Building more mines? The devil is in the details

Years of neglecting its critical metal supplies is finally catching up with the United States, whose government now realizes it must invest heavily in mining and manufacturing, as demand for the raw materials needed to build a new green economy that rejects fossil fuels gears up.

The problem is, this epiphany comes 20 years too late, and there are few details as to how the country will actually go about re-building its mining sector after decades of mal-investment and relying on other countries for doing the “dirty job” of mining and mineral processing.

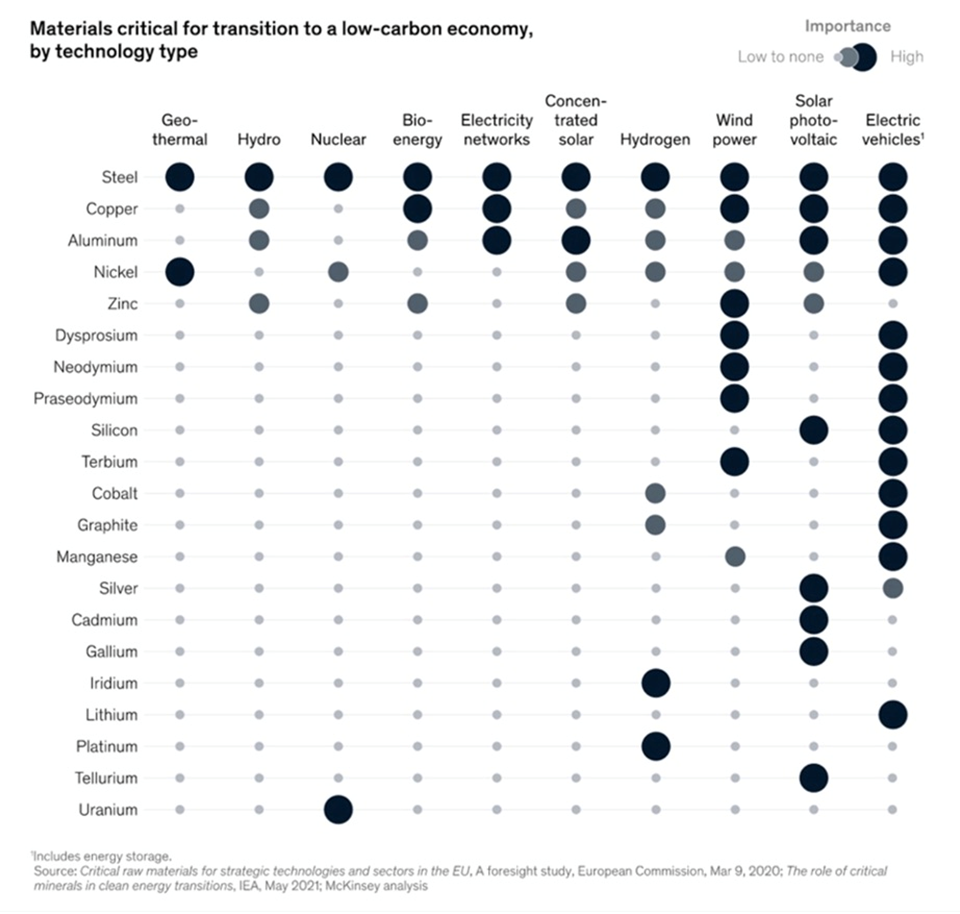

More clean energy means more solar panels, wind turbines, electric vehicles, and lithium-ion batteries, both for EVs and grid-scale storage. For some materials, like silicon, supply is plentiful, but for others, such as the rare earth neodymium for wind turbines, lithium, cobalt, graphite and nickel for batteries, and copper for just about everything involved in wiring, the supply chains will need to shift.

That’s because for most of the metals used in clean energy and electrification, the United States relies on imports.

Since Donald Trump’s presidency, the US has been planning to reverse its dependence on foreign rivals especially China, which has the largest EV market and dominates the global battery supply chain.

We weren’t paying attention when China cornered the rare earths market back in 2010 and were also blind to the Chinese locking up global supplies & processing capabilities for nickel, cobalt, graphite and lithium. About 85% of the world’s neodymium is concentrated in a few Chinese mines, and most of the world’s cobalt production comes from the politically unstable Democratic Republic of Congo. The lion’s share of palladium, used in catalytic converters, and nickel, a crucial ingredient of electric-vehicle batteries and stainless steel — is mined in Russia, which is subject to Western sanctions after invading Ukraine.

These are just a few ways to illustrate the United States’ near-total subservience to foreign critical metal suppliers.

It’s hard to imagine the US being able to fulfill the Biden administration’s new clean energy agenda without either a significant increase in critical metal imports that frankly may not be possible in current market conditions, i.e., the hostility between the United States and Russia and China, or executing a home-grown strategy to explore for and mine them in North America.

Infrastructure promises

Right now, governments are using interest rate hikes to curb inflation, which is chipping away at consumers’ purchasing power and making the cost of everything — groceries, gasoline, housing etc. — more expensive. We understand the “demand destruction” strategy — reduce spending by making the cost of borrowing higher — but it’s only addressing the consumer demand side of the equation. The formula for aggregate demand is AD = C + I + G + (X-M) where X is exports and M is imports, and AD is another term for GDP.

For the Fed’s strategy of lessening consumer demand to work, i.e., for prices to fall, any decrease in demand from C, consumer spending, cannot be offset by an increase in demand from G, government spending. Otherwise, one just cancels out the other.

Yet this is precisely what governments across the globe are planning.

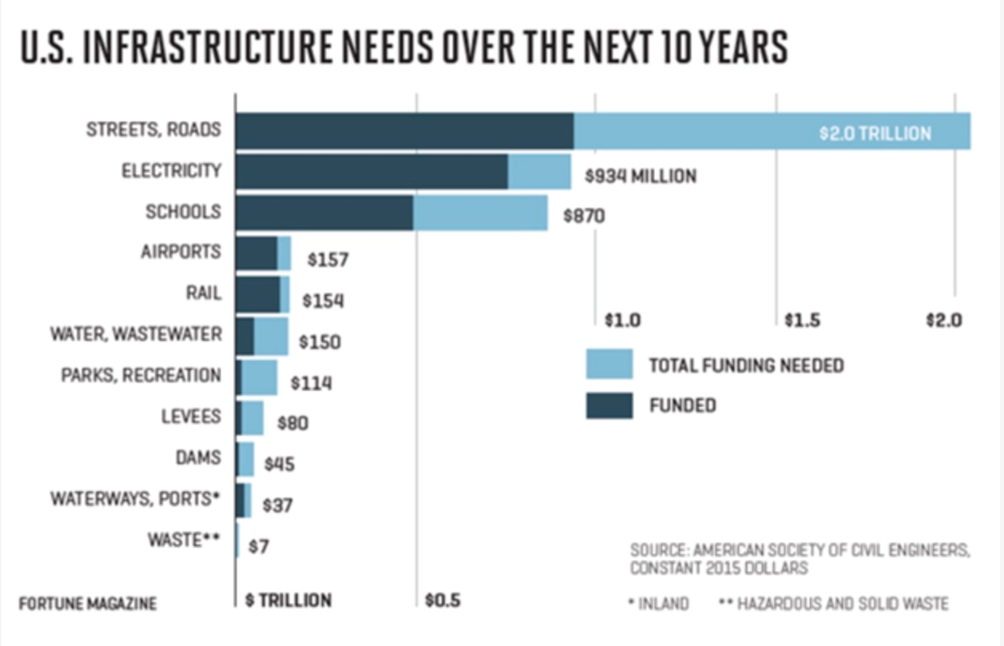

Many countries need to reduce their so-called “infrastructure deficits”. Basic infrastructure such as roads, bridges, water & sewer systems, has been poorly maintained, and requires hefty investments, measured in trillions of dollars, to repair or replace.

China, the world’s biggest commodities consumer, has committed to spending at least US$2.3 trillion this year alone, on thousands of major projects, according to Bloomberg.

“Made in China 2025” was initiated in 2015 to reduce China’s dependence on foreign technology, promote Chinese manufacturers, and to change its perception as a low-end manufacturer.

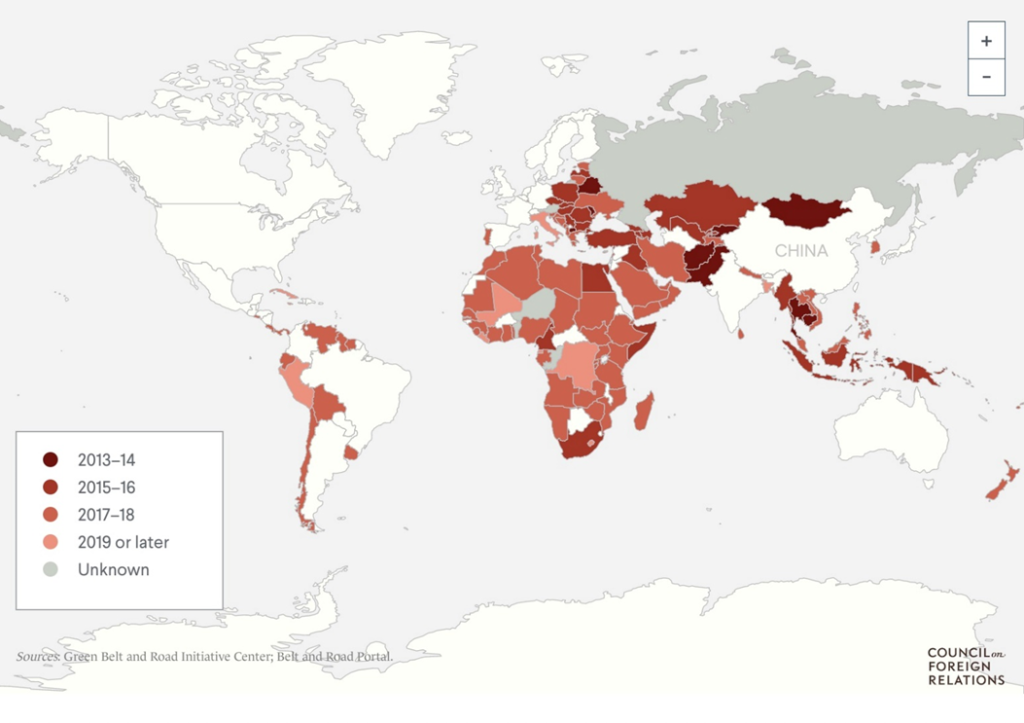

China’s $900 billion “Belt and Road Initiative” is designed to open channels between China and its neighbors, mostly through infrastructure investments. Over 130 nations have signed up to BRI, including countries well beyond its borders. They include Russia, Italy, Greece, Portugal, Hungary, Poland, Romania, Ukraine, Chile, Bolivia, Peru, Venezuela, Saudi Arabia, Iran, most of Africa, Indonesia, Thailand, Vietnam, Cambodia, Myanmar, Laos, South Korea and New Zealand.

The G7 just unveiled $600 billion to counter China’s Belt and Road. The United States has committed $200 billion in grants, federal funds and private investment over five years, with Europe pledging $316 billion and Japan promising $65 billion.

The United States is also pursuing its own $1.2 trillion infrastructure package, to be spent on roads, bridges, power & water systems, transit, rail, electric vehicles, and upgrades to broadband, airports, ports and waterways, among many other items.

Extensive minerals required

For such plans to work, extensive minerals are needed to build the required infrastructure, and will have to compete with one another (plus every other country) to do so, driving commodity prices higher.

The Infrastructure Investment and Jobs Act is the largest expenditure on US infrastructure since the Federal Highways Act of 1956. Rolled out over 10 years, it includes $550B in new spending. According to S&P Global, Among the metals-intensive funding in the legislation is $110 billion for roads, bridges, and major projects, $66 billion for passenger and freight rail, $39 billion for public transit, and $7.5 billion for electric vehicles.

In particular the spending package, signed into law on Nov. 15, 2021, is expected to be a boon to domestic steel and aluminum production. The American Iron and Steel Institute (AISI) estimates that every $100 billion invested in infrastructure, could increase demand for US steel by up to 5 million tons.

The infrastructure bill should also significantly boost domestic aluminum consumption that is already accelerating due to the “light-weighting” and electrification industrial trends, states S&P Global. For example, aluminum is widely used in the electrical grid, which will receive $65B as part of the legislation.

An extension of the infrastructure buildout is the global transition towards a “green economy”, which can only be accomplished with renewable power, electric vehicles and energy storage technologies.

All of these require lots of minerals. The amount of raw materials we’ll need to extract from the Earth to feed this transition is staggering.

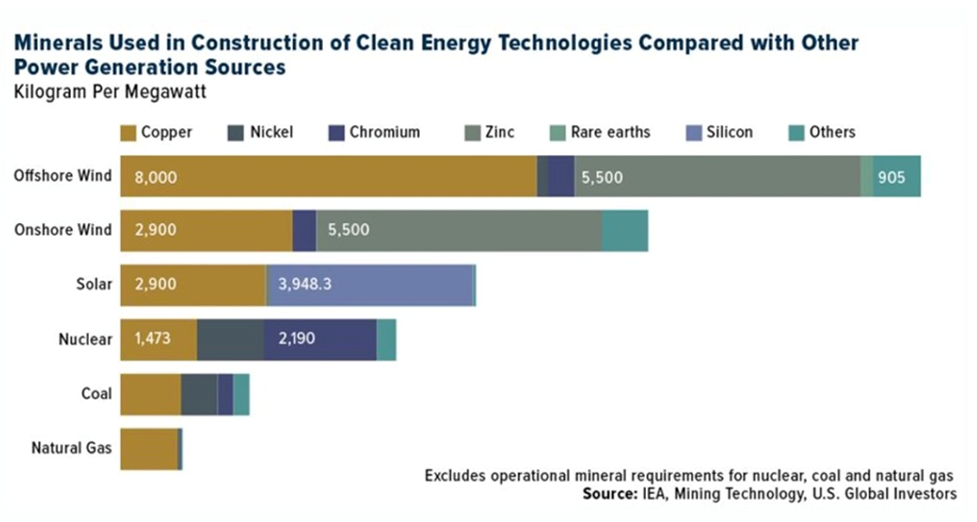

EVs require, on average, six times the amount of minerals such as nickel, copper, cobalt and lithium, as traditional gas-powered cars. According to the International Energy Agency (IEA), an offshore wind farm uses nine times as many resources as a natural gas plant, with 8,000 kg of copper needed to produce just one megawatt of power (1GW = 1,000MW)

All in all, Bloomberg New Energy Finance estimates that the global transition will require about $173 trillion in investments over the next three decades; every commodity under the sun will be gobbled up.

The Fed and governments working at cross-purposes

The US Federal Reserve’s objective of raising interest rates is to cool demand, in an economy where, for several months now, demand for goods and services has outpaced supply, causing the highest inflation in 40 years.

However, the Fed can raise rates as high as they want, the problem is they are not going to magically increase the supply of a number of commodities and manufactured goods we are running short of.

A big part of the current inflationary cycle, the worst since the early 1980s, is “supply-side” inflation. This has nothing to do with killing demand, and everything to do with increasingly supply.

In fact the Fed’s mandate of raising interest rates to “destroy” demand, is running up against the policy of several governments around the world who are committed to upgrading their aging infrastructure and fulfilling a massive shift to electrification and decarbonization, so-called “green infrastructure” investments. (read more here)

And the demands on governments keep increasing. Decarbonization & electrification, rectifying countries’ “infrastructure deficits”, and attempting to address the widening gap between rich and poor, are just three demand drivers likely to push government spending and therefore inflation higher.

In sum, when you think about all that is happening to pressure prices — climate change; resource nationalism; NIMBYism regarding new mines in North America & Europe, lower ore grades and poor metallurgy; decarbonization & electrification, hundreds of new mines required to meet battery metals’ demand; malinvestment in mining and oil and gas; money-printing “out the wazoo” to cover annual deficits and government bond purchases (QE), all the pandemic-related stimulus payments to Americans; and the trillions in promised new spending, that hasn’t yet been factored into inflation — there is no way that the Fed is going to have an impact on inflation. How can it?

The Federal Reserve does not seem to understand, or care, that constantly raising interest rates will do very little to stop inflation if measures aren’t also taken on the supply side.

I’m talking about more mining to address metals shortages, more manufacturing to create real, high-paying jobs, and figuring out where to farm to get decent yields crop without destroying the environment — an issue of increasing importance as the global food crisis continues.

Positive developments

In fairness, the US and Canadian governments have recently shown an interest in addressing the lack of domestic mining in North America, and what can be done to limit dependence on foreign suppliers of critical minerals.

For years neglected by governments, critical minerals like graphite and lithium are finally getting the attention they deserve. In June, the Canadian government unveiled its low-carbon industrial strategy, that will see Ottawa partnering with each province to “identify, prioritize and pursue opportunities”. This means battery manufacturing in Quebec and electric vehicle production in Ontario.

Natural Resources Minister Jonathan Wilkinson pointed to CAD$3.8 billion earmarked for critical minerals in the April budget. On top of that, “we have a billion and a half dollars in the Clean Fuels Fund, we have eight billion dollars in the Net Zero Accelerator, we’re setting up the Clean Growth Fund, we have the Canada Infrastructure Bank,” Bloomberg quoted him saying. He added:

“The average mine takes 15 years to bring into production. In the context of the energy transition, we don’t have 15 years if we’re actually going to provide enough of the minerals to be able to support just the battery development. So it behooves us to bring everybody into the room to figure out how to do it.”

At AOTH, we couldn’t agree more. Canada’s new industrial strategy dovetails with what is happening south of the border.

The US, which has long sought to improve its battery supply chain, recently invoked its Cold War powers by including lithium, nickel, cobalt, graphite and manganese on the list of items covered by the 1950 Defense Production Act, previously used by President Harry Truman to make steel for the Korean War.

To bolster domestic production of these minerals, US miners can now access $750 million under the act’s Title III fund, to be used for current operations, productivity and safety upgrades, and feasibility studies. The DPA could also cover the recycling of these materials.

Later this year, the Department of Energy will begin doling out over $7 billion in grants for battery production, nearly half of which are earmarked for domestic supplies of materials and battery recycling. The DOE has also committed $45 million in funding for battery development called the Electric Vehicles for American Low-Carbon Living program. It’s all part of the Biden administration’s goal of making half of all new vehicles sold in the United States electric by 2030.

The administration has also allocated $6 billion as part of a huge infrastructure bill aimed at developing a US battery supply chain and weaning the auto industry off its reliance on China. In a July 2021 report, the White House said the number of mineral commodities for which the US is reliant on imports for more than a quarter of demand, has jumped to 58 from 21 in 1954.

In summary, there have been some positive developments by officials at the highest levels of government in Canada and the United States, to facilitate the building of battery cells, electric vehicles and charging infrastructure, and to incentivize EV purchases with generous subsidies.

What’s missing is any concerted effort to support the mining of minerals deemed necessary for the electrification and decarbonization agendas being vigorously pursued by both countries.

Obstacles to mining

$750 million is a good start, but it’s not nearly enough to accomplish the domestic mine-building of the scale needed to reduce our dependence on foreign suppliers, and to lessen the coming deficits of key battery/ energy metals such as graphite, lithium, nickel and copper. Three quarters of a billion might pay for one or two mines; we need dozens of mines.

The National Mining Association followed up the Defense Production Act news by stating that changes to the act will do nothing to ease mining permit bottlenecks.

“Unless we continue to build on this action, and get serious about re-shoring these supply chains and bringing new mines and mineral processing online, we risk feeding the minerals dominance of geopolitical rivals,” association President Rich Nolan wrote in an email to Bloomberg. “We have abundant mineral resources here. What we need is policy to ensure we can produce them and build the secure, reliable supply chains we know we must have.”

The mining association said the country should take steps to streamline the process and put it on par with Canada, including reducing duplication between state and federal governments for approvals and setting specific deadlines.

In fact, the Biden administration has come out against domestic mining through a number of anti-extractive industry decisions, while it supports cleaner EV manufacturing and auto-assembly.

The Democratic Party’s aversion to mining is, at least partially, a reflection of the American public’s reluctance to accept mining as part of the country’s future.

So, instead of building a “mine to EV” supply chain, Biden and his Democrats want to skip the mining and go straight to the cleaner, manufacturing-intensive electric vehicle-building, that will supposedly bring plenty of jobs.

A Reuters story claims the United States has enough reserves of lithium, copper and other metals to build millions of its own vehicles, but opposition to new mines may force the country to rely on imports that could delay efforts to electrify its roughly 275 million cars and trucks.

Arguably, if electrification is delayed due to metals supply problems, Biden’s administration have only themselves to blame.

The United States has plenty of EV metals but the White House and Congress have chosen not to tap them.

“If we don’t start getting some mining projects under construction this coming year, then we will not have the raw materials domestically to support EV manufacturing,” said Reuters quoting an executive at a company developing a US lithium-boron deposit.

Among the mining projects facing opposition from indigenous groups, ranchers or environmentalists, are:

- The Thacker Pass lithium project in Nevada. A judge last September denied a request by native Americans to halt excavation at the mine site over concerns it may host ancestral bones and artifacts. This year, federal judges will rule in separate cases whether mine approvals granted by former President Trump should be reversed.

- Another lithium project, in North Carolina, is facing pushback from local landowners that could cost Piedmont Lithium necessary local zoning approvals.

- State regulators in Minnesota are weighing whether permits issued to Polymet Mining, controlled by Glencore, should be revoked or re-issued. The North-Met project would be Minnesota’s first copper-nickel mine.

