “It’s rare to find true synergies in the mining industry, but if you can develop two assets at the same time, you can embed tens of millions of dollars in savings over the life of mine in both capex and operating synergies.”

A couple of months after their initial investment, Asanko would announce a merger with PMI to create a company with a clear path to 400,000 ounces of annual gold production.

But it was never going to be that easy for Asanko.

A couple of months after announcing the proposed merger, the two agreed to terminate the deal after a small but influential group of PMI’s shareholders wanted to hold out for better days.

Fast forward one year and the two companies would, indeed, successfully merge creating what is now Asanko Gold.

Today, they are just over a quarter of the way through the construction of Obotan (the former PMI asset) which is the first phase of the mine and is expected to cost US$295 million. First gold is slated for early 2016 with average annual production expected to be roughly 190,000 ounces at US$781/oz all-in sustaining cash cost, which places phase 1 in the lowest cost quartile for the industry.

A pre-feasibility study on the phase 2 development which should double production (up to 400,000 ounces annually) is expected in early Q2 2015.

Breese says that he and his operations team meets every morning, without fail, to talk.

“At 7am every morning, we all get together in the office and talk about anything and everything, whether its football or metallurgy, we talk about it.”

This dedication to communication all stems from – you guessed it – SST.

As Jimmy Carter’s Budget Director Bert Lance famously said: “if it ain’t broke, don’t fix it.”

Clearly Breese’s system is far from broken.

For more information visit Asanko Gold’s Corporate Website.

By: Travis McPherson

The information contained in this article is for informational purposes only and may contain errors. All figures in Canadian dollars unless specified. The article is not intended to provide legal, accounting, tax, investment, financial or other advice to you, and you should not rely upon the information to provide any such advice. This article is not to be construed as a form of promotion, an offer to sell securities or as a solicitation to purchase our securities. This article has been produced as a source of general information only and opinion.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments