Frank Giustra builds another gold producer

Pan Mine, Nevada

1. Introduction

In December 2016, I introduced Fiore Exploration Ltd. (F:TSX.V; FIORF:OTCQB), a new company backed by Frank Giustra, and it has been a relatively quiet six months. Fiore completed some drilling on the Pampas El Peñon project in Chile and an IP survey on the newly acquired Cerro Tostado.

But behind the scenes, things were in motion. Earlier this year, Fiore began exploring the idea of merging with GRP Minerals, a private company ramping up the Pan heap leach operation in Nevada. GRP bought Pan and other Midway Gold assets for US$5.5 million and spent another US$18 million on upgrading and restarting the operation. Midway had spent more than US$100 million constructing the Pan mine but in the end failed to execute. The demise of Midway Gold is a whole other story, one I will touch on later.

The new entity will be named Fiore Gold, and Fiore Exploration CEO Tim Warman will stay on as CEO. I spoke extensively with Warman while preparing this article.

The agreement to combine with GRP Minerals has transformed Fiore from a quiet explorer into a developing producer with exploration assets. Now, however, those earlier-stage projects in Chile will be underpinned by development and production from the new Nevada assets. Strong and experienced heap leach management has been brought on by advisor Paul Matysek to get a firm grip on production at Pan and future development, and further acquisitions of producing assets are possible.

All pictures are company material, unless stated otherwise.

2. The Deal

Trading in Fiore Exploration shares was halted on June 12, 2017, and the business combination of Fiore Exploration and GRP Minerals was announced on June 15, 2017. The news release mentions that it is anticipated Fiore will acquire GRP Minerals, thus gaining ownership of the former Midway Gold assets. However, depending on advice from Fiore and GRP’s respective legal and tax advisors, the final deal structure may actually involve GRP acquiring Fiore.

In either case, it is expected that Fiore shareholders will receive 0.265 of a share in the combined company for each Fiore share held. GRP shareholders will receive 1 share of the combined company for each GRP share held.

Based on pro forma calculations provided to me by Fiore CEO Warman, the resulting estimated market cap of the combined company would come in at C$112.4M, with a share price estimated at C$1.15. Is this an attractive value proposition for existing and potential new shareholders? This will be discussed later on in this article.

Since the deal involved a significant change to the Fiore story, I wanted to take a closer look. I was aware the company was looking for more advanced assets, for example one with a NI 43-101 compliant resource that could then be explored and developed further into economic studies and even permitting.

Adding a producing asset, however, changes the profile and the thesis. Investors go from the high risk/high reward proposition of an exploreco to the lower risk profile of a company with both development and exploration assets. When I asked Warman about this, he explained that the company really needed a solid asset to underpin its market capitalization, which was predominantly backed by intangibles (and some cash). After doing a lot of due diligence, Fiore and Giustra decided to move on this deal.

3. The new story, and some context

Fiore Exploration is turning into a producer called Fiore Gold, so what will happen to Fiore’s exploration assets? According to Warman, the new strategy includes a focus on both, with the Pan cash flow basically paying for exploration and development ventures. Former Midway Gold CEO Ken Brunk will be COO of the new venture.

The company still has drill programs at Pampas El Peñon, where initial drill results were disappointing, and Cerro Tostado. But the exploration focus becomes Cerro Tostado, with minimal spending at Pampas El Peñon. I asked about a couple of pending drill results at the latter project, and they are still to come but Warman’s expectations seemed low. He thinks drilling success at Cerro Tostado could make things very interesting, since Yamana still needs additional mill feed as its nearby El Peñon plant is running below capacity—the original thesis of Fiore Exploration. Yamana describes El Peñon as its “flagship precious metals mine.”

It dawned on me that the acquisition of this substantial producing asset—after kicking off with early-stage exploration—bore some resemblance to the playbook of Lithium X, another Giustra-backed company. Lithium X also listed and raised its first capital based on Giustra’s reputation, management team and an early-stage, “stepping stone” exploration asset: Clayton Valley. Later, Lithium X managed to use its increased market value, amplified by rising lithium hype, to buy into Sal de los Angeles (SDLA), a much more valuable and advanced asset. As an aside: Lithium X recently sold the Clayton Valley asset to Pure Energy, and on June 28 achieved full ownership of Sal de los Angeles by buying the remaining interest from Aberdeen Capital.

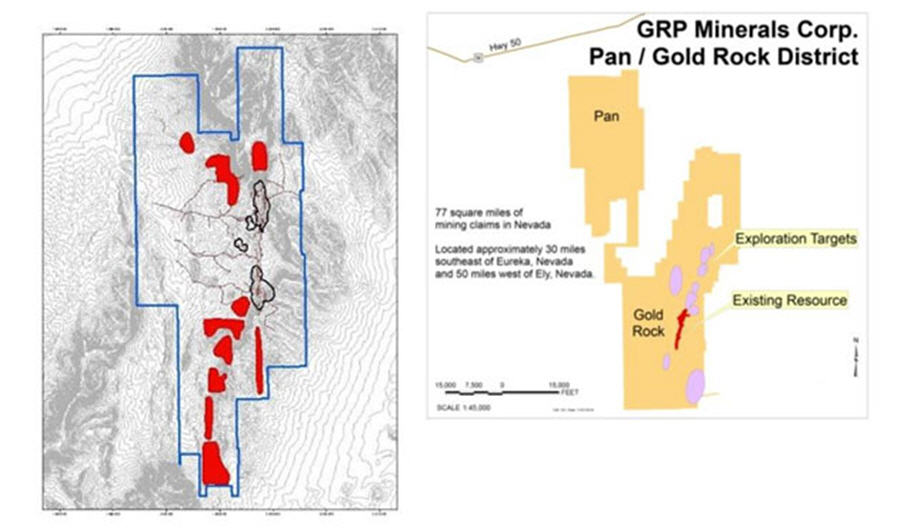

The GRP assets in Nevada, Pan and Gold Rock, need a lot of step-out and infill drilling, so Fiore Gold will have a complete strategy of grassroots exploration, brownfield exploration and development, and production. The Pan Mine is already ramping up production to a targeted level of 50,000 oz per year in 2019, and Warman expects its NI 43-101 compliant resource (434,000 oz @ 0.44 g/t Au M&I, and 72,000 oz @ 0.44 g/t Au Inf) to grow through infill drilling. A Feasibility Study is complete and should be released soon.

The Gold Rock deposit is less developed and has a historic resource (343,000 oz @ 0.58 g/t Au M&I and 409,000 oz @ 0.41 g/t Au Inf, per the 2012 Gustavson report). But after studying the asset with his team, Warman is convinced that Gold Rock has upside on grade, resource size and economics compared to Pan.

Pan and Gold Rock are just 10 km apart, and Warman and I discussed the idea of transporting ore by trucking or conveyor belt. But the CEO said it wasn’t economic because the grade is too low. That means Fiore is targeting a second stand-alone mine in the future for Gold Rock. However, there are possible synergies including refining and administration. Warman thinks Gold Rock could have potential for at least a 50,000-oz and likely a 75,000-oz per year heap leach operation. Metallurgical work suggests more or less similar mineralization as Pan, so it looks like a relatively cheap ROM heap leach concept is possible for this project, too. That could indicate a rough estimate of a post-tax NPV5 (5% discount) of US$100-120 million, based on an estimated US$80-90M capex.

GRP’s third asset, Golden Eagle in Washington State, is a bit more complicated. It has a decent open-pittable resource of 1.74 Moz @ 1.7g/t Au Indicated, and 0.19 Moz @ 1.2g/t Au Inferred. But according to Warman, the claim boundaries are tight and an open-pit operation is probably not possible on the GRP claims alone. Part of the surrounding claims are owned by Hecla (Golden Eagle’s former owner) and Kinross’s nearby Buckhorn mill is running out of ore, with closure pending. That makes some kind of three-way deal for Golden Eagle a possibility. The NI 43-101 report on this deposit indicates that the ore is refractory, which means much higher costs to recover the gold. Most of the time, recovery by acid leaching is not possible and requires a very costly and energy-consuming autoclave to roast the large percentage of pyrite. Capex and opex have been known to double in such instances. However, a closer read of the Golden Eagle report reveals that all is not lost.

Golden Eagle project

Next up are a few extensive quotes from the NI 43-101 report to provide some additional color/explanation, which could be useful in my view:

Pg. 10:

“Hecla and SFPG conducted various metallurgical tests in the 1980s and 1990s which demonstrated that direct cyanidation is not a feasible process option for most of the samples, that the gold is finely and homogeneously disseminated in the samples, and that the mineralized material is generally refractory for gold extraction. Refractory gold refers to mineralized material that is naturally resistant to gold recovery by direct standard cyanidation and activated carbon absorption processes.Calculations based on estimated abundances of different types of pyrite in a metallurgical sample suggests that about 66% of the gold could be present in solid solution in arsenic-bearing, fine to medium grained pyrite. Gold extraction by direct cyanidation was limited to 11.8% to 27.8%, except in one composite which exhibited gold extraction up to 59.2% by direct cyanidation, for a composite weighted average of 22.4%. Whole ore cyanide extraction therefore does not appear to be a viable extraction process for most of the deposit.

Due to the refractory properties of most of Golden Eagle’s mineralized material, sulfide oxidation will improve gold extraction and recovery. Standard pre-treatment options for sulfide refractory ores include chemical pre-treatment, roasting, bio-oxidation, pressure oxidation (POX), ultra-fine grinding and concentration by gravity or flotation. The gold in the Golden Eagle mineralized material mostly occurs as solid solution within the pyrite matrix, which is generally impermeable to direct cyanidation, so the gold must be liberated by oxidation of the sulfides to yield permeable sulfates and oxides that are more readily leached. Thus, the degree of sulfide oxidation will generally correlate with the success of extracting the gold via cyanidation. Flotation tests were able to achieve gold recoveries at 82.4% to 95% into the flotation concentrate, which comprised 12.46% to 26.84% of the total weight.

Flotation concentrate assays ranged from 0.143 opt to 0.905 opt. This large concentrate mass with relatively low gold grade may be challenging to transport, capitalize and process economically. Additional metallurgical testing on the flotation concentrate for bio-oxidation and pressure oxidation followed by cyanidation showed overall gold extractions using bio-oxidation at 71.7% to 82.6% and POX gold extraction at 88.5% to 93.5%. Mather (1990) noted that bio-oxidation and pressure oxidation of the whole samples supplied by Hecla both enabled subsequent optimal extraction of 90% or more of the gold. The tests achieved a high degree of sulfur oxidation (>99%) and enabled gold extractions of 94% to 98%. At sulfur POX oxidation of 92%, gold extraction dropped to 89%.”

The report clearly indicates various methods not involving roasting, but still with probably economic extraction percentages. In another chapter, the report touches on why Hecla shelved the project:

p.32:

“This study concluded that the ore had very homogenous grades but was refractory and could not be run in the existing oxide mill. They explored several options for gold recovery with recovery results ranging from 50% to 80%. Costs to treat the refractory ore were deemed uneconomic at a $400 gold price. Hecla shelved the project but recommended exploration for deep vein potential.”

When doing analysis on Midway Gold in 2014, I was told by management that Golden Eagle was shelved by them as well because of issues with permitting. Warman had this to say when I asked him about permitting: “We haven’t looked into the permitting issue in detail at this point, but the project is located in a historic mining district with current mining operations, and with a local economy that’s dependent on the resource industry.”

The Golden Eagle report further discussed the merits of an autoclave, confirming it had the best recoveries:

p.81:

“Based upon Hecla’s and SFPG metallurgical test work, autoclave pressure oxidation of the whole mineralized sample appears to have the best overall gold recovery, with extractions in the 88.5% to 98% range. Silver extraction appeared to not be tracked well. This whole ore oxidation process followed by neutralization then cyanidation-CIL of the residue on site would be capital expensive. If a used autoclave can be found then this flowsheet development will need to be examined closely. The sulfide sulfur is low in the whole mineralized sample and will need additional sulfide concentrates, or extra heat must be added. A detailed capital and operation cost study should be undertaken and compared with the previous flowsheets.”

However, bio-oxidation is recognized as the best option, generally speaking, in this case:

p.101:

“Three potential process flowsheets have been identified, including whole ore flotation with cyanidation carbon-in-leach of the flotation tails, whole ore bio-oxidation in heaps or ground slurry with cyanidation carbon-in-leach of the bio-oxidation tails, or whole ore pressure oxidation followed by cyanidation carbon-in-leach of the pressure oxidation tails. Bio-oxidation appears to hold the most promise and should probably be the base assumption until further scoping level analyses can be performed to provide refinement of this assumption.”

The recommendations established the need for the asset owner to buy more land around the Golden Eagle property. That likely requires striking a deal with Hecla:

p.103:

“Undertake slope stability studies to establish the maximum slope angles for an ‘ultimate’ pit shell design and to determine the extent of neighboring additional land required to realize the full potential of the mineral resource.• Consider the purchase of additional land and mineral rights from Hecla Mining Co. to obtain neighboring land and undertake appropriate environmental and engineering studies on the extra land.”

Fiore’s focus is on ramping up Pan at the moment, so Golden Eagle is not a top priority for the next six months. The Pan Mine is not your average small-time, bread and butter gold mine, so I questioned Warman extensively about it.

I will not discuss the entire Midway/Pan story here, since the article is about Fiore Gold. However, the demise of Midway Gold is one of the most well-known debacles in recent mining history, so it’s appropriate to take a look back.

Pan Mine: rehabilitating leach pads

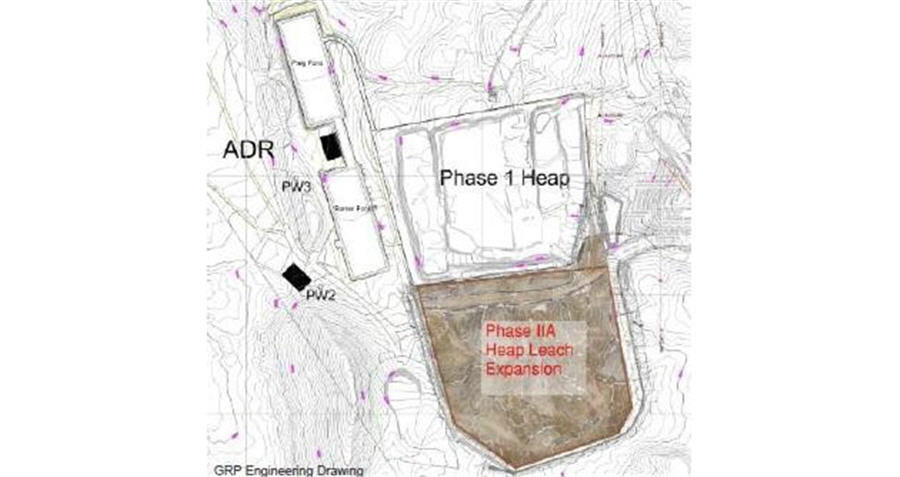

The Gustavson resource estimate for Pan, describing much more gold and less clay than present in reality, and resulting in the dreaded grade variance, may have been the start of the troubles. But there was more to it. Capex in the Pan Feasibility Study was estimated way too low as it turned out, and after raising the projected capex in debt and equity, further engineering pointed quickly to cost overruns. In response, Midway management decided to defer crushers and switch from owning a mining fleet to contract mining.

Despite these cost saving measures, more cash was needed soon. Major shareholder and financier Hale Capital was not impressed and resisted more financings, so management’s back was against the wall. At one point, they decided to save time and start production faster by starting construction of the leach pads at the lower end. That way the leach pads didn’t have to be completed before ore stacking and leaching could begin. It may have been a nice idea in an area where it never rains.

However, in Nevada it does rain from time to time. And sure enough, right after Midway completed the first, lower part of the leach pads, a few days of torrential rains severely damaged pads and already completed groundwork. That set construction back at least six weeks and caused millions of dollars in damage. A resulting cash shortfall emerged and while construction proceeded to the point of first production, it stalled the project.

Production was halted and a new NI 43-101 report had to be completed, to address the grade variance. The new Pan resource estimate included only about 40% of ounces as resources and no reserves. Midway went down in flames, despite an additional last-minute US$10-million line of credit provided by Hale Capital. All assets were sold out of bankruptcy to GRP Minerals, a new player established to buy the former Midway assets. GRP is founded and headed by Ken Brunk, the former Midway CEO who retired in 2014.

I spoke to Warman about some of Midway’s issues, and he assured me Fiore Gold will be very transparent going forward. He noted that Giustra and Matysek’s team of engineers and advisors had done extensive due diligence for months, and will control and monitor things closely from now on. The big game changer at Pan was the opportunity to mix the clayish ore with more rocky ore, so crushers and agglomerators weren’t needed anymore. The Fiore team sifted through history and current operations, and Pan appears to be a well-run ramping up mine at the moment. Having veterans like Matysek and heap leach specialists like David Keough (ex COO of Goldrock Mines and its Lindero heap leach deposit, bought by Fortuna Silver) and Tim Scott (ex Gold Fields general manager heap leach mine) monitoring proceedings is reassuring.

As for the timing, Fiore has a good handle on the value of the GRP assets and wanted to proceed with the transaction as soon as possible, Warman told me. No negative surprises are expected from the pending FS, and the post-tax NPV5 of Pan probably comes in at C$60-65 million. The amount of sunk costs is huge, I estimate the total costs for exploration and advancement to construction at US$50-60 million, spent capex at US$110-120 million, so before GRP bought it the sunk costs could have been as high as US$160-180 million. After buying the Midway assets for just US$5.5 million, GRP invested another US$18 million on rehabilitating Pan and permitting Gold Rock.

Most of the money was needed to adequately mix and restack the ore on the leach pads, as the solution for the lower grade clayish ore previously mined from the South Pit was to mix it with rockier (and higher grade) ore as mentioned, coming from the new North Pit.

Pan is producing at a 10,000-tonne-per-day rate at the moment, and had 1,700 oz Au per month production in June, which is set to increase to 1,900 oz monthly from July onwards. The average grade is 0.44 g/t Au, which is exactly confirming the resource grade. Fiore is targeting 3,300 oz per month at the beginning of 2018 as the company expands the mining rate to 14,000 tpd, which would result in an annual production of 40,000 oz Au. With further improvements and a heap leach expansion, this figure is expected to grow to 50,000 oz Au for 2019.

Gold Rock will be fast-tracked and Fiore thinks the project is capable of adding another 50,000–75,000 oz Au of annual production by 2020. Permitting is underway, with a EIS Record of Decision expected in Q4 2017. The current historical resource will be updated at the end of Q2 2018, most likely by SRK. Both Pan and Gold Rock have considerable exploration upside, which could extend both mine life and annual production. Key to the strategy is acquiring another near-production deposit of 800,000 to 1 million ounces Au, capable of producing at least another 50,000 oz Au annually. That would bring total annual production to at least 150,000 oz Au in 2020-2021.

How to value Fiore Gold after the transaction closes? The sum of parts consists of:

- the current exploration assets, of which I estimate El Peñon at C$1M and Cerro Tostado at C$4M

- about C$25M in cash, zero debt

- Pan with a C$65M NPV

- the Gold Rock historical deposit and the exploration potential of both Pan and Gold Rock combined at C$20M

- Golden Eagle at C$5M, bringing the total NAV at C$120M. Compared to the calculated pro forma market cap of C$112M, it seems like Fiore Gold will be close to fairly valued when shares start trading again at the calculated share price of C$1.15.

The market cap target of Fiore Gold management is C$1 billion when it arrives at the targeted 150,000 oz a year—peers would include Guyana Goldfields, McEwen Mining and Klondex Mines. Each of these companies have completely unique stories, of course. But if Fiore Gold manages to achieve this production with low all-in sustaining costs, high margins and a healthy balance sheet, I don’t see why it’s not possible.

Fiore’s most important assets are located in the safe, mining-friendly jurisdiction of Nevada) and the involvement of big names (Giustra, Matysek) should help arrange easy access to capital (debt and equity). Usually, this combination of features generates a decent premium to average market ratios, and this is why I think, like management, that the C$1 billion target isn’t unrealistic at all. The only question will be the amount of dilution when funding the Gold Rock capex and the acquisition and development of the eventual new asset. In the very hypothetical and most conservative funding scenarios, the Gold Rock capex is $80-90M. Financed on a 1/3-2/3 -debt basis based on a share price of C$1, dilution would be about C$40M / C$1, or about 40M additional shares. I’m not ruling out funding a part through internal Pan cash flow, which could improve dilution figures considerably.

The same goes for the new asset. Let’s say a new asset would cost US$30 million (assuming all equity) and another US$80-90 million (assuming same equity/debt ratio) to develop it, this would add another estimated 80M shares. The resulting number of shares would increase with a hypothetical 120M, bringing the total shares O/S to about 220M, assuming internal cash flow would finance all working capital needs in the meantime. Let’s assume some more dilution for contingency just in case, Fiore could end up with 250M shares O/S. If Fiore would succeed in all this, and maintain a share price of at least C$1 by then, the market cap would be C$250M, which still means a potential four-bagger re-rating if everything goes to plan and gold remains at least in the $1200-1300/oz Au range for the next three to four years. Something tells me Giustra isn’t satisfied with just a 150,000 oz per year producer in three or four years. Besides this, the company is named after his mother, as you might recall, so I’m convinced Giustra is determined to make Fiore Gold a resounding success.

4. Conclusion

After a remarkable deal, involving remarkable assets, Fiore seems to have transformed from a quiet explorer into a busy, ramping up producer almost overnight after a reverse takeover of GRP Minerals. According to CEO Warman, Fiore will continue to do lots of exploration underpinned by development and production from former Midway assets Pan and Gold Rock.

The first goal is to get Pan to 40,000 oz annually at the end of 2018, and grow further by bringing Gold Rock and possibly another to be acquired asset into production by 2020-2021. That would bring targeted total annual production to 150,000 oz, which I believe is conservative. Yes, this will require dilution by funding capex and a new asset, but the upside over the coming three to four years could very well be an estimated quadruple, based on the characteristics and potential of projects and people.

Pan Mine; ore stacking on leach pads

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at http://www.criticalinvestor.eu/, in order to get an email notice of my new articles soon after they are published.

The Critical Investor Disclaimer:

The author is not a registered investment advisor. Fiore Exploration/Fiore Gold is a sponsoring company. All facts are to be checked by the reader. For more information go to www.fioreexploration.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long term commodity pricing/market sentiments, and often looking for long term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Streetwise Reports Disclosure:

1) The following companies mentioned in the article are sponsors of Streetwise Reports: Klondex Mines. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

2) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

3) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

4) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Charts and photos provided by author

Source: The Critical Investor for Streetwise Reports (7/13/17)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments