Gold’s perfect storm

US Treasuries are as much sought-out by investors in a crisis or pending crisis, but lately, Treasuries have become much less popular as a means of storing wealth.

The reason is simple: T-bills don’t offer a good return, and neither do other sovereign debt instruments. Although US Treasury yields have been climbing, owing partly to expectations of inflation, in recent weeks this trend has reversed, amid renewed concerns about the pandemic.

On Tuesday, the World Health Organization warned that global infections were reaching their highest levels, prompting many fund managers to rotate money into safe-haven bonds. The yield on the 10-year Treasury slid to 1.5% while the 30-year yield was reduced to 2.26%.

Looking at the 10-year chart, we see the yield starting to climb in January, reaching as high as 1.74% on March 19 before falling from 1.69% at the start of April to the current 1.5 %.

Subtract 2.6% inflation and the real yield is negative 1.1%.

There’s an old saying on Wall Street: “Six percent interest will draw money from the moon.” And it’s true, but what is also true is, 1/ As long as real interest rates are below 2% gold is in a bull market and 2/ Real interest rates below 2% draw investors to gold.

Central banks know this, so do educated gold buyers.

With Treasury notes paying such low net yields, gold becomes an attractive investment. And while the precious metal offers no yield, its status as an inflation hedge and store of value not subject to fiat currency manipulation are good reasons for central banks to purchase gold. Due to an increase in inflation every decade except the 1930’s, the US dollar has lost 90% of its purchasing power since 1950.

Gold, on the other hand, has gone from $35 in 1970 to $1,750 in 2021, a 50X increase!

In October 2020 central banks sold gold for the first time in a decade. Bloomberg reports the sell-off was profit-taking among gold producing nations who wanted to exploit near-record prices (gold hit a record $2,030 an ounce last fall) to soften the blow from the coronavirus pandemic.

Six months later, the tables have turned.

China back into bullion

China reportedly has just given domestic and international banks permission to import large amounts of gold, which could help support gold prices after months of declines.

China and India are the world’s two largest gold consumers, accounting for some two fifths of annual demand.

Quoting anonymous sources, Reuters stated on April 16 that Beijing has given the okay to bring in 150 tonnes of the precious metal, worth $8.5 billion at current prices, expected to arrive in April and May.

That is a dramatic turnaround from the past few months. Chinese customs data shows since February 2020, the country has only imported roughly 10 tonnes a month.

Reuters explains the reason for China wanting more gold is its recovering economy hiking demand for gold jewelry, bars and coins, driving domestic prices above global benchmark rates and making it profitable to import bullion.

Other commentators however probe a little deeper.

An article in Zero Hedge written by the site’s Tyler Durden points out that two weeks ago, the IMF reported the global share of US dollar-denominated foreign exchange reserves fell to 59% in the fourth quarter of 2020, matching a 25-year low set in 1995.

Durden asks: Is this just the next stage in China seeing the writing on the wall for the US dollar as global reserve currency… and paving the way for a gold-backed yuan?

Let’s take a look at what we know. In 2018 China launched a yuan-denominated oil futures contract backed by gold. The move was at the time seen as a way for China to buy and sell oil without having to use US dollars.

The 2018-19 gold-buying spree by central banks (651 tons of gold was accumulated in 2018, the highest amount since the end of the gold standard in 1971, followed by 650t in 2019) was driven by the de-dollarization of countries like Russia, China and Turkey, which have an axe to grind with the US. They want to get out from under the thumb of Uncle Sam.

China also last week became the first major economy to unleash a central bank digital currency, “cementing its trailblazer status in virtual currencies far ahead of other countries, after already recently experimenting with large-scale trials of actual payments by consumers, which was met with mixed results,” Durden writes.

Finally, the Zero Hedge author quotes billionaire and PayPal co-founder Peter Thiel, who warned, “Bitcoin should also be thought [of] in part as a Chinese financial weapon against the US… It threatens fiat money, but it especially threatens the U.S. dollar.”

And while Durden acknowledges, through a 2020 article by Alasdair McLeod, that it is not in China’s interest to destroy the dollar (the country holds the most US currency, @ $3.5 trillion), in the event of a banking crisis that throttles fiat currencies, China will have no alternative to abandoning all attempts to support the dollar and its means of buying overseas influence. China will then need to secure its own currency [by introducing a gold standard and tying the yuan to gold – brackets mine].

Added up, these factors make an extremely interesting case for gold, amid China’s renewed interest in the precious metal as a way of further distancing itself from the United States.

Other central banks pile on

The People’s Bank of China is not alone in amassing gold right now — proving correct a World Gold Council (WGC) survey 11 months ago that indicated central banks were planning to substantially increase their stores of bullion over the next year.

An Indian government source told Reuters that its central bank imported a record-breaking 160 tonnes in March. The Polish central bank reportedly plans to buy 100 tonnes over the next few years, and in April, Hungary tripled its gold reserves to 94.5 metric tons from 31.5 tons, citing “long-term national and economic policy strategy objectives.”

Bullion Vault quotes the WGC’s Krishan Gopaul, senior analyst for Europe, the Middle East and Africa, saying that with 2021 expected to bring a global economic rebound, “The possibility of capital inflows into emerging markets and the [continued] low interest-rate environment may lead to central banks adding gold for diversification purposes.”

Indeed this trend already appears to be in play. As mentioned above, central banks in October sold gold for the first time in a decade, making them net sellers (more gold sold than bought) in the third quarter, but in February they became net buyers again, according to a World Gold Council report.

9.5% drop in gold supply

In a recent article we addressed the question of whether the world can produce enough gold to meet rising demand — especially considering we are entering what could be a particularly ugly period of inflation.

The latest World Gold Council report shows a 4% decline in total gold supply in 2020, compared to 2019. Mine production also slid 4%, to 3,401 tonnes, including just 896t in Q4, a five-year quarterly low. WGC attributes the decreased output to coronavirus disruptions.

Last year production from the world’s eight largest gold producers fell 6.5%, to 25 million ounces, owing to lower ore grades, asset sales, reduced mill throughput and lower recoveries, according to GlobalData, a UK-based data analytics and consulting company.

Newmont, Barrick and AngloGold suffered the worst production losses, with collective output dropping to 13.7Moz in 2020 form 15Moz in 2019.

GlobalData did the analysis, and although the research firm suggests production from the same top eight miners is expected to recover 3.1% this year, we note the following: recovering 3.1% from a fall of 6.5% means there will still be a drop of 3.4% in 2021. In fact, over the two years, if GlobalData’s 3.1% prediction comes true, the world’s top tier gold miners will have seen their total production drop by 9.5%!

Peak gold

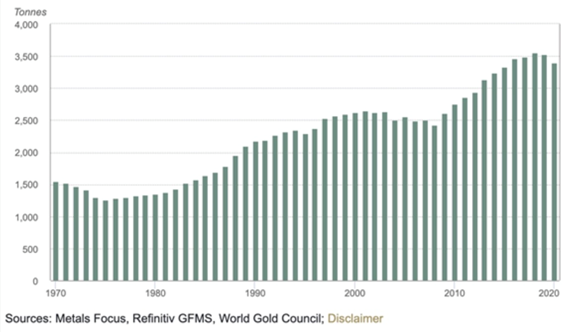

Our conclusion regarding gold supply? Peak gold was reached in 2019, the first year since 2008 that mine output dropped, and it has not increased since then.

In 2020 total gold supply including jewelry recycling reached 4,633 tonnes. Total demand was 3,759t — the first year under 4,000 tonnes since 2009.

No peak gold here, right? Demand is more than satisfied by supply.

But when we strip jewelry recycling from the equation, 1,297t, we get an entirely different result. ie. 3,759 tonnes of demand minus 3,401 tonnes of production leaves a deficit of 358t.

We at AOTH don’t count gold jewelry recycling. What we want to know, and all we really care about, is whether the annual mined supply of gold meets annual demand for gold. It doesn’t!

Only by recycling 1,297 tonnes of gold jewelry could demand be satisfied in 2020.

Are we alone in this peak gold assertion? No. In fact some heavy hitters in the gold industry are on board with it.

“Mine production has flat-lined, and is likely on a downward trajectory, but not dramatically so,” says Ross Norman of MetalsDaily.com, formerly the CEO of London-based bullion dealer Sharps Pixley.

Ok, so the decline isn’t dramatic. But it’s still a decline.

And gold reserves are dwindling.

In fact gold reserves have been receding for the past decade. Last September Mining Weekly reported that 16 of the world’s 20 largest gold mining companies, including the three mentioned above plus Kinross Gold, saw their mine lives reduced between 2010 and 2019. Kinross, for example, had just nine years of production left, compared to 24 years in 2010.

Only two of the gold companies analyzed by S&P Global Market Intelligence, Zijin Mining and Fresnillo, had more remaining years of production at the end of the period than at the start.

Gold companies whose assets are depleting often turn to competitors’ portfolios to replace their reserves. The more difficult means of creating new gold resources/ reserves is through exploration.

New deposits cost more to discover. This is because they are in far-flung or dangerous locations, in orebodies that are technically very challenging, such as deep underground veins or refractory ore, or so far off the beaten path as to require the building of new infrastructure from scratch, at great expense.

The costs of mining this gold are often too high. Only about one in three advanced-stage gold development projects ever become mines.

Within the past three years, there have only been three major gold discoveries, and just 25 in the past decade.

S&P Market Intelligence concludes additional grassroots exploration is needed to ensure there are enough projects in the pipeline to replace aging gold mines.

So far global gold supply is looking pretty bullish. Central banks have switched from sellers to buyers, especially China, which is planning to amass 150 tonnes, within the next six weeks. Mined gold production isn’t keeping up with demand, without recycling jewelry, and the reserves of the 20 largest gold mining companie have been in decline for a decade.

The only thing we haven’t looked at on the supply side is gold ETFs. Gold-backed exchange traded funds that trade on major stock exchanges offer an easy vehicle to play the gold trade, for those unwilling or unable to buy physical gold. Their inflows and outflows are a fair proxy for gold demand.

The latest data from the World Gold Council shows 107.5 tonnes flowed out of global gold ETFs in March — four of the past five months have seen outflows — as investors judged rising strength in the US dollar and higher US government bond yields as reasons to rotate funds out of gold.

Kitco quotes Juan Carlos Artigas, director of investment research at the WGC, stating that, while momentum in the gold market has definitely slowed compared to last year,

strategist investors continue to see long-term value in the yellow metal and are providing critical support.

Artigas also noted that investors also need to view the outflows in a broader context as last year saw historic ETF demand.

“It is natural for the gold market to see some outflows as investors continue to take profits from last year’s record rally,” he said. “This is a natural rebalancing of the gold market.”

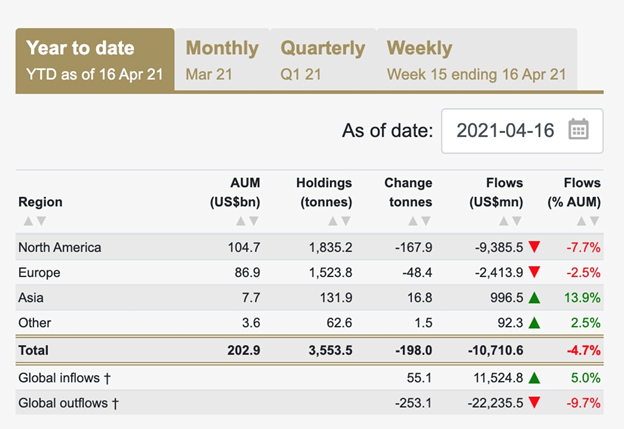

Year to date ETF activity, tabulated below by the World Gold Council, sees global inflows lagging outflow by 10,710.6 tonnes, showing that there may still be a fair bit of profit-taking left before gold investors decide a bottom is reached and start buying again.

Port shipments going bonkers

Continuing with gold demand, we note that the blistering speed of economic recovery in the US — economists are predicting annual GDP growth of 6.5%, versus a 2020 contraction of 3.5% — is stoking fears of inflation.

The consumer price index (CPI) jumped 0.6% in March, led by higher oil prices, and the 12-month rate of inflation rose to 2.6% in March from 1.7% in February, as the bar graph below shows.

The massive fiscal stimulus, which includes the trillions already spent on covid-19 relief and more to come with President Biden’s proposed $2 trillion infrastructure bill, and plans for education and health care, dwarfs anything even considered in the 1970s — when the United States suffered the last major bout of inflation.

Moreover, there is a palpable excitement that Americans will finally be able to discard the shackles of covid and spend the money they saved last year and the wages they’re starting to earn again. So demand is likely to soar.

In fact we already see evidence of this demand. On April 14 S&P Global Platts reported that the Port of Los Angeles — among the most active container ports in the world — had the busiest first quarter on record, handling upwards of 2.6 million TEUs (20-foot-equivalent units). In March alone, the 957,599 TEUs that passed over the docks was double the amount of cargo moved in the same month last year.

“The consumer spending surge continues unabated, with more of us vaccinated, businesses opening, economic outlook looks strong,” said Gene Seroka, executive director of the port. “Consumers are spending as fast as importers can stock their shelves.”

It’s hard to exaggerate what “busy” these days means at the LA port.

The influx of trade has created a congestion crisis, with an alarming number of ships at anchor, waiting for a berth.

The fiscal stimulus provided by the US government, including $1,200 cheques in direct aid, has meant a one-way flow of goods, ie., imports from Asia, mainly China.

“The port handled 490,115 loaded TEU imports, up 122.5% on the year. Firm consumer demand for furniture, home goods and appliances, athletic equipment and automotive parts helped drive the record number of imports,” Seroka said.

By comparison exports were only 122,899 TEU, up just 1.5% in March, year on year.

Higher demand has put pressure on freight rates and caused a serious shortage of empty containers in Asia, as loaded ones pile up at West Coast ports.

The shipping imbalance also sent the US trade deficit to a record high in February.

According to S&P Platts, the cost of shipping a container from North Asia to the West Coast of North America has skyrocketed to around $4,000 per FEU (40-foot equivalent unit), compared to just $630/FEU for the same-sized container traveling the other direction.

This, my friends, is cost-push inflation as I’ve never seen it.

Conclusion

Gold may have seen a pullback since the heady days of last summer when it was trading around $1,800, $1,900, even crossing over $2,000 briefly, but a perfect storm for gold is brewing once again.

Let’s look at the facts.

On the supply side, we have mined gold supply unable to keep up with demand — without recycling jewelry. Peak gold was reached in 2019 and output continues to lag. Last year the amount mined fell 6.5% and this year it’s predicted to fall 3%. Where I live that means a 9.5% decline over two years.

On top of this, the reserves of the major gold mining companies are depleting, and there is a dearth of new discoveries to replace them. Any junior gold company with a decent-sized, scalable deposit will surely be the belle of the ball as far as attracting potential acquirers or joint-venture partners.

China has just announced it is importing 150 tonnes of gold. Is it a coincidence that China also last week became the first major economy to unleash a central bank digital currency, and that the global share of USD foreign exchange reserves in Q4 matched a 25-year low? I don’t think so.

Since the trade war started between the US and China, Beijing has grasped at every opportunity to make itself independent of the US dollar-denominated trading system and this is more evidence of the fact. China has its Belt and Road, its five-year plans, and monopolizes several of the world’s most important metals markets. It doesn’t need the US and the country is preparing, through a massive influx of gold imports, for the time when the USD is no longer the reserve currency and the yuan can stand on its own, backed by gold.

The demand side of the equation for gold is also building, fast.

We already have negative real interest rates — always a positive for gold prices — the US Federal Reserve has said it will tolerate inflation beyond 2% (we are already at 2.6%) and has no intention of raising interest rates for the foreseeable future. Low rates are also great for gold prices, as is inflation, for which gold is the time-honored defensive play.

Anyone who buys groceries and gas is already seeing their purchasing power eroded on a daily basis due to inflation, and this inflation is usually not counted in official government statistics.

Unconvinced inflation is coming like a slow-rolling tsunami? Check out the ships lining up at the Port of Los Angeles waiting to unload their cargo originating from Chinese factories — purchased from the labor of American workers and a crisp $1,200 check (soon to be $1,400) from the US government.

Even with Trump out of the picture, the world is still a dangerous place, evidenced by what is happening in Ukraine right now.

Satellite images show Russia has moved warplanes to Crimea and bases near Ukraine, adding, states the Wall Street Journal, to its capability for military or political intervention.

Gold’s safe haven demand status is being triggered by what looks like an attempt to intimidate the Ukraine government and send a message to the Biden administration which has taken a hard line on Russia.

It’s hard to say how this one will play out, but from the factors we have outlined, all indications point to another gold run amid rising geopolitical tensions, tighter supply, central bank gold buying, low interest rates, negative real yields, and what could be the most inflationary period in decades.

(By Richard Mills)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Robert

“On Tuesday, the World Health Organization warned that global infections were reaching their highest levels, prompting many fund managers to rotate money into safe-haven bonds.” The higher the rate of infection, the higher the likelihood of governments printing money to aid the distressed, and hence the less safety investing in bonds, period.