- Biden himself took steps to block Antofagasta’s Twin Metals copper and nickel project in Minnesota, with the US Forest Service last October proposing a 20-year ban on mining in the Boundary Waters region. The Chile-based company appealed the decision which it called politically motivated, since Biden aimed to shore up support with environmentalists and counter his earlier commitments to allow more domestic mining. Earlier this year the Biden administration effectively canceled two long-standing mineral leases at the Twin Metals mine.

- The massive Pebble deposit of Northern Dynasty has been halted because of environmental concerns.

Along with siding with, or not going against, mining opponents, the Biden administration is also practising resource nationalism by trying to exact a larger piece of the metals pie.

Last September a congressional committee added language that would set an 8% gross royalty on existing mines and 4% on new ones.

There would also be a 7-cent fee on every ton of rock moved. According to a Reuters story the proposal would mark one of the most-substantial changes to the law that has governed U.S. mining since 1872 and could raise about $2 billion over 10 years for federal coffers…

Executives say Biden’s goal to have 35% of U.S. electricity generated by solar panels – up from 3% today – would be all but impossible without new mines.

Note: the United States already has very strong environmental protections through the National Environmental Policy Act (NEPA).

Infamously, the act can require seven to 10 years to secure a US mine permit, compared to two years in countries with similar regulations like Australia. Thus it is no surprise that mining companies with a choice to mine domestically or abroad, would choose the latter.

In Canada, Bill C-69 is an example of legislation passed by a government that has the ear of special interests. Bill C-69 broadens the scope of the assessment process and adds more consultation with the public and particularly indigenous groups.

Such anti-mining legislation can present a significant obstacle to companies trying to move a project forward to production, and in the worst of cases, drags the process out so many years that the economics no longer work and the mine is shelved.

This often happens in North America, where it can take up to 20 years to move a project from discovery to commercial production. A preliminary economic assessment done in year 3 is of little use if the minerals aren’t produced until year 20.

A Fraser Institute report found that Canadian mining jurisdictions lagged their international competitors for increases in the time for permit approval, transparency and confidence that permits will be granted.

Special interest groups tend to treat all mining as having the same destructive effect on the environment. They don’t differentiate between mining for metals that are on the way out (like coal) and say, copper and nickel, metals that are highly in demand, where the benefits of extraction could, depending on location, outweigh the effects of some ground disturbance.

In response to anti-mining sentiment among some sectors of the population, resource companies are trying harder to make their operations less carbon-intensive and are ensuring that they adhere to more stringent environmental, social and governance (ESG) criteria.

Miners are finding that institutional investors are pressuring them to show they are investing in solutions, not problems.

Companies that proactively address the issues that investors want them to look at may see a lower cost of capital, but this must be weighed against the implementation of ESG solutions which add to a miner’s cost per tonne or ounce.

Reality check

Notwithstanding efforts by the Canadian and US governments to promote mining, especially the extraction of critical minerals needed for the new green economy, there remains a deep divide between what it will take, and reality.

In a recent column, Michael Goehring, the president and CEO of the Mining Association of British Columbia, wrote that without mining and minerals, decarbonizing the global economy and achieving net zero is impossible. Full stop.

That may seem self-evident after all that we’ve discussed, but it’s interesting to read that despite nearly 200 countries signing the 2015 Paris Accord to reduce their emissions, policy makers are only beginning to focus their attention on whether we will have enough minerals and metals to meet net zero by 2050.

Goehring quotes the International Energy Agency’s (IEA) eye-opening study last year warning that the world needs to significantly increase the supply of metals that are essential to clean technologies. We’re talking about up to six times more than what we’re producing today.

“Today, the data shows a looming mismatch between the world’s strengthened climate ambitions and the availability of critical minerals that are essential to realizing those ambitions. The challenges are not insurmountable, but governments must give clear signals about how they plan to turn their climate pledges into action,” the IEA’s executive director Fatih Birol pointed out.

In another recent report, specific to copper, S&P Global predicts a global supply deficit of approximately 10 million tonnes of copper by 2035. This shortfall is equivalent to the production of 76 Highland Valley Copper mines, Canada’s largest copper mine.

“Simply put,” Goehring concludes, “we are not bringing enough new mines or expansions into production fast enough to produce the minerals and metals required to meet our climate commitments by 2050.” To accelerate mining in British Columbia, he advocates timelier permitting process for mines, addressing the shortcomings of our carbon pricing system and more investment in geoscience.

(The problem of taking a very long time for mines to be built is particularly acute in BC. The first two mines to open after the BC Liberal government took power in 2001 on a promise to reinvigorate the province’s mining industry, were Mount Milligan (2013) and Red Chris (2015). Now-defunct Placer Dome tried to develop Mount Milligan in the 1990s when an NDP government was in power, while Red Chris was nearly 60 years in the making.)

But it’s not much better state-side.

Reuters recently reported that mining companies in the United States will struggle to meet a deadline for sourcing key minerals, as set out in a bill signed into law on Tuesday.

The Inflation Reduction Act provides $369 billion to fund energy and climate projects aimed at reducing carbon emissions by 40% in 2030. The bill, states Reuters, includes a $7,500 tax credit for new electric vehicles, but to win the full credit, EV makers have to source in 2023 at least two-fifths of battery materials from the United States or free trade agreement (FTA) partners such as Canada, Chile and Australia or recycle it in North America.

The guidelines… increase the material sourcing target to 80% by 2026.

Note what is being implied here. The United States wants to increase domestic manufacturing of electric vehicles but it doesn’t wish to mine the raw materials. The White House said last year it would rely on allies like Canada and Australia to secure the minerals needed for EV batteries, noting that the country “cannot and does not need to mine and process all critical battery inputs at home.”

Canada, eh? We just showed it can take up to 60 years to build a new mine here, given the ridiculous amount of red tape a mine developer must wade through, such as duplication of federal and provincial permitting. Few mines take under 20 years to reach production.

Australia is an option but it’s a long way from the nearest US port. In most cases the transportation costs of bringing in raw or processed ore would be prohibitively expensive to end users.

The United States under the Democrats are anti-mining and like in Canada, there is duplication between state and federal governments when it comes to mining approvals.

Even those in the mining industry under-estimate how long it takes. A recent Reuters story quotes Simon Moores, the CEO of Benchmark Mineral Intelligence, stating that “Considering it takes seven years to build a mine and refining plant but only 24 months to build a battery plant, the best part of this decade is needed to establish an entirely new industry in the United States.”

In what universe does Moores think it takes seven years to build a mine in the US? Like in Canada, it’s 10 to 20, probably more, by the time all the i’s are dotted and t’s are crossed, and all the interested parties have their say for and (mostly) against.

As for constructing new critical mineral mines, the US government is seemingly all talk and no action. On Aug. 10 Metal Tech News reported the Department of Energy is asking for public input into a $675 million program “to address vulnerabilities in the domestic critical minerals supply chain.”

So let me get this straight. The US is 20 years behind China in sourcing not just critical minerals but important industrial minerals like copper, iron ore, aluminum, and the like, yet it will waste nearly three quarters of a billion dollars to find out what we at AOTH already know: that China is “eating our lunch” when it comes to critical minerals.

The article goes on to say that the DOE “has a comprehensive strategy to increase domestic raw materials production and manufacturing capacity.” If it already has a strategy, why does it need to spend $675 million for public input?

It was also amusing to read that “the $675 million Critical Materials Research Program will expand on the department’s decade-long history of investment in critical materials supply chains.”

May we remind our readers that, far from investing in critical materials supply chains, the US government has let other countries do the work. The obvious example is when, in the 1980s, the US ceded its control of rare earths mining to China. As for how America lost the plot on rare earths, we previously wrote that, within two decades, the Chinese filled the void left by US rare earth mining with gusto – establishing the world’s largest rare earth research facility; filing the first rare earth patent in 1983 and over the next 14 years filing more patents than the US which had been working on them since 1950; and acquiring US technology in metals, alloys, magnets and rare earth components.

China wouldn’t have been able to develop its REE industry if it wasn’t for the dubious acquisition of Magnequench, a division of General Motors established in 1986.

For the fascinating story of how Magnequench and its technology was ceded to the Chinese, read a 2006 article by Jeffrey St. Clair.

Since then, rare earth metals, alloys and magnets needed by US defense contractors come either directly or indirectly from mostly China. According to the US Geological Survey, the United States relies on Chinese imports for at least 20 minerals, including rare earths.

Unintended consequences

There are currently about 12 million electric vehicles on global roads compared to 1.4 billion vehicles run on internal combustion engines (ICEs).

The world’s brightest minds not only have to come up with a plan to transition from ICEs to EVs, but how to fill all those new batteries with energy that is green, i.e., non fossil-fueled. Otherwise, the shift to electrification will have no net reduction of greenhouse gases.

Unfortunately, the events of the past few months have shown that it only takes a regional war in Europe to completely de-rail plans for decarbonization, as EU countries scramble to replace natural gas imports from Russia, and the prices of oil, natural gas and coal soar.

Many countries will continue to require huge amounts of coal, oil and natural gas. Europe, supposedly on the leading edge of “green”, relies heavily on Russian gas for electricity, heating and cooling. Japan, which has no natural resources of its own, in 2020 imported the majority of its oil from Saudi Arabia. And Australia, despite being a mining powerhouse (coal, iron ore), will by 2030 be 100% reliant on imported petroleum, due to the ongoing closure of its refineries.

Our addiction to oil means that hybrid vehicles, obviously requiring gasoline, are expected to continue outpacing electrics for years. The focus of government policies on electrification and renewables, at the expense of investment in traditional oil and gas, will keep the latter’s prices elevated, and the balance sheets of oil and gas companies fat.

Even coal, the red-headed stepchild of the fossil fuel family, is making a comeback. Bloomberg recently reported that despite the world being in the grips of a climate crisis as temperatures soar and rivers run dry, it’s never been a better time to make money by digging up coal.

The energy market shockwaves from Russia’s invasion of Ukraine mean the world is only getting more dependent on the most-polluting fuel. And as demand expands and prices surge to all-time highs, that means blockbuster profits for the biggest coal producers…

Ironically, those efforts have helped fuel coal producers’ success, as a lack of investment has constrained supply. And demand is higher than ever as Europe tries to wean itself off Russian imports by importing more seaborne coal and liquefied natural gas, leaving less fuel for other nations to fight over. Prices at Australia’s Newcastle port, the Asian benchmark, surged to a record in July.

Dump renewables

Coal use in the United States has dropped considerably over the years but it still burned 546 million tons in 2021, representing a tenth of total energy consumption, according to the US Energy Information Administration (EIA).

In Canada, despite a plan by the federal government to quit burning and exporting thermal coal by 2030, requests have been made by two provinces to keep their coal plants operational for another decade. Global News reported that Nova Scotia is negotiating an agreement in principle with Ottawa to keep its coal-fired electricity plants open until 2040. New Brunswick made a similar request of the feds. Coal is also burned for power in Alberta and Saskatchewan, although Alberta is on track to phase it out by 2023, Global News said.

Coal use, of course, is being driven by a huge increase in natural gas prices, with power plants sourcing coal as a cheaper alternative.

Trouble is, we’ve been so focused on expanding renewable energy, before it can actually replace fossil fuels, that we have virtually guaranteed oil, gas and coal prices will stay high for the foreseeable future.

As for the long-term, we obviously don’t know to what extent renewables will replace fossil fuels and nuclear power (nobody else does either), but we have a hard time believing it will exceed 40% and we don’t think it will ever reach 100%.

In a previous article we crunched the numbers, an edited version of which appears below.

If we get rid of all fossil fuels — oil, NG and coal — in 20 years, we need to generate an additional 134,838,220 GWh of renewable energy.

1 gigawatt hour (GWh) = 1,000.00 megawatt hours (MWh).

A large solar farm would be 500 megawatts (MW), keeping in mind that the biggest solar farm in the US, the Topaz/ Desert Sunlight, is 550MW, the biggest in the world is 1,547MW; most solar farms in the US are much smaller, less than 5MW).

Let’s say it is able to operate half the time, or 182 days. 500MW x 24 = 12,000 MWh x 182 = 2,184,000 MWh. 134,838,220,000 MWh divided by 2,184,000 = 61,739 500MW solar farms.

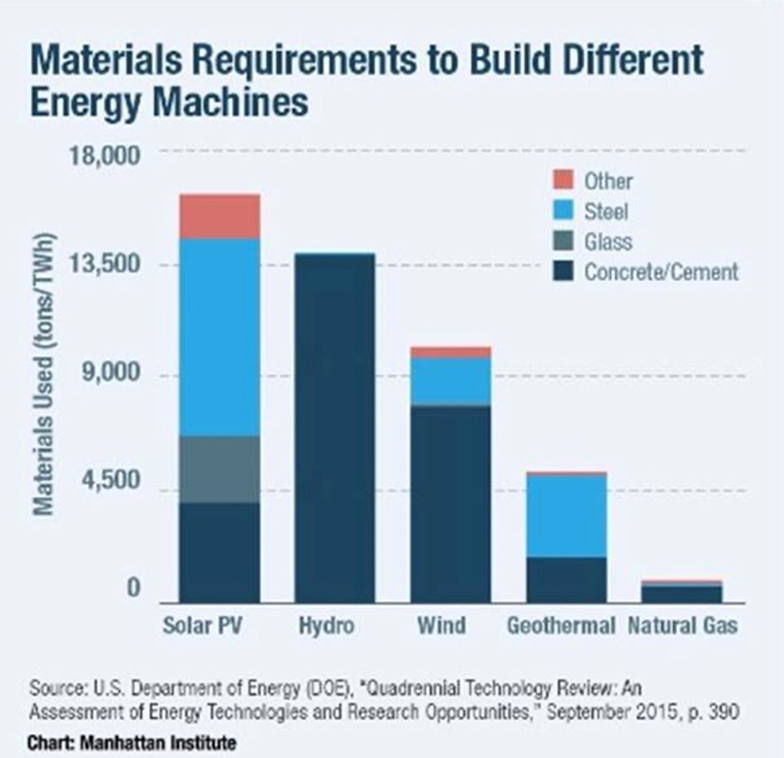

What does this mean for materials? We know that a 500MW solar conversion plant would cover 65 to 130 square kilometers with 17,500 tons of aluminum, a million tons of concrete, 3,750 tons of copper, 300,000 tons of steel, 37,500 tons of glass, and 750 tons of other metals such as chromium and titanium — 500 times the material needed to construct a nuclear plant of the same capacity.

The amount of aluminum and copper needed to build that many solar farms is off the charts:

- 17,500 tons aluminum x 61,739 (500MW) solar farms = 1,080,432,500t @ 64 million tonnes (MT) global production (2019 USGS) = 1,080,432,500 tonnes aluminum required or 16x global production

- 3,750 tons copper x 61,739 (500MW) solar farms = 2,321,521,250t @ 20Mt global production (2019 USGS) = 2,321,521,250 tonnes copper required or 11.5x global production

But it’s not only the amount of materials, but the land, that would have to accommodate the more than 61,000 new solar farms. A study by Denholm and Margolis calculated the per capita solar footprint per person, based on the assumption that electricity needs in each state are met by solar power alone. Using an average of 200 square meters per capita, extrapolated to the population of the whole country, of 328.2 million, gives a figure of 65,640 square kilometers of land required for solar energy — a size roughly equal to the size of Nevada. Not taken into consideration is the amount of land needed to fit renewable energy storage batteries.

Is wind power any more feasible? The 10 largest wind farms in the world range from 630 megawatts to 20 gigawatts. Taking a 500MW wind farm, to facilitate a comparison between solar and wind, the Manhattan Institute estimates that replacing the output from a single 100MW natural gas-fired turbine, would require at least 20 wind turbines, each about the size of the Washington Monument, occupying 25 square kilometers of land. Upsizing that to 500MW would thus require 100 wind turbines, on 125 square km. That’s just for one wind farm equivalent in size to a natural gas or solar plant.

How many wind farms would be required to produce 134,838,220 GWh of electricity, the amount needed to replace fossil fuels? A 2MW wind turbine with a 25% capacity factor (the actual output over a period of time as a proportion of a wind turbine’s capacity), due to intermittency, can produce 4,380 MWh in a year. Upsizing this to 500MW = 1,095,000 MWh. 134,838,220,000 MWh divided by 1,095,000 MWh = 123,139 wind farms @ 500MW each.

To replace about 20% of Canada’s power generation that is still from combustible fuel sources, the country would need four times as many wind farms as today. Finding space for that many, a total of 46,800MW of nameplate capacity, would require 26,676 square kilometers. This is the size of five Prince Edward Islands, or around half of Nova Scotia. Remember this is just to replace 20% of Canada’s electricity still generated from fossil fuels.

Consider that in the United States, around 63% of its power still comes from coal, oil or natural gas. According to the EIA, replacing the 966 TWh generated from coal in 2019, would require 344.6 GW of wind farm capacity, spread over 200,000 square kilometers! (about the size of Nebraska)

How about materials? According to a report from the National Renewable Energy Laboratory, wind turbines are predominantly made of steel, fiberglass, resin or plastic (11-16%), iron or cast iron (5- 17%), copper (1%), and aluminum (0-2%). This isn’t counting the electrical system, which uses copper and rare earths such as dysprosium and neodymium.

A single 2MW wind turbine weighing 1,688 tons, comprises 1,300 tons of concrete, 295 tons of steel, 48 tons iron ore, 24 tons fiberglass, 4 tons each of copper and neodymium, and .065 tons of dysprosium. (Guezuraga 2012; USGS 2011).

The Manhattan Institute estimates that building a 100MW wind farm would require 30,000 tons of iron ore and 50,000 tons of concrete, along with 900 tons of non-recyclable plastics for the large blades. The organization says that for solar hardware, the tonnage in cement, steel and glass is 150% greater than for wind, to get the same energy output.

According to The Institute for Sustainable Futures at the University of Technology Sydney, Australia analyzed 14 metals essential to building clean tech machines, concluding that the supply of elements such as nickel, dysprosium, and tellurium will need to increase 200–600%.

If BP is correct in its outlook that in two decades, renewables are going to supply the equivalent amount of electricity currently generated by coal and gas combined, we have a problem, Houston. First of all, just replacing the current amount of energy demanded by coal and natural gas, let alone the inevitably higher figure in 2040, with solar and wind would be nothing short of miraculous. Our research shows that it would mean over 60,000 solar farms and more than 120,000 wind farms. In all it’s about a 450% increase in renewables.

Of course, solar and wind farms can’t be located just anywhere. They need to be in the right locations, where the winds are strong and frequent, areas that get a lot of sunshine, and close enough to power lines to be economical.

We already know that we don’t have enough copper for more than a 30% market penetration by electrical vehicles. Building renewable energy capacity is over and above supplying the ever-growing marketplace for EVs. How are we going to get enough solar and wind to produce a minimum of 134,838,220 GWh (that’s for 2019, it could be double by 2040), if we are to replace fossil fuels in 20 years?

And even if we could, how are we going to find the raw materials? For solar power we are talking about finding 16 times the current annual production of aluminum, and 11 times the current global output of copper. Up to six times the current production levels of nickel, dysprosium and tellurium are expected to be required for building clean-tech machinery. Good luck!

Even if the mining industry could identify and produce this amount of metals to meet the world’s goal of 100% decarbonization, the supply shortages guaranteed to hit the markets for each would make them prohibitively expensive. It’s just supply and demand.

By all means, let’s electrify, but let’s produce the extra energy with nuclear, preferably driven by thorium instead of uranium, and let’s dump the mega-raw-materials-consuming solar and wind.

Not only are solar and wind inappropriate for base-load power, because their energy is intermittent, and must be stored in massive quantities, using battery technology that is still in development, they don’t have anywhere near the energy intensity provided by fossil fuels, or nuclear. (read more)

Conclusion

Driven by the need to decarbonize due to increasingly apparent climate change, governments around the world right now are choosing to de-invest from oil and gas, and instead are plowing funds into renewable energies even though they aren’t yet ready to take the place of standard fossil-fueled baseload power, i.e., coal and natural gas.

We have seen this foolish endeavor playing out in Europe, where natural gas prices hit records due to gas plants being shut down as well as nuclear plants shelved, such as in Germany and France.

The supply chain for batteries, wind turbines, solar panels, electric motors, transmission lines, 5G — everything that is needed for a green economy— starts with metals and mining. Demand for lithium, nickel and graphite on the battery side and copper on the energy side is expected to rise rapidly.

In fact, battery/ energy metals demand is moving at such a break-neck speed, that supply will be extremely challenged to keep up. The demand now, and in the foreseeable future, will continue to rise, as governments around the world execute plans to replace aging infrastructure like roads & bridges, and invest trillions of dollars in renewable energies, electric vehicles and grid-scale energy storage.

If governments decide that they need to spend colossal amounts of money on combating climate change through electrification and decarbonization, to wean themselves off fossil fuels, there will be a direct demand for more minerals.

These expenditures are inflationary and in the short term will clash with the current mandate of central banks to crush consumer demand as a way of bringing down unreasonably high inflation. It’s a battle that I believe will be won by government infrastructure spending.

On the other hand, without a major push by producers and junior miners to find and develop new mineral deposits, glaring supply deficits are going to beset the industry for some time.

Either way, we are looking at elevated prices for critical metals and certain industrial metals that are central to the new green economy, like copper and aluminum, for years if not decades to come.

(By Richard Mills)

More News

Lynas, South Korean magnet maker sign deal for Malaysia factory

July 06, 2026 | 04:52 pm

Vale chairman Stieler pushed out by pension fund

July 06, 2026 | 04:40 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments