The Metals Report: Mark, what is the supply situation with tungsten?

Mark Seddon: China accounts for approximately 80% of global tungsten supply, so it’s the clear dominant player when it comes to both tungsten and rare earth elements (REEs), both of which are on most national lists of strategic or critical materials. The Chinese government has recently taken an active role in managing supply for a broad range of strategic metals, including tungsten, through export quotas, mining quotas and licensing systems. These actions have reduced the availability of ores, concentrates and intermediate products available for export. China’s goal is to add value to their natural resources by serving its own domestic markets rather than export these materials—and refining and manufacturing jobs along with it. That dynamic applies to both tungsten and REEs.

“Tungsten is a very industrial metal. It’s mainly used as a carbide or ‘hard metal’ in drilling and cutting tools used in heavy industry. Tungsten is not sexy in that sense.”

Another similarity is the fairly significant price rises in both markets. But while REE price hikes have been labeled a bubble, that’s not the case with tungsten, simply because there has not been a lot of interest from the investment community. It is possible that a bubble in tungsten will happen in the future as investors see prices for products rising and that feeds a self-reinforcing investment case and increases investor interest. But we are not anywhere near that now.

There are notable differences between the two markets as well. One of the big differences between tungsten and REEs is their applications. Tungsten is a very industrial metal. It’s mainly used as a carbide or “hard metal” in drilling and cutting tools used in heavy industry. Tungsten is not sexy in that sense. It’s a very solid industrial market. This contrasts with REEs, which are used in a lot of newer, high-tech applications that are much easier for the investment community to make into an exciting story.

TMR: So, the tungsten narrative is a little more staid.

MS: Absolutely. Here in the U.K., the national press was running articles about REE production in China and how the Chinese might cut off supplies. The result would be no more wind turbines. That narrative is the type that gets lots of attention. Meanwhile, tungsten is used in industrial applications that people don’t get as excited about. The image of the market is quite different. Another thing to keep in mind is that tungsten is just a single element with a few critical applications, whereas REEs include a number of different elements with many applications.

TMR: How large is the tungsten market?

MS: I evaluate it in terms of volume. The global market is approximately 80,000 tons of tungsten metal content. When looking at supply/demand statistics, it is important to make sure that you are using consistent units. For clarity, I use tungsten metal content (W) rather than WO3 or other intermediaries.

TMR: Overall, is the tungsten market growing?

“Tungsten demand growth, over time, has consistently outperformed GDP.”

MS: The largest segment of the market is in cemented carbides or hard metals, which probably accounts for about a quarter of the market. Tungsten demand growth, over time, has consistently outperformed GDP. In the mid- to late eighties, for example, tungsten demand increased up to 8–10% a year when global GDP was growing at between 4–5%. The historical use of tungsten metal in mill products like filaments for light bulbs accounts for around 15% of the market. The demise of the incandescent light bulb is not a major problem for the tungsten market, as tungsten is still used in some of the newer light bulbs.

TMR: Part of the REE narrative is the limited ability to substitute other materials in specific applications. Are consumers of tungsten required to use tungsten for their particular applications?

MS: Pretty much. In most current applications, there aren’t any viable substitutes for tungsten. Demand for tungsten is therefore relatively inelastic to price changes. Five years ago, when prices started to increase, demand didn’t drop. In fact, demand was still growing at the time. Consumers require tungsten and are willing to pay for it. There’s no real substitute.

TMR: How do you track the pricing trends in the various global markets for tungsten?

MS: One feature of tungsten, as with REEs, is there’s no terminal market. There’s no exchange where you can pull up the tungsten price like you can do with copper, gold or wheat. You’re relying on price discovery publications like Metal Bulletin, Metal Pages and Metals Weekly. Depending where they’re published, they give you an idea of regional pricing. Metals Weekly is a U.S. publication, so it tends to focus on U.S. prices. Metal Bulletin is based in Europe. Metal Pages has a very strong Chinese office so it can watch Chinese prices closely.

Even with those sources, it is still difficult to get exact prices for materials due to the nature of the contracts. But over time, you can see trends developing. Recently, because the European market has been weak, European tungsten prices have lagged behind China, where the tungsten market is growing quicker. Chinese economic growth is still at 7–8%, so they’re in a different part of the cycle than Europe, which has been a bit of a disaster area. But European prices are now starting to catch up and are similar to the Chinese export prices at the moment. Due to the nature of the market, pricing differentials do pop up in different regions from time to time.

TMR: Are there large players that can set prices across regional markets?

MS: Not really. I suppose if you’re looking at the price for tungsten, your first port of call is China because it accounts for so much of the market. The Chinese export market sets the world price and that’s a price you can buy Chinese tungsten—if it’s available. In the U.S., companies such as Global Tungsten Powders and Kennametal Inc. are quite big purchasers. In Europe, major consumers could include companies like H.C. Starck and Sandvik, for example. Whether they’re big enough to set prices, I don’t know.

Tungsten tends to be produced and sold to the consumer on relatively longer-term contracts, so spot business is less important. People tend to form their contracts based on the Metal Bulletin or Metal Pages price or whichever price source they feel most comfortable with. The contract will be for a certain amount of tonnage over a certain period of time and it could be a premium or a discount to the Metal Bulletin published price, depending on grade and quality.

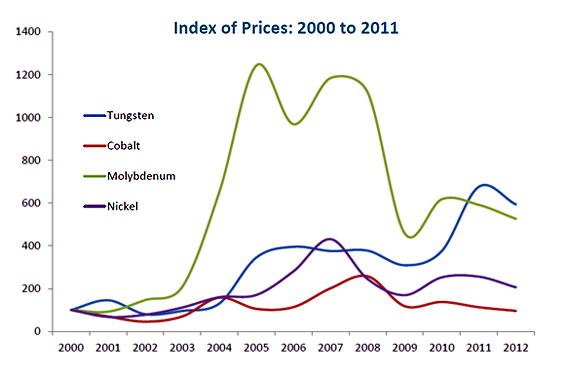

TMR: How is tungsten price performance right now?

MS: The tungsten market is performing pretty well when you compare it to other minor metals—over both short and longer-term time horizons. Tungsten prices have been increasing for about five months in a row now. [See the chart below.]

“Tungsten prices have been increasing for about five months in a row.”

The supply side will drive the tungsten price in the near future. China’s not going to change its strategic approach to natural resources management. The whole export license and export quota system will remain in place. Effectively, you’ll find less and less intermediate tungsten available for export from China. They’ll be shipping out more finished products whether it’s tungsten carbide powders, drill bits or cutting tools. The good news is that this presents an opportunity for tungsten mine projects.

TMR: In their yearly commodity summary for tungsten, the U.S.G.S. states that there are many tungsten mines throughout the world that are in various stages of coming on-line. Many of them are restarts of old mines. Will new mine supply make it to production given the difficulty of financing mining projects?

MS: You hit the nail on the head with financing. Securing funding is the biggest hurdle between projects and production at the moment. We’ve had many financial events over the past few years that have hurt confidence for lending. It’s not unique to the tungsten market—it’s pretty much universal. Tight lending is a macro condition that is working its way all the way down the food chain.

If you look at the fundamental situation, the tungsten market is going to need new production from somewhere. The Chinese aren’t pumping out extra tungsten. In fact, if anything they’re exporting less and less tungsten, particularly the intermediate and unrefined products. Demand in 2012 was level or down because of the problems in Europe. This year, I would expect demand to pick up a little bit.

The current producers of tungsten don’t have the capacity to materially increase production. The biggest mine outside of China, the Cantung mine in Canada, which is owned by North American Tungsten Corp. Ltd. (NTC:TSX), is producing at close to capacity and has only two or three years of reserves—and that’s a generous estimate. Most of the other mines, including a couple of mines in Europe, are producing close to capacity, so they don’t have much leeway. If demand starts to pick up, new projects or restarts will be needed to fill the gap.

“If tungsten prices do take off, as I expect they will, the beneficiaries should be the producers.”

In the last couple of years, the only major project that’s started production is the Nui Phao project in Vietnam, owned by Masan Group (private). It’s a Vietnamese company. That project has been through a number of hands and has been in development for quite a long time. At least $500 million ($500M) has been spent on the project. It is somewhat unique in that it is a polymetallic deposit. The process flow sheet is fairly complicated and getting the entire plant up and running will take some time. Other new producers include a smaller-scale operation in Australia andAlmonty Industries Inc.’s (AII:TSX.V) Los Santos mine in Spain. These are not particularly large projects, with annual production at less than 1,000 tons of tungsten each.

The largest projects in the tungsten market are up to $500M in size. That is small compared to world-class gold or copper projects. But it is large for this market, and far larger than many of the smaller mining companies can pull off. In that sense, the tungsten market falls between large-scale and small-scale mining. And there might be an opportunity in that space. You could say that the tungsten market “falls between two stools.”

In the context of an approximately 80,000-ton annual market with 3% growth, you need 2,400 tons of additional tungsten metal per year in supply, and with 5% growth you need 4,000 tons. That’s one new big tungsten project per year. It is difficult to see where that supply could come from. In the current market, miners can’t get the financing needed to take projects from a bankable feasibility study to construction. It’s a big problem.

The only other apparently fully funded project that I know of is the Hemerdon project in the U.K., which is owned by Wolf Minerals (WLF:ASX). That project is beginning construction now, but won’t be in production until late 2014 at the earliest. There aren’t any other significant projects that will come on-line in less than two years. Most of the larger projects have at least a two-year construction phase, but most of those projects aren’t fully funded yet. The fundamentals in the tungsten market are good. Price projections for tungsten are good. The problem is getting the funding. Add it all together and it appears that the tungsten market is storing up trouble. For many reasons, the tungsten market isn’t well understood by the investment community. The problem is that whoever’s looking to fund a project is waiting for tungsten prices to go crazy and then they’ll get involved. If an investor waits until then, the timing is just not right.

TMR: What are the ways investors can get exposure to the tungsten market? Are there ways to get exposure through refiners or specialty chemical makers? Is there any practical way to buy the physical commodity?

“Investment in mining companies is the only practical way to access this market.”

MS: Investment in mining companies is the only practical way to access this market right now. Tungsten is one commodity that’s mostly traded between producers and consumers. Historically, governments would enter the market and stockpile, but as an individual investor, you can’t really go out and easily buy a couple of tons of tungsten and warehouse it. That would be far outside normal market behavior.

If tungsten prices do take off, as I expect they will, the beneficiaries should be the producers. One of the larger current producers outside of China is North American Tungsten. Its current production comes from the Cantung mine, which hasn’t got much life left in it. The company has additional projects, like Mactung, that may be able to come on-line. A potential investor would need to examine each project closely.

In evaluating projects, investors have lots of variables to consider. What are comparable projects? What are the size, grade, operating costs and all the other details that need to be evaluated? Most importantly—what’s the funding situation? It is not always clear as to why some projects advance and others don’t. Mining is a risky business, but that is why there are rewards when it works out.

TMR: It has been great to talk to you.

MS: It has been a pleasure.

Mark Seddon has over 25 years of experience in the commodities industry as a trader, researcher, consultant and company executive. Seddon is an acknowledged expert in the tungsten market and writes a number of Roskill’s tungsten reports. He has presented papers on various minor metals at international conferences and was a speaker at the most recent International Tungsten Industry Association (ITIA) Annual General Meeting.

Want to read more Metals Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Metals Report homepage.

DISCLOSURE:

1) Alec Gimurtu conducted this interview for The Metals Report and provides services to The Metals Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Metals Report: None. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Mark Seddon: I or my family own shares of the following companies mentioned in this interview: None. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Comments