Critical minerals take central stage in US-China rivalry

Critical minerals have become the new frontline of the rivalry between the world’s two superpowers.

The United States looked to have taken a giant leap in this arms race late March with the signing of a cooperation agreement with Japan covering various minerals for electric car batteries.

Under this swiftly negotiated agreement, the US and its Asian ally will refrain from imposing export duties on lithium, cobalt, manganese, nickel and graphite.

The countries would also share information on potential labor violations in the supply chain for those critical minerals and “identify opportunities to build their respective capacities”, a statement said.

US making moves

The US-Japan pact comes as the Biden administration prepares to release guidance on how EV makers can qualify for the maximum tax credit under the Inflation Reduction Act, a landmark piece of climate legislation enacted by the US Congress last year to jumpstart clean energy production.

The IRA represents the single largest investment in climate and energy in American history. The Act, which is aimed to reduce emissions to half of 2005 levels by 2030, would provide US consumers tax credits of up to $7,500 per electric vehicle, provided the parts and materials are sourced from countries with which Washington has a free trade agreement.

Technically that would exclude Japan, but the new agreement essentially provides US allies the same FTA status for critical minerals trade.

“EVs that use materials that have been collected or processed in Japan will be eligible for incentives under the US Inflation Reduction Act,” Japanese Trade Minister Yasutoshi Nishimura confirmed in an official statement.

“This announcement is proof of President Biden’s commitment to building resilient and secure supply chains,” US Trade Representative Katherine Tai said in a separate statement. “Japan is one of our most valued trading partners.”

Speaking of valued trade partners, Washington is also close to striking a similar deal with the European Union after the two sides entered talks last month, according to reports. A draft of the agreement, as seen by Bloomberg, currently lists five minerals cobalt, graphite, lithium, manganese and nickel, mirroring that of the US-Japan deal.

However, a few details would still be ironed out for this critical minerals pact to become official. The EU has been seeking concessions from the law, which is offering as much as $369 billion in funding and tax credits over the next decade for clean energy programs in North America.

Other issues the EU needs to assess, both internally and with the US, include the scope of some of the trade, environmental and labor-related provisions, as well as their links with the IRA and implications on EU policy, Bloomberg sources said.

Another country eager to capitalize on the IRA benefits is Indonesia, which is reportedly looking at a limited free-trade agreement for some minerals shipped to the US to help its companies serving the EV battery supply chain. The Southeast Asian nation currently boasts the world’s largest nickel reserves.

China’s dominance

The motive behind the United States trade strategy is well-documented — to shed itself of dependence on China while loosening the grip its main rival has on the global supply chain of critical minerals.

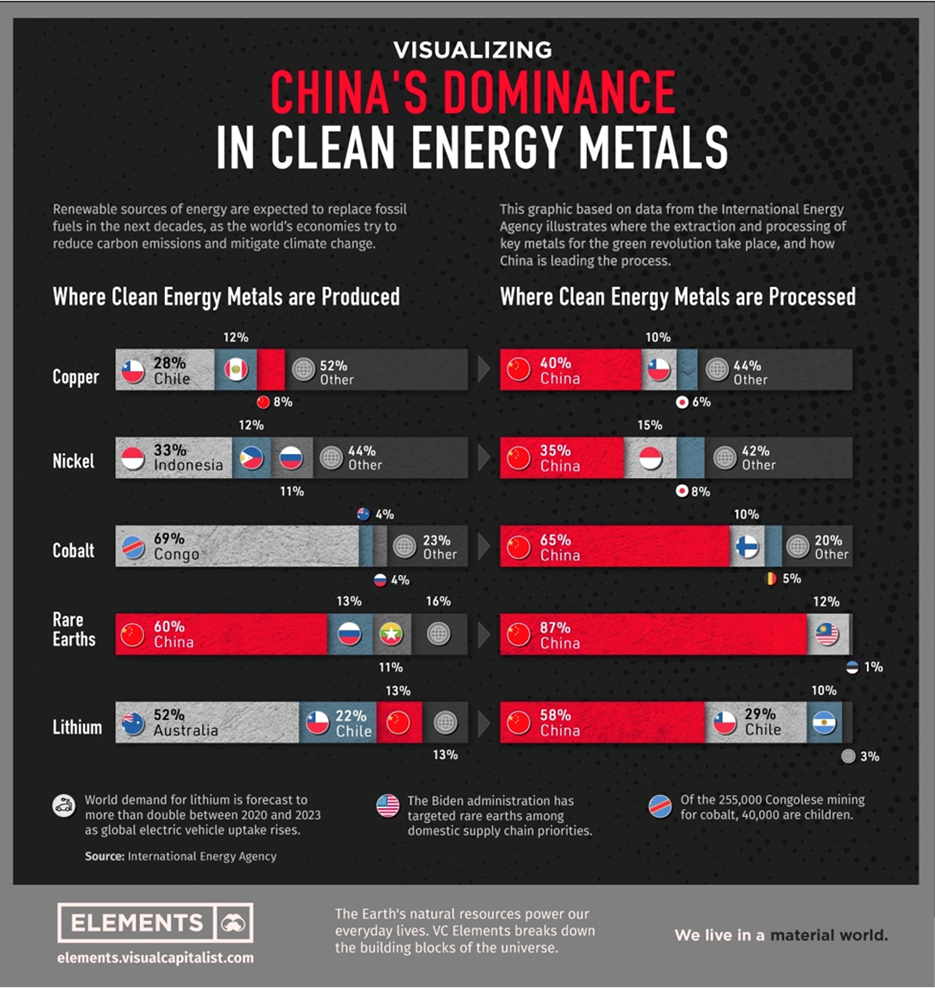

When it comes to raw materials for the electric vehicle industry, China is undisputedly the most dominant force on the planet.

For example, almost every metal used in EV batteries today likely comes from there, either mined or processed. Thanks to its technological prowess in refining, China has established itself as the across-the-board leader in the battery metals processing business (see below).

According to the International Energy Agency, the country accounted for roughly 60% of the world’s lithium chemical supply in 2022, as well as producing three-quarters of all lithium-ion batteries.

It also has a tight grip over the world’s supply of cobalt through its mining operations in the Democratic Republic of the Congo. Over the next two years, China’s share of cobalt production is expected to reach half of global output, up from 44% at present, according to UK-based cobalt trader Darton Commodities.

IEA estimates that China’s share of refining is around 50-70% for lithium and cobalt, 35% for nickel, and 95% for manganese, despite being directly involved in only a small fraction of the mine production.

The nation is also responsible for nearly 90% of rare earth elements, which are essential raw materials for permanent magnets used in wind turbines and EV motors, as well as 100% of graphite, the anode material in EV batteries.

The Road to “Independence”

A new report by Rice University’s Baker Institute for Public Policy reveals that China now controls roughly 60% of the world’s production of these minerals which are considered crucial to the global energy transition.

For the US, this poses a great security risk, as China could easily decide to weaponize its market dominance at any point, essentially locking America out of the critical minerals supply chain.

In a February 2022 fact sheet, the White House conceded that: “The US is increasingly dependent on foreign sources for many of the processed versions of these minerals. Globally, China controls most of the market for processing and refining cobalt, lithium, rare earths and other critical minerals.”

Speaking to CNBC earlier this year, Special Presidential Coordinator Amos Hochstein called this “a major concern for the US” and for the rest of the world. “As we are going into a cleaner, greener, an entirely new energy system, we have to make sure we have a diversified supply chain,” he said.

“We can’t have a supply chain that is concentrated in any country, doesn’t matter which country that is,” he continued. “We have to make sure from the mining and refining process to the building of the batteries and wind turbines that we have a diversified system that we can be well supplied for.”

Mining executives in the US critical minerals space are well aware of the market dissonance. “China is leading the way when it comes to lithium — and the rest of the world has not been quick enough to respond to its dominance,” American Lithium CEO Simon Clarke told CNBC back in November.

“For decades, they’ve been locking up some of the best assets across the world and quietly going about their business and developing knowledge on building lithium-ion technology, soup to nuts, and we’ve been very slow to react to that,” he stressed.

He added that the Inflation Reduction Act, and a number of other measures, meant people were “starting to wake up to it.”

Hochstein, however, rejected the idea that the US was being held hostage to China. “They’re trying to build an economy in the clean energy space and we all need to do the same,” he said. And that begins by giving incentives, through the IRA, to those that can bring minerals into the US for refining, processing and battery manufacturing.

After striking the trade deal with Japan, US officials told reporters that strengthening the US supply chain for critical minerals along with like-minded partners was “vital to the growth of the clean energy economy.”

The pact also contains a screening mechanism to ensure that critical minerals coming from “countries of concern” — referring to China and Russia — don’t benefit from the IRA incentives, Biden administration officials said.

Still, lots of work remains to be done for the US to fully reap the benefits of this new legislation and achieve net zero by its target date.

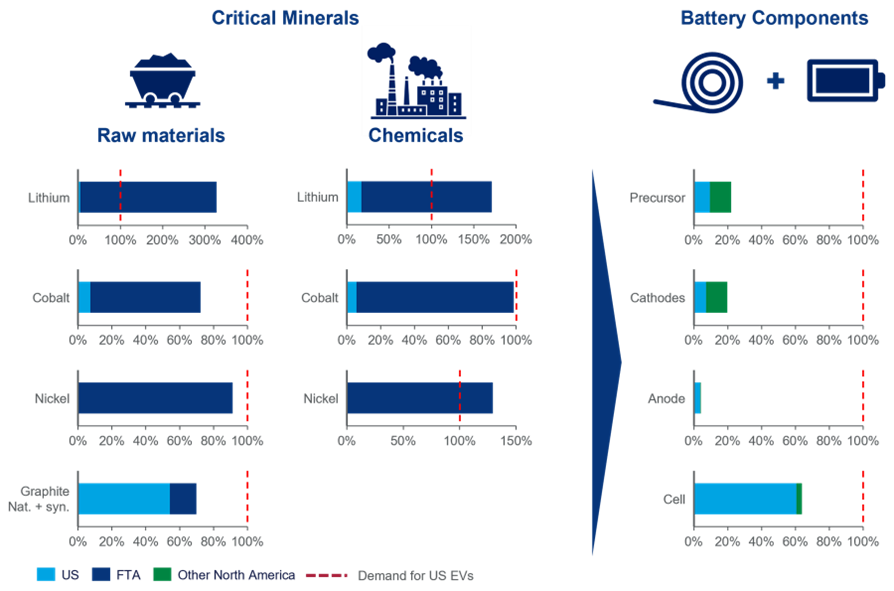

Wood Mackenzie senior analyst Max Reid suggests that US automakers could theoretically achieve the threshold for critical minerals through 2030 by focusing on the higher-value minerals in commercial batteries – lithium, nickel and graphite. However, battery components “are an altogether bigger challenge”, he said, since China dominates the supply chain for cathodes, anodes, current collectors, solvents, additives and electrolyte salts, with over 80% market share for certain parts.

China’s Play

Over on the other side, America’s rival is hardly sitting on its laurels in the critical minerals battleground. In recent years, China has made it increasingly difficult for the West to access its raw materials through stringent export restrictions.

These restrictions — most frequently taxes, but also quantitative limits — have increased more than five-fold in the last decade to a point where 10% of the global value of exports is subject to at least one measure, according to this week’s OECD report.

“The research so far suggests that export restrictions may be playing a non-trivial role in international markets for critical raw materials, affecting availability and prices of these materials,” the OECD wrote.

The OECD also warned in its report that these export restrictions could exacerbate the situation, “largely because they are permitted under World Trade Organization rules.” The overall global economic impact of these measures can thus be sizable, it said.

There are already growing fears that China’s export policy could extend to an outright ban on some minerals, in particular rare earths, for which it is by far the world’s largest producer.

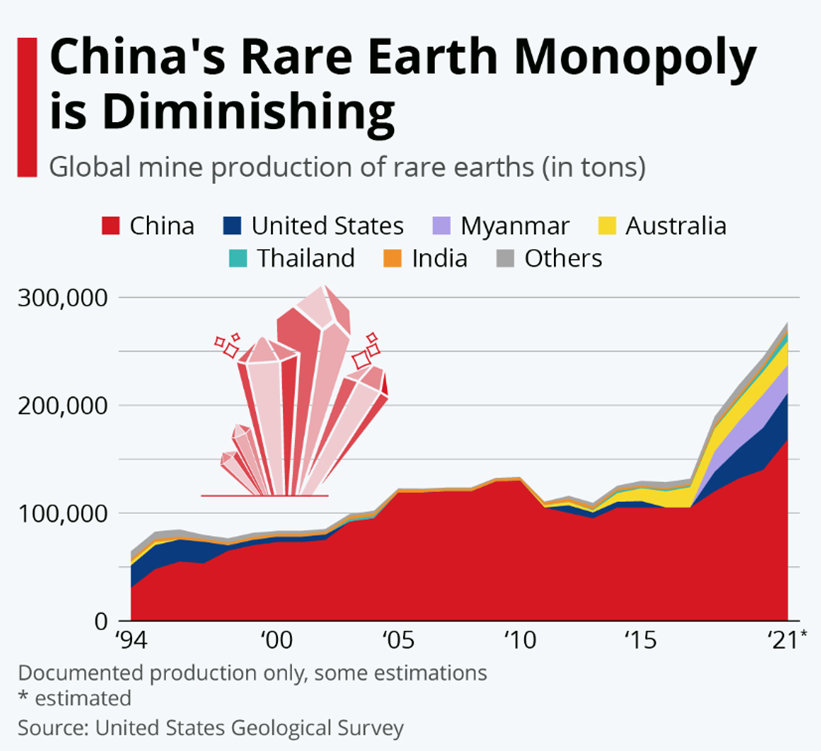

Of the estimated 120 million tons of rare earth deposits worldwide, the bulk of those at 44 million tons are found in China. The nation now accounts for 60% of rare earth mining, 85% of rare earth processing and 90% of high-strength rare earth permanent magnet manufacturing.

Rumblings of a China ban on rare earth exports first emerged in 2019, which caused angst amongst Western powers, pushing them to consider other sources of supply and establish new partnerships. And while it has been “all talk, no action” since, China’s threat remains a ticking time bomb.

Things could be heading in a precarious direction, though, following Washington’s recent decision to impose restrictions on exports of high-end semiconductors to Beijing. Reports are coming out that China is now considering the possibility of banning certain rare earth magnet technology exports.

The reality of China cutting off rare earths could prove catastrophic for the US, whose high-tech sectors imported 78% of their rare earth metals from China between 2017 and 2020, according to the US Geological Survey.

The Biden administration’s national security strategy, published in October 2022, has already identified rare earth supply chains as a major issue. A 2021 Defense Department review also concluded that overreliance on China “creates risk of disruption and of politicized trade practices” that would hit commercial sectors particularly hard.

China previously suspended exports of rare earths to Japan following tensions in 2010 surrounding the Senkaku Islands, which also alarmed those in Washington.

The US has since moved to bolster its domestic rare earth supply chain, with a degree of success. USGS data shows that China’s share of all rare earths produced globally dropped to roughly 70% last year from about 90% a decade earlier.

Nevertheless, China still has a firm hold on the processing of rare earths, and amid the heightened trade tensions, it would be fascinating to see what unfolds next.

Richard (Rick) Mills

aheadoftheherd.com

Subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments