China’s property stimulus creates iron ore price conundrum

Can you end a years-long property crisis without triggering a surge in the commodity that stands to benefit most?

That’s the dilemma facing the Chinese government, which is taking the most decisive steps yet to ease the impact of a devastating real estate crunch. Yet it’s already grappling with the bullish consequences for the price of iron ore — a key source of commodity inflation for the world’s second-biggest economy.

As the steelmaking ingredient soared toward its highest level since June 2022, China’s top economic planning body sent staff to the exchange that hosts futures trading to pursue tighter supervision. The National Development and Reform Commission then cautioned against hype, manipulation and “illegal activities” in the market. The NDRC is also seeking to strengthen oversight of iron ore held at ports to prevent hoarding and speculation, according to a statement on Friday.

So the next moves in the market depend not just on whether Beijing’s stimulus measures leave iron ore supply stretched, but also on whether the government can rein in bulls as it reboots the real estate sector. Citigroup Inc. sees prices reaching $140 a ton soon, after they burst through $130 a ton on Nov. 15.

“When they’re doing something that fights the fundamentals, they can slow the basis of price appreciation and cause pullbacks,” said Marcus Garvey, head of commodities strategy at Macquarie Bank Ltd. “But they don’t deliver a sustained change in the trend.”

Traders in China also report a more bullish tilt in the market’s mood, although there’s widespread reticence about talking publicly given the government’s scrutiny of the market.

China has long viewed iron ore rallies with suspicion, and has turned more interventionist in recent years to contain commodities prices. Beijing also wants to diminish the market clout of global mining giants like BHP Group Ltd. and Rio Tinto Group, which it claims reap outsized profits from Chinese demand.

The latest warning shots have had some effect on prices, which have softened in recent sessions. But futures in Singapore still racked up a solid fifth weekly gain last week, and have risen about 40% from this year’s lows.

“Basically, sentiment for iron ore next year has turned,” said Tomas Gutierrez, analyst at Kallanish Commodities. “This isn’t fully supported by current fundamentals, as demand now is weak. But we expect 2024 demand to be up from this year, with construction steel demand stabilizing.”

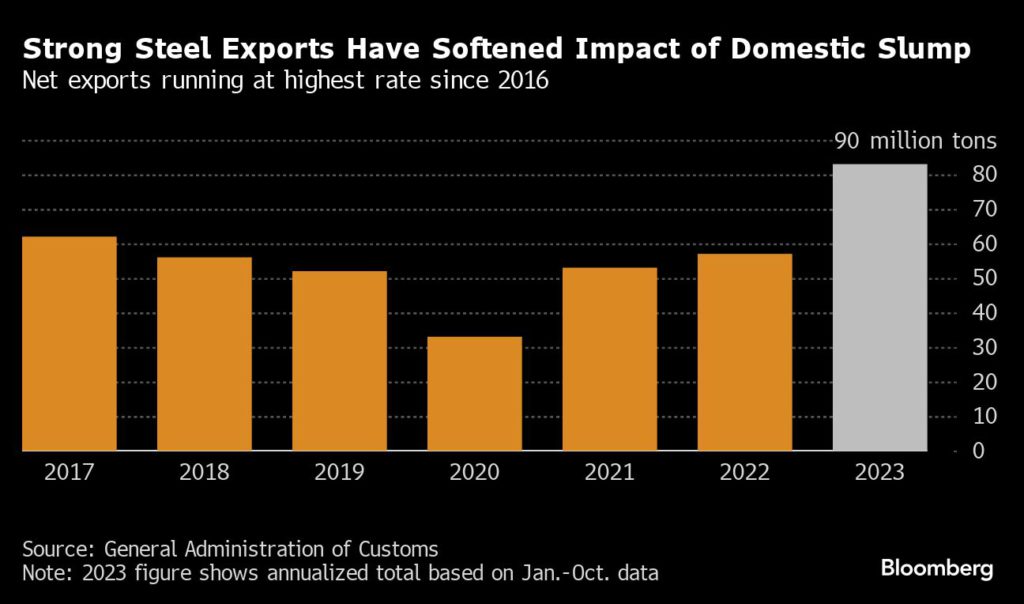

Even before Beijing amped up support for the property market, iron ore prices were showing resilience. Pockets of strength in the economy — from machinery to shipbuilding and infrastructure spending — have offset weakness from private construction. Rising steel exports have also helped, as has reduced availability of scrap, an alternative to iron ore.

But the most recent gains are, put simply, a bet that Beijing’s latest stimulus measures — particularly those focused on property — will put a floor under demand. Other commodities from copper to aluminum have also advanced in part on hopes of stronger Chinese consumption.

The plans for property mean “a major increase in our confidence around stable consumption from this portion of the market,” Citigroup analysts including Wenyu Yao wrote in a note. “Any dip on iron ore from here through to at least the Chinese New Year could represent a buying opportunity.”

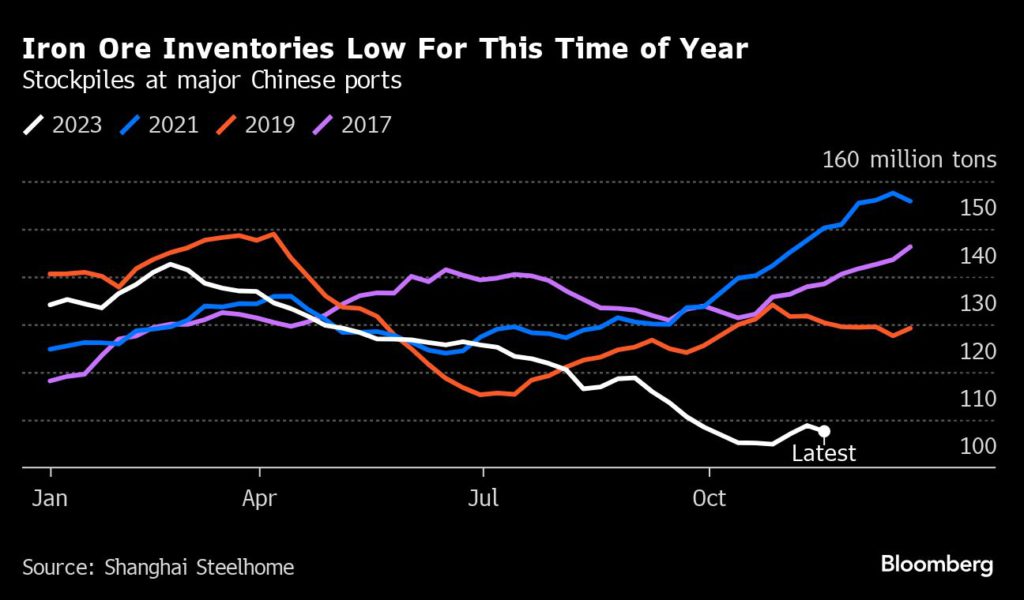

The turn in sentiment comes with the supply chain fairly tight. Iron ore stockpiles at major Chinese ports are at their lowest level for this time of year since 2015. Likewise, inventories of steel are also thinner than usual, with Citigroup noting an unusually rapid drawdown in recent weeks.

Chinese steel production is also proving robust, and the government looks increasingly unlikely to enforce its usual cap on output at the previous year’s level. Production in the first ten months was 1.4% higher than the same period last year and is comfortably on track for another billion-ton haul in 2023.

Steelmakers “largely have positive operating margins, so production will likely hold near current levels for the rest of this year,” said Kallanish’s Gutierrez. And they expect to keep run rates high through the first half of 2024, he said.

The onshore market views official intervention as “the main downside risk” for prices in the near term, Nicholas Snowdon, analyst at Goldman Sachs Group Inc., said in note after visiting China in early November. But participants also see “selloffs as a buying opportunity given the tight micro setup” and greater confidence for demand next year.

Iron ore’s rally comes at a sensitive time for China Mineral Resources Group, the state-owned trader created by Beijing to boost China’s heft in supply negotiations with the major overseas miners.

Guo Bin, CMRG’s president, said earlier in the month that prices were already unreasonable when they were in the low $120s. They’ve since risen nearly $10.

More News

Antofagasta to seek environmental approval for Encierro, Volcanes exploration in fourth quarter

The move would mark a step forward for two of Antofagasta's longer-term copper growth options.

July 03, 2026 | 04:16 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments