Silver demand to exceed supply again this year

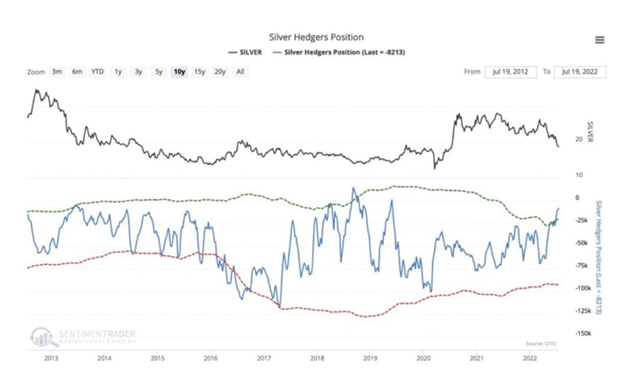

The pain in the silver market could soon find some relief. While the monetary and industrial metal is down substantially from a year ago (-27%), King World News points to the latest Silver Hedgers Position report as showing “The setup in the silver market has turned extremely bullish.”

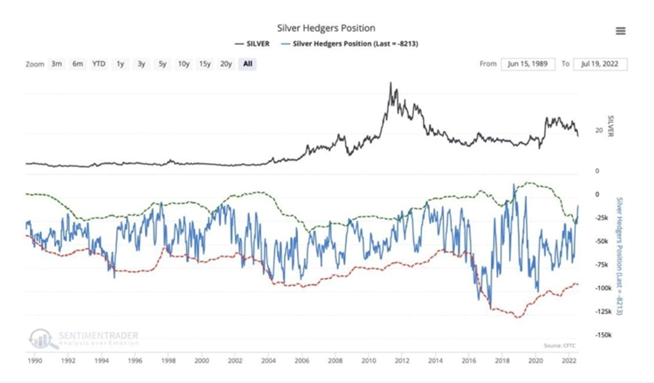

The chart below shows commercial traders “are now in one of the most bullish positions in the last decade.” The second chart offers a multi-decade view of how bullion banks and commercial traders have been positioned in the silver market. “There is no question the setup in the silver market is extremely bullish at this point from a historic perspective,” King World News writes, adding that “right now and on any further weakness it is a good idea to be extremely aggressive in accumulating physical silver.”

But why silver, and why now?

Like gold, silver functions as a safe haven in times of economic uncertainty. And its lower price, currently 1/87th the cost of gold, makes it the “poor man’s alternative” flight to safety.

This explains silver’s excellent performance in 2020, as investors piled into precious metals due to the panic in the financial markets caused by the coronavirus.

While gold took about a year and a half to move from $1,300 to a record $2,034, in August 2020, silver made tracks in just six months — shooting from $13 in March 2020 to $28 in September 2020. It could easily happen again.

Silver is vulnerable to supply disruptions, more so than gold, because there are relatively few pure-play silver mines.

In 2020, mined silver slumped the most in a decade, owing to a number of coronavirus-related mine closures in Latin America where the majority of silver is produced.

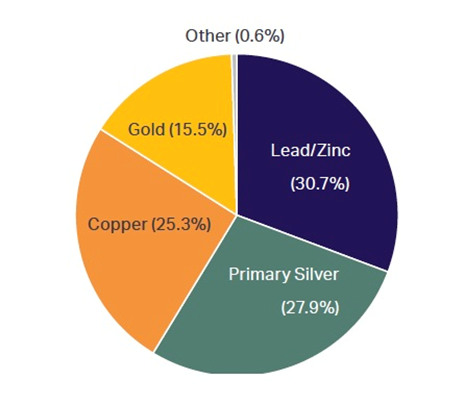

In fact, only around 30% of annual supply comes from primary silver mines. Over two-thirds is sourced from polymetallic ore deposits, including lead/zinc operations, copper mines and gold mines.

“Native silver” found in the Earth’s crust on its own, is relatively rare. More commonly, it is mined alongside gold, or as a by-product of zinc-lead ore.

While most mined gold is still in existence, either cast as jewelry, or smelted into bullion and stored for investment purposes, the same cannot be said for silver. It is estimated around 60% of silver is utilized in industrial applications, leaving only 40% for investing. Of the 60% used for industrial applications almost 80% ends up in landfills.

Despite silver being about 17.5 times more plentiful than gold in the Earth’s crust, silver and gold have roughly the same amount, ~2.5 billion ounces, available for investment purposes.

However, since very little gold is used by industry, it trades as an investment commodity — prices moving up and down in relation to factors like the US dollar, inflation, interest rates and sovereign bond yields.

In comparison, silver commands a relatively small amount for investment, just 40% of supply. Because over half of supply is needed for industrial applications, silver usually trades more like an industrial metal than an investment commodity. But when it trades as a monetary metal moves are explosive…

Silver survey says…

2021’s Silver Institute Survey made headlines for being the first year since 2015 that the silver market recorded a deficit. According to SI, “All areas of silver demand strengthened, boosted by a post-pandemic recovery in activity, secular factors driving industrial offtake and a surge in retail investor appetite for the metal.”

The largest area of demand volume came from coin and bar purchases, followed by industrial demand, with the latter due to a resumption of industrial operations and the re-opening of businesses following covid-19 lockdowns and restrictions in 2020-21. Industrial fabrication rose by 9.3% to 508.2 million ounces, or 15,087 tonnes, which was the highest tracked by the Silver Institute since 2010.

This year, the Silver Institute says that higher mine production, due to both project ramp-ups and some gains in established mines’ output, coupled with a rise in industrial recycling, will drive a 3% increase in global silver supply. This will not be enough to meet global demand, which is forecast to rise by 5%, thanks to gains in industrial fabrication and a continued post-pandemic recovery in jewelry and silverware. (more on the expected supply deficit below)

While rising US interest rates will put pressure on the silver price, a number of supporting factors should limit the decline in its full-year average to 5%, says SI. For instance, while Fed Funds Futures suggest an interest rate of nearly 2.5% by year end (we’re there already, on Wednesday the Federal Reserve enacted its second consecutive 0.75% increase, taking its benchmark rate to range of 2.25-2.5%), the Silver Institute “finds this excessive,” arguing that “expectations sooner or later will be adjusted, which should offer silver some support.”

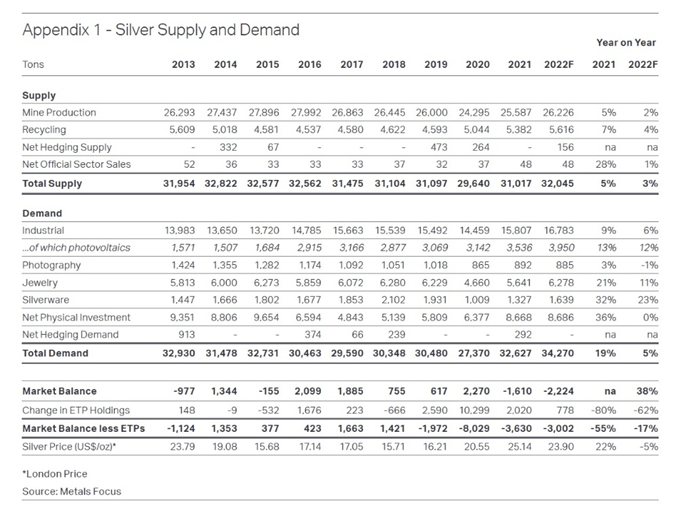

In Appendix 1 below, the Silver Institute forecasts total silver supply in 2022 will reach 32,045 tons, not enough to match the 34,270 tons of silver demanded, leaving a market deficit of 2,224 tons.

Global silver mine production is expected to rise 2.5% compared to last year, reaching 843.2 million ounces or 26,226 tons, with the biggest increase likely to come from Mexico. The biggest decline will come from Peru, a loss of 365 tons, mostly due to the suspension of Uchucchacua in the fourth quarter of 2021, to allow Buenaventura to undertake development work aimed at improving the economics of the mine. Also, the Russia-Ukraine conflict led to Kinross suspending operations at its Kupol mine in early March, which produced 3.3Moz (104t) in 2021.

As mentioned the majority of silver is produced as a by-product of other metals, including lead-zinc, copper and gold. According to the Silver Institute, by-product silver production this year is expected to increase mostly from primary gold mines, driven by higher output from several existing operations, along with the commissioning of the silver-rich La Coipa gold project in Chile.

Over the longer term, meaning four to five years out, output will begin to decline unless sufficient investments are made to bring earlier stage projects on-line. A re-start of Pan American Silver’s Escobal mine in Guatemala, which has been in care and maintenance since 2017, would have a meaningful impact on global output. However, consultations with the local community aimed at a potential re-start are still at an early stage, the Silver Institute explains in its World Silver Survey 2022.

On the other side of the ledger, strong demand for silver in 2021 is expected to have momentum. According to SI, Industrial demand is forecast to rise 6% to a new record high this year. On top of global GDP growth, end-use in the green economy will benefit from rising vehicle electrification and as the geopolitical conflict also boosts investment in renewables, especially photovoltaics.

While the war in Ukraine has hurt the recovery in vehicle output and introduced uncertainty, and photographic demand is set to fall again this year, jewelry fabrication is expected to rise by 11%, surpassing 2019 levels. Net physical investment will likely be flat in 2022, however the Silver Institute forecasts a gain of 778 tons for exchange traded products (ETPs), their fourth consecutive annual rise.

Their popularity will likely be boosted by a decision last year by the Securities and Exchange Board of India to allow the launch of silver ETPs. India is currently the world’s third largest physical silver investment market after the US and Germany. According to the report, as of February 2022 there were three active ETPs in India with a combined AUM (assets under management) of USD$82 million.

Through ETPs, the institute expects Indian silver investment to grow, adding to the extremely successful silver bar market in India, that has seen around 500Moz, or 16,000 tons, bought over the last 10 years.

The Silver Institute’s long-term demand forecast is quite positive, with projected successive record highs driven by silver’s potential for green energy applications and new, emerging uses.

Last year, 20 countries achieved 1 gigawatt (GW) of solar power, helping photovoltaic (PV) installations to reach 3,5336t, close to 11% of total silver demand. This occurred despite an 80% reduction in silver loadings per cell over the past decade. PV silver demand is expected to stay strong as growing capacity additions counter the negative of finger width expected to drop a further 30% by 2025 (finger width is the width of the lines of silver paste that are printed onto the front and rear of panels to collect deliver the DC current).

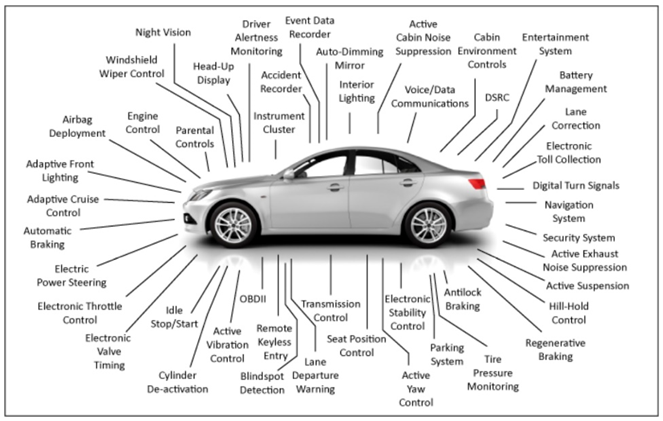

Much of the growth in automotive silver demand is due to the increasing number of devices, that are used to control a variety of features including safety and entertainment systems. These devices use a multitude of contacts, wires and electronic components that all contain silver, an excellent electricity conductor.

Additional demand is being created by electric vehicles, where silver is largely consumed in the main electrical connector material in the battery packs, in the surrounding control modules, and as the most efficient/ reliable material for cables in onboard charging equipment. Both hybrids and even more so, battery electric vehicles, have higher silver loadings than internal combustion engine equivalents. A further boost for silver is the demand for ancillary equipment, especially in-house chargers and curb-side charging stations.

The Silver Institute says the shift to EVs has also pushed investment in autonomous driving, resulting in growing demand for silver-coated or silver-alloy wires, that provide high-frequency transmission of big data.

According to SI, “surging battery demand from the automotive sector is still outstripping supply capabilities and creating challenges to secure various raw materials.”

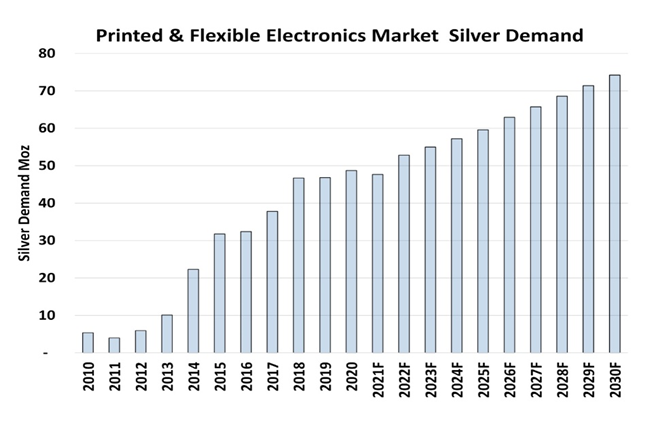

Then there is silver demand for “printed and flexible electronics”, forecast to increase 54%, from 48Moz in 2021 to 74Moz in 2030, meaning a consumption of 615Moz during this time frame.

A Silver Institute news release describes them as “mainstays” in a variety of electronic products, including sensors that measure everything from temperature, pressure and motion, to moisture, relative humidity and carbon monoxide. They are also used in medical devices, mobile phones, appliance displays and consumer electronics.

On top of silver’s use in solar cells, industrial fabrication, and the automotive industry, future demand is also likely to come from the field of nanotechnology, thanks to silver’s unique properties, such as high conductivity, resistance to oxidation and its anti-microbial nature.

Applications include the food industry, such as packaging with anti-microbial coating that improves shelf life, and quality monitoring performed by gas sensors. Here, silver can indicate the presence of gas through oxidation. For example, methane or ethanol can be measured to indicate spoiling, or ethylene to indicate ripeness — information used to determine when food should be shipped.

Gas sensors can also be used to monitor pollutants in the environment such as formaldehyde, often found in paint, or in the medical sector, where a person’s breath sample could be used to detect diseases including diabetes and cancer.

Inventory depletion

Because so little silver is available, above-ground silver stocks are closely monitored for signs of depletion.

Remember, 60% of silver is utilized in industrial applications, leaving only 40% for investing. Of the 60% used for industrial applications almost 80% ends up in landfills.

From 2010 to 2020, total silver supply exceeded demand, fueling a cumulative rise of 9,709 tons during this period. But when last year’s supply shortage of 1,102t is combined with the Silver Institute’s forecasts, it points to a decline in silver inventories of 9,212t, from 2021-26 (excluding retail investors’ bar and coin holdings).

Of particular interest is the trend of falling commodity-exchange silver stocks. According to SI, in 2021 inventories at Comex-approved depositories fell by 1,270t, as did exchange stocks in China, as the local price discount created arbitrate opportunities.

The downtrend in reported (vs unreported) silver stocks continued into 2022, with London Metal Exchange inventories slipping by 934t in January and February, and those on the Comex dropping by 480t to late March. Chinese silver exchange stocks are also down. According to Metal Focus, and already mentioned above, in bold, there will be a 2,224-ton deficit in the silver market this year, that will need to be filled by the mobilization of above-ground inventories.

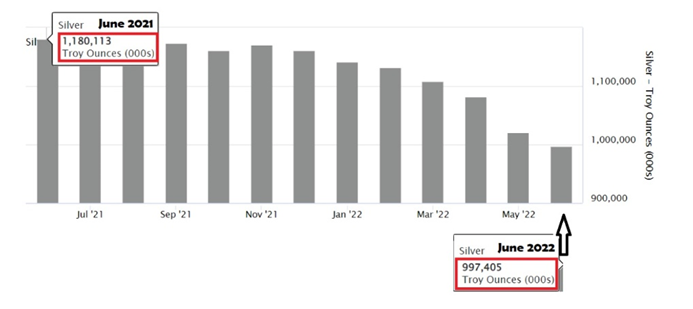

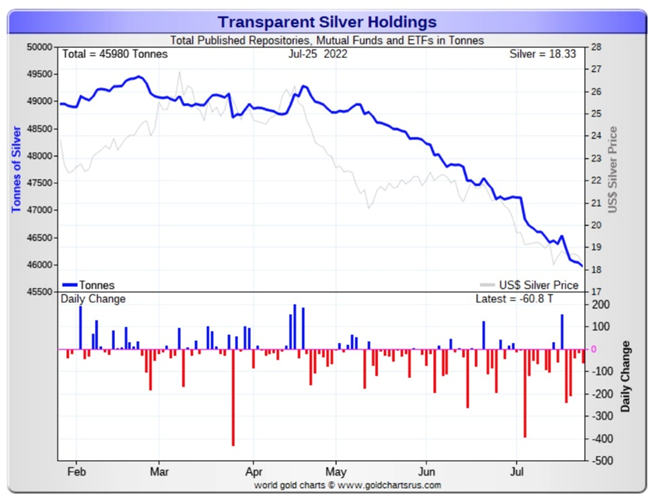

This could prove to be a challenge, considering that the quantity of silver held in London Bullion Market Association (LBMA) vaults, has been hemorrhaging for the past seven straight months. Ronan Manly, a precious metals analyst with Bullion Star, sourced the data. It shows LBMA vaults now hold less than a billion ounces (997.4Moz or 31,023 tonnes), which is 15.4% lower than a year ago (to end of June), when silver inventories sat at 1.18 billion ounces, or 36,707 tonnes.

Manly notes that June 2022’s LBMA silver holdings are the lowest silver inventories since December 2016 and the first time since November 2016 that inventories have fallen below 1Boz. Also, there has never before been a seven-month period, or six months, during which LBMA silver stocks fell consistently every month.

Manly suggests that owners of silver-backed ETFs are flirting with danger due to the London Bullion Market Association holding such a small amount of silver available for satisfying investment demand.

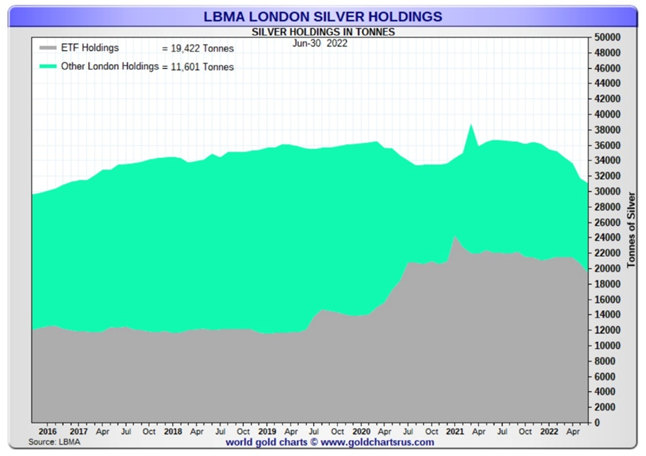

While the association on its website claims that the silver and gold held in LBMA vaults “underpins the physical OTC (over the counter) market,” the reality is the majority (nearly 63%) of this silver is owned by exchange-traded funds such as the iShares Silver Trust (SLV), the Wisdomtree Physical Silver ETC (PHAG), and the Aberdeen Physical Silver Shares ETF (SIVR).

In other words, at the end of June only 11,601 tonnes of silver, or 37.5% of the 31,023t held in LBMA vaults, were not held within ETFs, which together own 18,835t. Not counted here is the amount of silver held by Bullion Vault and Gold Money clients. Adding these to the ETF total means that, as of July 26, 19,154 tonnes of silver (of 31,023t) in LBMA vaults was held by silver-backed ETFs and private client investors.

Recall that during the “silver squeeze” of early 2021, 28,698 tonnes (or 922.65Moz) of silver, accounted for in the combined ETFs and BV/GM holdings, represented a massive 85.4% of all the silver that the LBMA claimed was in the London vaults — leaving under 5,000 tonnes to meet all other silver demand.

Manly wrote at the time,

This then gives an estimate of how much room these ETFs have before they hit a wall of not being able to source any more silver in the London vaults without having to import it or ship it in. And the answer… is not that much room at all.

Here’s where it gets interesting.

Manly believes, and I’m inclined to agree with him, that the reason silver inventories have dropped so much since early December is a concerted effort by the bullion banks to suppress the silver price.

Start with the assumption that, if the global silver market is in deficit, with demand outstripping supply, the market has to find supply by tapping above-ground stockpiles. This includes both reported inventories, such as metal held by the LBMA and Comex, and unreported inventories whose custodial stockpiles remain opaque.

Silver supply is only set to reach 32,000 tons in 2022, against 34,000 tons of demand. Manly maintains that “as witnessed in early 2021, the bullion banking cartel is terrified of the silver-backed ETFs gobbling up greater percentages of the London LBMA vault stocks… It’s as if they are inducing the ETFs to shed silver by creating a lower silver price to literally flush silver out of the ETFs.”

The chart below proves there is some truth to this assertion. It shows a strong correlation between a sharp fall in the silver price since mid-April (the light gray line), and reductions in the amount of silver held in silver-backed ETFs (the blue line).

He argues this flushing out serves two purposes:

- It creates a negative psychology and prevents ETF investors adding buying pressure that might break the LBMA shell game and lead to a situation where there is not enough metal in London to fulfill ETF silver demand;

- It flushes out existing silver from the ETFs that can then be channeled off into meeting physical silver demand requests coming in from all over the world.

Conclusion

Silver market manipulation? Say it isn’t so! Earlier this month, it was reported that three former JPMorgan traders are accused of manipulating the gold market. The trio are charged with racketeering conspiracy as well as conspiring to commit price manipulation, wire fraud, commodities fraud and spoofing from 2008 to 2016. Spoofing, banned in 2010, involves large orders that traders cancel before they can be executed in a bid to push prices in the direction they want to make their actual trades profitable.

It has long been suspected that the silver market is being equally manipulated, so the manufactured silver squeeze in the London bullion vaults described above by Manly, certainly comes as no surprise.

It makes sense during a period when the silver price, down 27% from a year ago, appears to have become disconnected from market fundamentals. How can we have a falling silver price when demand is exceeding supply by over 2,000 tons?

While part of the answer is clearly Fed-induced interest rate hikes that have sucked much of the wind out of gold and silver prices this year, arguably this isn’t the whole story.

As we stated in a previous article, increasing rates only makes sense if the economy can handle them; at a certain point, high inflation plus high interest rates will squeeze economic growth, prompting the Fed to reverse course, and begin lowering interest rates again.

There is ample evidence to show we are closer to this point than many think, and that the Fed could switch to lowering rates as early as the fall.

Economists see a sharp slowdown in job growth of 193,000 on average over the next 12 months, while the unemployment rate could edge up to 4.2% from 3.6%, according to Bankrate’s poll of the nation’s top economists.

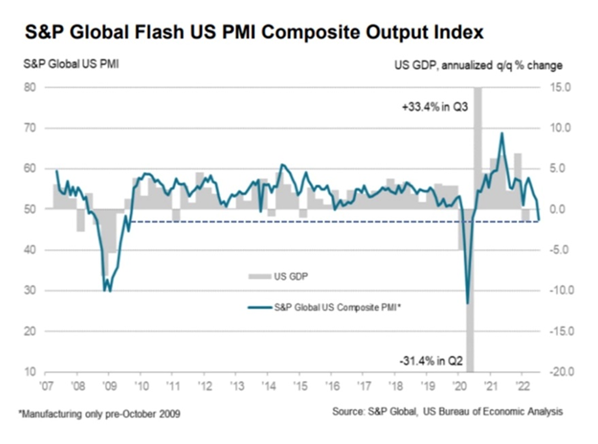

The Producers’ Manufacturing Index is showing weakness, as high inflation impacts customers’ ability to pay, and higher interest rates make borrowing more expensive. As the chart below shows, the S&P Global Flash US PMI Composite Output Index fell for the first time in over two years (26 months). Manufacturers and service providers both reported subdued demand conditions.

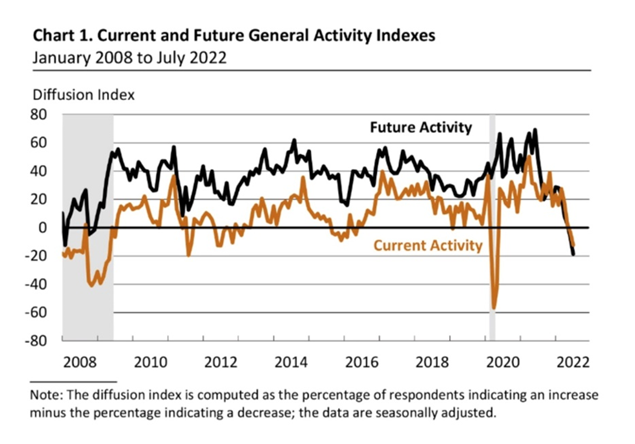

Last week the Philadelphia Fed Manufacturing Index plunged for the fourth straight month. Even more worrying was the gauge of future economic activity, with -18.6 indicating the worst reading since 1979.

Economists in Bankrate’s Second-Quarter Economic Indicator poll put the chances of a recession in the next 12-18 months at 52%, on account of the Fed’s more aggressive stance. A separate poll by Reuters found a 40% likelihood of a recession over the next year, and 50% within two years.

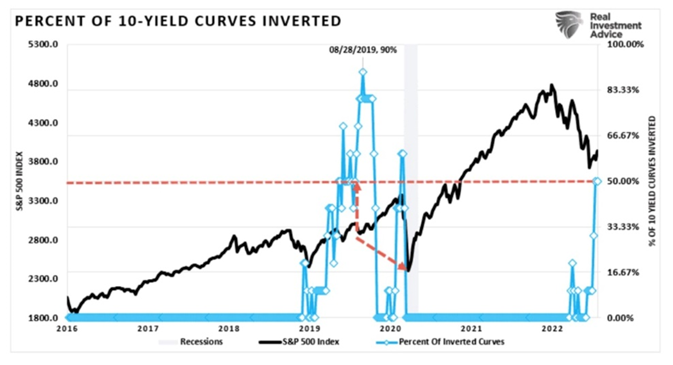

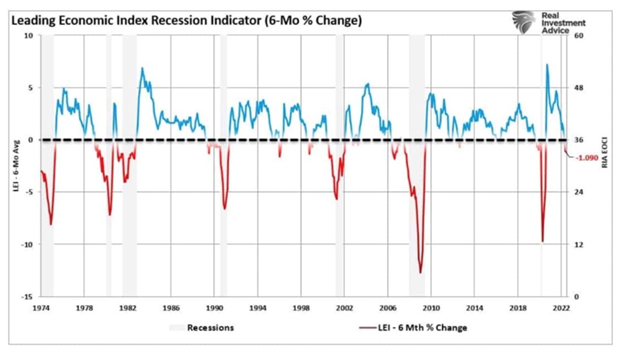

In a recent article, Real Investment Advice notes there are two indicators warning of a recession, both of which have near-perfect track records. The first is that currently, 50% of the 10-year spreads they track are inverted, as the chart below shows.

The second is the Leading Economic Index’s 6-month annual rate of change. According to RIA, the chart below showing the 6-month rate of change turning negative, either precedes outright recessions or near-recessionary environments.

Cue media reports on Thursday that the US economy shrank for a second quarter in a row — the classic definition of a recession. The Wall Street Journal cited a housing market buckling under rising interest rates, and high inflation taking the steam out of business and consumer spending. GDP growth fell in the second quarter by 0.9%, following a 1.6% contraction during the first three months of 2022.

In my opinion it’s only a matter of time before the Federal Reserve’s failure to control inflation, through a hawkish interest rate policy that is killing economic growth and leading rapidly to a recession, results in a “Fed pivot” wherein interest rates start heading down again.

It could happen as early as the fall.

When the monetary doves are back in charge, I expect precious metals to come roaring back, possibly testing highs seen two years ago.

Gold and silver stocks are deeply oversold and they could move forcefully to the upside. To avoid missing out I’m buying discounted quality juniors now, while they are on sale.

(By Richard Mills)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments