What are the factors that influence the uranium price?

The uranium spot price has fallen below most of the world’s uranium mine operating cash costs, now standing at US$18.25 a pound. Which factors affect the price and which do not, and what rules are at play in the uranium market?

Today’s price in year 2000 dollars, assuming 28% inflation, would be US$10.60 a pound as opposed to US$8.30 back in 2000.

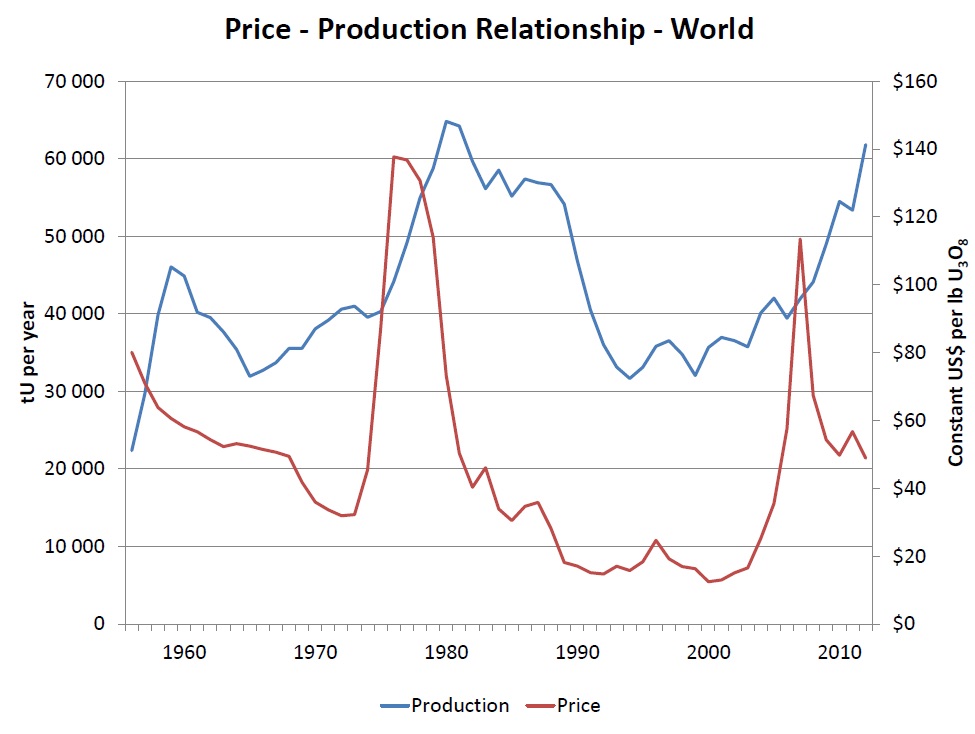

Uranium traded in the $8-12/lb range in January 1989 through December 1995, and May 1997 through July 2003 with the exception of 2001 when the price fell to the all-time low of $7 /lb. The top of the range would be roughly equivalent to US$15 in 2016 dollars. Privately, uranium producers describe the current state of the market as “horrible, naturally”. However, uranium traded within the same range for over 13 years until the price rose and then skyrocketed.

How well does the 2000 market compare to that of 2016?

As market insiders recollect, the players in these 16 years remained virtually the same. There was Cogema (later merged with Areva), Cameco, Rosatom, Rio Tinto, and WMC Resources (bought out by BHP in 2005). But there was no Kazakhstan with its 40% share in the world’s uranium supply produced at the world’s lowest-cost operations (according to Uranium One’s third quarter 2016 report, the company’s Kazakh operations’ ‘aggregate average realization cost is $7 per pound’). The world’s largest underground uranium mine at Cigar Lake was not yet commissioned. Today, according to Cameco’s CEO Tim Gitzel, operating cash costs at Cameco’s Canadian mines are ‘under $20 per pound’

It is difficult to say how past cash costs compare with current ones.U.S. nuclear consultant UxC didn’t publish its research at the time, and there is no such data in OECD’s 2001 Red Book. We know though that Cameco had to curtail its Rabbit Lake production from 4,491 tonnes in 1998 to 2,700 tonnes in 1999 and 2,790 tonnes in 2000 when the price did not exceed US$10 per lb.

“This sharp decline from 1998 production of 4,491 tU is the result of the production cutbacks implemented by Cameco in November 1998, which included the suspension of mining operations and a reduced milling rate at Rabbit Lake. In August 2000, Cameco announced that it would be extending the temporary shutdown of mining at Rabbit Lake through 2001. As a result, when the existing ore stockpile is depleted (expected in June 2001), the mill will be placed on standby for approximately one year, depending on market conditions,” said the 2001 Red Book.

The company did the same in April 2016 when the price had dropped below US$30.

It appears to be impossible for journalists, investment bankers and specialty consulting firms to forecast uranium price moves. The forecasts by UxC are regarded as the most reliable in the uranium industry and yet,“the spread in the forecast range varies up to 100%” notes “Uranium: Geology, Mining, and Economics” published by ARMZ in 2012 . Obviously, the practical value of such forecasts is rather limited.

Market forecasts made by International Nuclear Incorporated (INI), Royal Bank of Canada (RBC), and Global Mineral Research (GMR) cited in “Uranium: Geology, Mining, and Economics” turned out to be wrong, too.

Still, some factors influencing the uranium price seem to exist and we can attempt to determine the extent of this influence.

Economy and oil price

Some analysts posit that uranium prices correlate with the oil market. This correlation was first noted during the 1973-1975 oil crisis. When OPEC removed its oil embargo, commodities and food prices continued to rise and the uranium price peaked in 1975. In the following years, uranium showed little correlation with oil, its peaks and valleys preceding those of oil.

It seems that the uranium price responds to transformative events and trends in the world economy rather than to the movements in the oil market. For example, the 1978 oil crisis made little impact on the uranium market, and the pre-crisis peak of 2007 was not so much a history of uranium speculation as a reflection of irrational exuberance in the investment community, which affected the entire commodity market.

In the meantime, both the OECD and IMF have downgraded their forecasts. In September 2016 OECD downgraded (compared with its June figures) the world economy growth outlook for 2016 and 2017 by 0.1% to 2.9% and 3.2%, respectively. In October, IMF (compared with its April assessment) downgraded both outlooks by 0.1% to 3.1% and 3.4%, respectively.

For the uranium industry, it is important to recognize what will drive economic growth. Nuclear power should play the leading role in “green and big energy” (as opposed to “green and small” renewable energy) which is much needed for large industrial and urban development projects in environmentally-conscious countries. Possible decisions to construct new nuclear reactors in the UK and USA after Brexit and election of Donald Trump could provide the much-needed positive momentum in the uranium industry.

“Trump likes nuclear power, and he may push the zero emission attributes of nuclear plants, but, the insider said, there is little that can be done to reverse the economic challenges that nuclear power faces which, like coal-fired generation, are largely the result of low priced natural gas, which has driven down wholesale power prices,” said utilitydive.com (http://www.utilitydive.com/news/trump-energy-policy/430205/).

The world’s largest reactor fleet operates in the U.S, where, according to IAEA, 99 reactors are in operation and four are being constructed. Following the 2011 flood and issues with restart, the Fort Calhoun plant was shut down in June 2016. The Clinton and Quad Cities plants are also expected to be shut down within the next few years.

Demand and supply

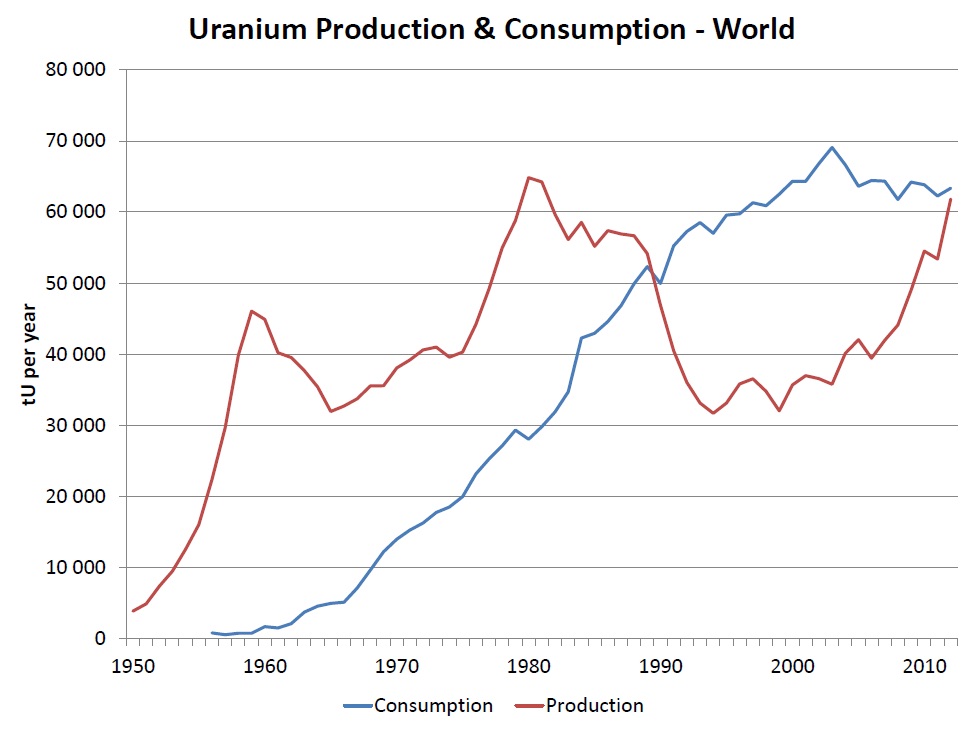

A comparison of uranium price and production shows a lag of several years in the declining market and quick recovery of production when the price rises.

The uranium price has not been very responsive to the changes on the supply side; it actually fell when Australia adopted the Three Mines Policy, and exhibited little reaction to news of mine accidents or shutdowns. The supply and demand chart since the early 1990s shows little correlation between the two data sets.

The correlation between the price of uranium and the cost of electricity exists but the impact of the nuclear fuel on the price paid by the final consumer is nearly negligible. According to the calculator by World International Service on Energy, the doubling of the uranium price to US$36.50 will result in a 17% rise in the cost of enriched uranium fuel. As reported by NEI, the share of nuclear fuel in the cost of electricity has been about 20% (±1%) over the last 13 years. So, a two-fold increase in the uranium price might lead to a mere 3.4% rise in the cost of power generation.

The history of the uranium market demonstrates that the only industry events the price is responsive to are nuclear accidents – Three Mile Island (1979), Chernobyl (1986), Fukushima (2011). Still, it is not easy to measure their true impact as it was overprinted by overall economic trends. For example, since March 2011 until March 2012, the price dropped by US$11.60 when the governments of Japan, Germany and Switzerland were making their decisions to shutdown nuclear reactors. And yet, between March and November 2012, the price dropped a further US$11.40 when the shutdown decisions were thought to have been accounted for by the market. During the same period, all other metals began to slide and notions of continuing economic crisis became commonplace.

If the global economy trends and accidents are so hard to predict, how can the uranium market be forecasted?

“Uranium OPEC” and state governments

Since uranium mining and nuclear power are of strategic importance, we might assume that governments could affect the market. The idea to institute an OPEC-like uranium organization to regulate uranium market and pricing to minimize the impact of spot prices has been floated in the industry, including by uranium-mining companies.

“That’s a good idea, of course,” said a source at Rosatom. But it was noted that such a structure on the corporate level could give rise to accusations in cartel agreements. Cameco’s director of communications Gord Struthers commented on the idea likewise: “It may be possible, but would not be practical given the wide range of players in the nuclear fuel market and the fact that many are state-owned entities that are not motivated by commercial interests alone. Additionally, there are certainly a number of legal and anti-trust considerations that would need to be taken into account on a matter such as this.”

Moreover, just as uranium and nuclear energy are part of global politics, a “Uranium OPEC” is impossible. “Nuclear OPEC has long been needed, and it should cover the entire nuclear power industry, not only uranium. But… it’s unrealistic. Nuclear is high-level politics, and nobody is going to allow a formal organization of this nature,” said atominfo.ru’s editor Alexander Uvarov.

To market participants who have been active in the industry for over 20 years, governmental oversight of corporate decisions does not look so much different as it was back in 2000. Today governments, agencies, and state-owned companies in China, Russia, Kazakhstan, and India agree on sales, deliveries, enrichment facilities, reactor and mine development, but do not take actions that could render direct impact on the spot market.

Big spot

It is thought that 10% to 30% of the uranium supply goes through the spot market. But as Cameco’s CEO Tim Gitzel commented in May 2016, the same physical uranium could be traded in many transactions, thus the real market size is impossible to estimate. “The number of U transactions is so small that we don’t have the benefit of a price based on thousands of transactions as with other exchange-traded commodities,” said Struthers, of Cameco.

Paradoxically, a relatively small segment of the market, which is volatile precisely because of its small size, determines the pricing in the entire uranium market.

The significance of the uranium spot market has been rising. Cameco notes in its Q3 2016 report that it received “gain from termination of long-term contracts.” This could mean that the buyer was actually saving by entering into new agreements and paying Cameco the termination penalties.

Buyers currently opt for executing one- or two-year delivery contracts whereas one-year delivery is recorded as a spot contract, according to Trade Tech.

The significance of the spot market even for major players could be indirectly proved by Kazatomprom’s recent announcement on establishing its own uranium trading company.

Good news for uranium miners could come from the spot market all the same. Uranium Participation Corporation (TSX:U) recently announced: “ As of November 2, 2016, UPC has entered into agreements to purchase 560,000 pounds U3O8 at an average price of US$20.57 per pound, with deliveries expected during November 2016” (http://uraniumparticipation.mwnewsroom.com/press-releases/uranium-participation-corporation-reports-uranium-purchases-and-net-asset-value–tsx-u-201611021074801001). The purchase was relatively small but it was upmarket and, besides, Uranium Participation already has a sizeable stockpile of yellowcake – some 4,300 tonnes (or almost 9.5 Mlb). It is interesting how the company funded the transaction – it raised over C$20 million by issuing 5.2 million shares to a syndicate of investors led by Cormark Securities, including Dundee Securities, Scotia Capital, and TD Secutiries. The proceeds are to be used to fund purchases of U3O8 and/or UF6. Does this mean that investors have begun to buy uranium even if indirectly? If so, this could be good news for the miners.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments