China’s grip on copper sets scene for make-or-break supply talks

A pricing mechanism underpinning the global copper-processing industry faces a major stress test this week, with negotiations coming to a head at a time when geopolitical tensions are running high, metal is limited and China’s dominance has left smelters elsewhere struggling to survive.

Tensions have been building for years, fueled by a rapid expansion of metal-processing capacity that has outpaced mined production. That’s now prompting questions over the entire benchmarking structure, a longstanding process under which major miners strike a deal with China’s smelters, and the rest follow suit.

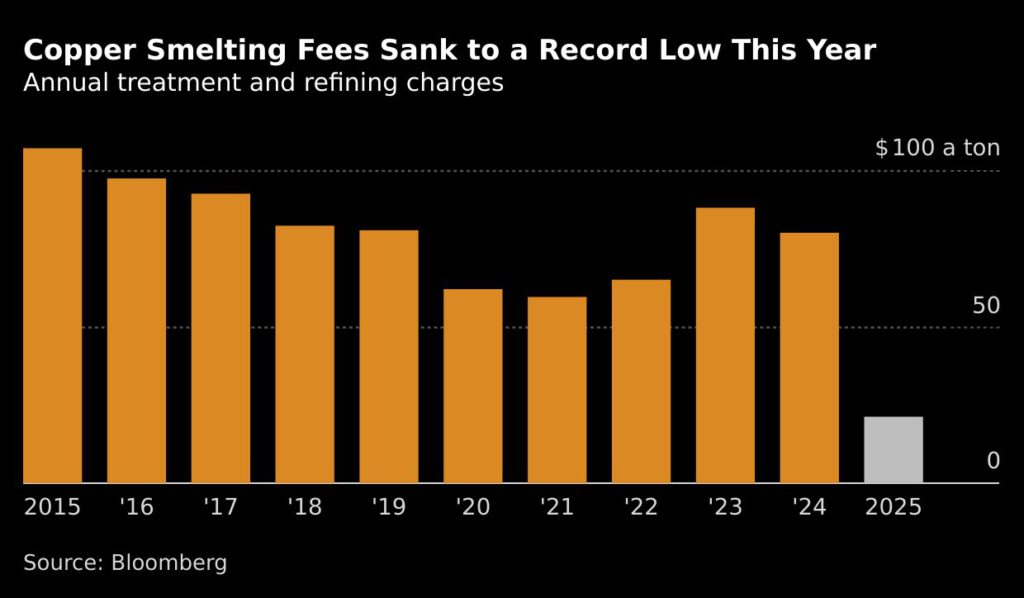

The crunch point may come during a major industry gathering in Shanghai over the coming days, which serves as a backdrop to annual discussions. Miners are expected to push for even tougher supply terms for 2026, after a year when annual treatment and refining charges — or TC/RCs — crashed to a record low.

A “further breakdown” of the annual benchmark system is expected, said Craig Lang, an analyst with CRU Group. One-on-one talks could mean more bilateral agreements — possibly at different levels to the Chinese annual benchmark — or caps and floors on TC/RCs, or even quarterly pricing, he said.

At the heart of the tensions is China, where the copper industry has continued to expand even as annual fees plunge and spot charges turn negative, meaning processors are effectively paying miners to process ore. While some smelters in China have racked up large profits this year, there have been closures in the rest of the world.

There’s already been a push among non-Chinese players for better terms. Japanese smelters are joining forces to flex their bargaining muscle and ride out conditions that one producer, Mitsubishi Materials Corp., said have “significantly deteriorated.” Last month, the industry ministries of Japan, South Korea and Spain issued a joint statement criticizing punitive TC/RCs and what they called “policies and practices that may not reflect fair market dynamics.”

For much of the past decade, TC/RCs have swung in rhythm with supply and demand. But what began last year as a temporary squeeze in copper concentrate supply has evolved into a structural shift, as China’s relentless expansion coincided with severe disruptions at some of the world’s largest mines, making raw material scarce.

“The backdrop for copper’s 2026 treatment/refining charge negotiations, now underway, features a brutal game of industrial survival,” Panmure Liberum analysts led by Tom Price said in a note.

Japan’s JX Advanced Metals Co. this year announced an output cut running into the tens of thousands of tons, while Glencore Plc received a government bailout to keep its Mount Isa smelter and refinery in Australia running for another three years.

Chinese smelters do also suffer from low TC/RCs — but they benefit from the surging price of refined copper, used in construction and electrical wiring, and sulfuric acid, a byproduct. Copper was steady at $10,777 a ton on the London Metal Exchange as of 12:06 p.m. in Shanghai on Monday. Prices have retreated from a record high above $11,200 in late October.

China produced 9.7% more refined copper in the year through October. China is effectively “crowding out players abroad by securing the lion’s share of global concentrate supply and crushing the trade’s fee structure,” said the Panmure Liberum analysts.

With spot treatment charges having fallen as low as minus $60 per ton this year, not only buyers are walking away from the benchmark. Freeport McMoRan Inc., a top miner, has also signaled its intention to find alternatives, citing concerns about the viability of smelter clients.

A growing disparity between term TC/RCs and spot business has not helped the benchmark, said Li Chengbin, an analyst with consultancy Mysteel Global. “What we worry about more is how much volume Chinese smelters could secure via the annual contracts,” he said.

As long as they can afford to pay, Chinese smelters will continue to secure raw materials. Any pullback in their activity next year is likely to be limited, given the expected ramp-up of new capacity and commitments to uphold economic growth targets, said Xu Wanqiu, an analyst with Cofco Futures Co.

Read More: China copper smelters face pressure on declining acid prices

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments