Global metals exploration anticipated to rise 20% in 2018

S&P Global Market Intelligence predicts that exploration efforts will continue to expand over the course of this year

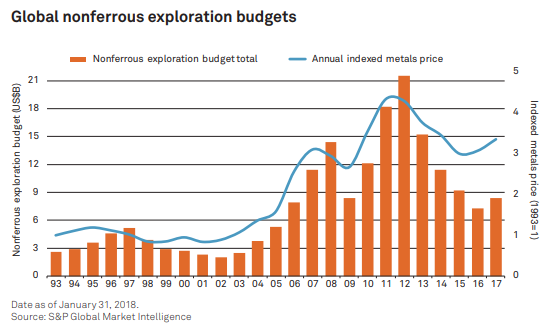

Global spending on the search for nonferrous metals rose to an estimated US$8.4 billion in 2017, compared with US$7.3 billion in 2016, representing the first annual increase in exploration spending after four consecutive years of declining investment in this area, according to the World Exploration Trends (WET) report from S&P Global Market Intelligence, released in conjunction with this year’s Prospectors & Developers Association of Canada (PDAC) International Convention.

Mark Ferguson, Associate Research Director at S&P Global Market Intelligence, says: “Improved equity market support for explorers allowed many companies to launch or resume drill programs on their most promising projects. Although the main focus was on gold, exploration targeting base metals assets also rebounded in the second half of the year, and the battery metals attracted particular attention. In the last quarter of 2017, there was a sharp increase in reported drill results, and financings closed the year on a high note. As a result, our year-end measure of exploration sector activity reached levels not seen since early 2013.”

“Despite significant market volatility, the generally positive trend in metals prices has continued in early 2018; we therefore expect the global exploration budget for 2018 to increase by a further 15% to 20% year-over-year.”

Key takeaways from the report:

- Signs of life: after four years of depressed exploration spending, the mining industry upped aggregate nonferrous exploration budget to US$7.95 billion by surveyed companies — a 14% increase over 2016.

- Reflecting funding challenges faced by some junior companies early in the year, the number of explorers with spending plans declined slightly, by 3% year-over-year to 1,535 companies.

Producers restrict exploration: major miners (revenues >US$1 billion) continue to allocate only a small proportion of their revenues to exploration efforts. Riskier exploration remains relatively unattractive.

Producers restrict exploration: major miners (revenues >US$1 billion) continue to allocate only a small proportion of their revenues to exploration efforts. Riskier exploration remains relatively unattractive.- Canada, Australia and U.S. continue to lead exploration spending: with allocations totalling US$5.55 billion. The top 10 countries accounted for 70% of the US$7.95 billion global surveyed total.

- Gold led the way to a higher global budget in 2017.

- Battery metals exploration surges: lithium exploration allocations in 2017 more than doubled year-over-year, while cobalt-focused exploration also increased strongly.

- Exploration sector health improves: S&P Global Market Intelligence’s measure of exploration activity, the Pipeline Activity Index, jumped to 87 in Q4 from 77 in Q3, the highest since Q1 2013, when the recent downturn was just beginning.

- The S&P Global Market Intelligence Pipeline Activity Index incorporates data on the number of projects announcing significant drill results, exploration financings, initial resources and positive project milestones

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments