Funds still wary of shorting super tight copper market

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

A slowdown in China’s manufacturing sector is casting an ever larger shadow over the copper market.

The country’s official purchasing managers index (PMI) was 49.2 in October, down from 49.6 in September and the second straight month of contraction. Environmental curbs, energy rationing and higher raw material prices are combining as a powerful brake on activity.

“Metals can’t ignore China slowdown for much longer” was the title of a Nov. 1 research note from Capital Economics and one that captures a growing sense of unease about copper’s price outlook as demand in the world’s biggest user cools.

Funds, however, show no inclination of shorting copper just yet. And who can blame them given the continued low exchange stocks and extreme spread tightness in the London market?

Funds play it from the long side

Last month’s turbulence, which saw the London Metal Exchange (LME) three-month copper price spike to $10,452.50 a tonne, sucked fund money in on the long side.

[Click here for an interactive chart of copper prices]

Money managers lifted outright long positioning on the CME copper market to a five-month high of 82,538 contracts in tandem with the price move.

That collective bull bet had retreated to 77,317 contracts in the most recent Commitments of Traders Report (COTR) but was still surprisingly elevated given the price had already collapsed below the $10,000 level.

The COTR captures positioning at the close of business last Tuesday (Oct. 26) and it’s quite possible there was a further reduction in bull positions over the back end of the week.

LME broker Marex, for example, notes heavy fund selling into the close of the month and estimates the net fund long in the London market slumped from 8% of open interest on Oct 20 to just 1% as of Friday.

What really stands out, however, is the absence of any fresh short positioning despite copper dropping back to $9,500 per tonne and the darkening macroeconomic outlook.

Outright short positions on the CME contract currently total just 29,721 contracts, slightly lower than at the start of October.

Fund managers seem happy to adjust their long positioning as the price gyrates but remain loath to go short.

Still turbulent

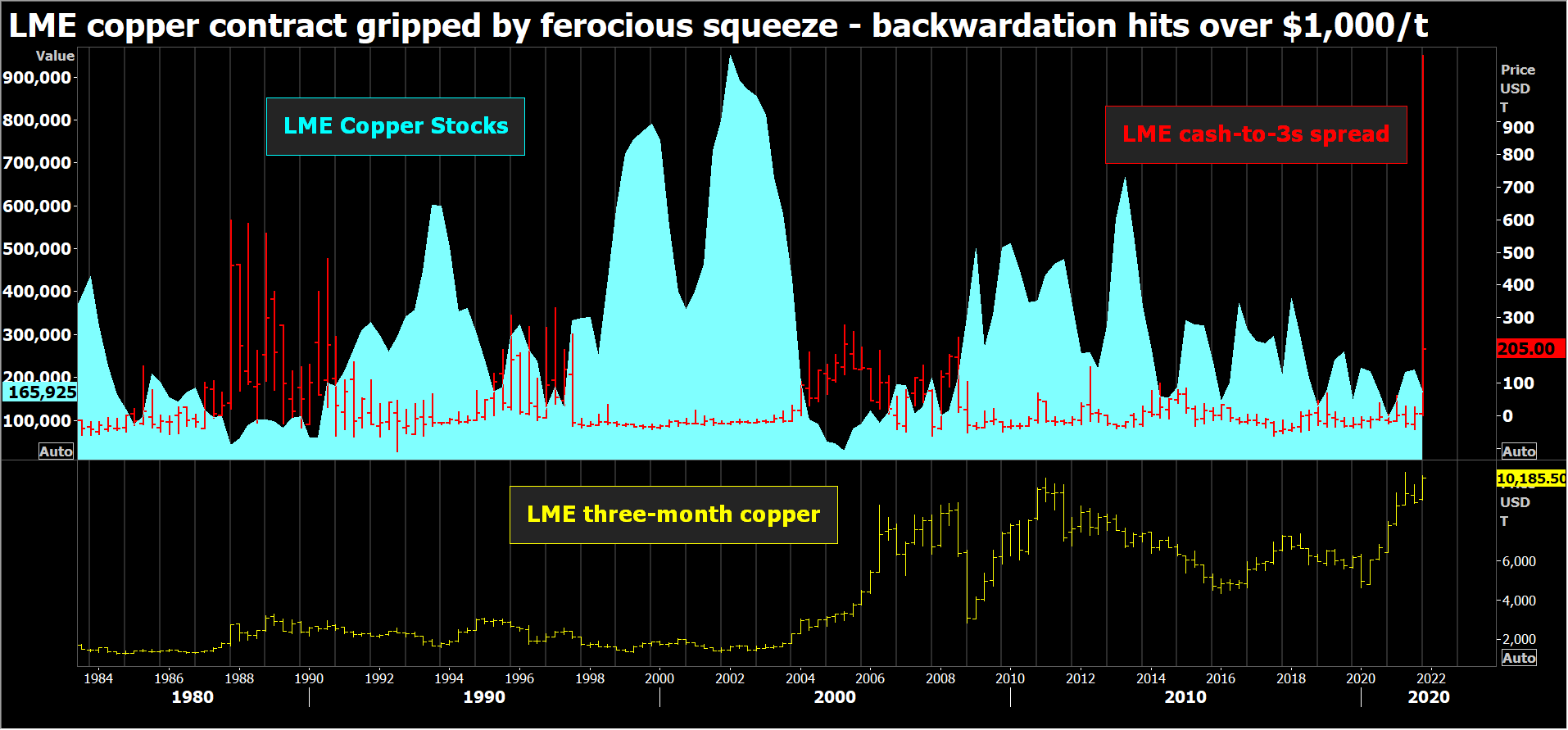

What’s deterring them is the wild backwardation still raging in the London market.

The LME’s Oct. 19 intervention here in the copper market has restored a semblance of order to the shortest-dated time-spreads, as intended.

But the benchmark cash-to-three-months spread remains extremely backwardated. The cash premium at Monday’s close was $438 per tonne, which until last month’s chaos would have been the widest this century.

The underlying problem remains chronically low exchange stocks.

The eye-watering premium for physical delivery has enticed metal into LME warehouses but total arrivals of 21,075 tonnes since the middle of October have been underwhelming.

The South Korean port of Busan has received 7,700 tonnes with the balance spread across seven locations in Europe, Asia and the United States. Absent is the sort of heavy volumes that might have been expected with such a historically high premium for exchange delivery.

What has arrived in the last couple of weeks has not offset the daily departures, with the headline LME stocks figure sliding to 123,925 tonnes, the lowest since the first day of June.

More significantly for short-position holders, the amount of available tonnage in the LME warehouse system has rebuilt only marginally from October’s multi-decade low of 14,150 tonnes to 31,675 tonnes.

That’s a long way from any sort of comfort zone, which is why the front part of the forward curve may be orderly in the LME’s regulatory sense of the word but is still highly turbulent.

Too turbulent, it appears, for macroeconomic bears to dare express their views.

Micro trumps macro… for now

Copper has been caught between a deteriorating macroeconomic outlook and the strength of its own micro dynamics for several months.

The nature of the raid on LME stocks – massive cancellations of available tonnage over the first half of October – remains controversial.

But it’s worth noting that global exchange stocks, comprising those in LME, CME and Shanghai Futures Exchange warehouses, have fallen for the last two months.

They stood at a cumulative 232,550 tonnes at the end of October, down 30,000 tonnes since the start of 2021 and down almost 150,000 tonnes from October 2020.

Shanghai stocks currently total less than 50,000 tonnes, despite evident weakness in key end-use sectors such as construction.

The Yangshan copper premium, a closely-watched indicator of China’s import demand, has fallen sharply from its October peak of $140 per tonne to $89 but that’s still much higher than the June trough of $21, suggesting continued supply-chain tightness within the Chinese market.

Combined with the conspicuous absence of any large arrivals in the LME system despite the roaring backwardation, the market’s fundamental optics still look bullish.

With no sign of any major inventory rebuild and no sign of any dissipation of LME tightness, it looks like copper’s micro picture is still strong enough to keep the macro bears at bay.

(Editing by David Clarke)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Amarjeet Singh

Copper is between the deep end the devil.