Supply risks fuel uranium’s flight to more than 16-year peak

Uranium prices have hit their highest in more than 16 years on a buying frenzy triggered after the world’s largest miner of the nuclear fuel highlighted production risks, but the price surge is likely to mean the restart of mothballed capacity.

Kazakhstan’s Kazatomprom earlier this month said it may cut its 2024 production plan due to difficulties with the availability of sulphuric acid needed to produce uranium.

Uranium oxide prices, under pressure for years after the Fukushima nuclear accident in 2011 battered demand, picked up momentum in August 2021 when disruptions caused by Covid lockdowns hit supplies and created shortages.

They have since rocketed 250%, and are up 15% so far this month to their highest since November 2007 at $106 a lb.

“After a decade of dormancy, uranium suddenly came to life in mid-2021, rising above its long-standing cap at $30 a lb, which also happens to be the global industry’s marginal cost of mined production,” said Liberum analyst Tom Price.

Marginal costs of production are a reference to the costs incurred per lb of additional output by the highest-cost producers.

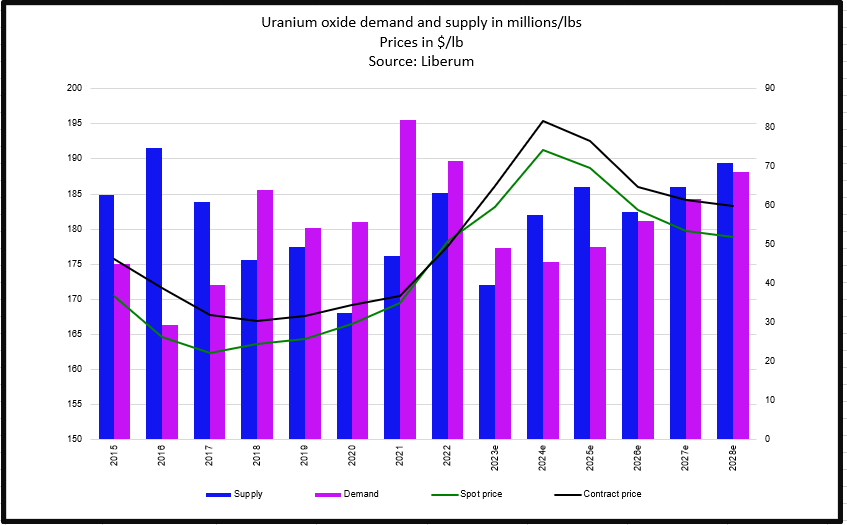

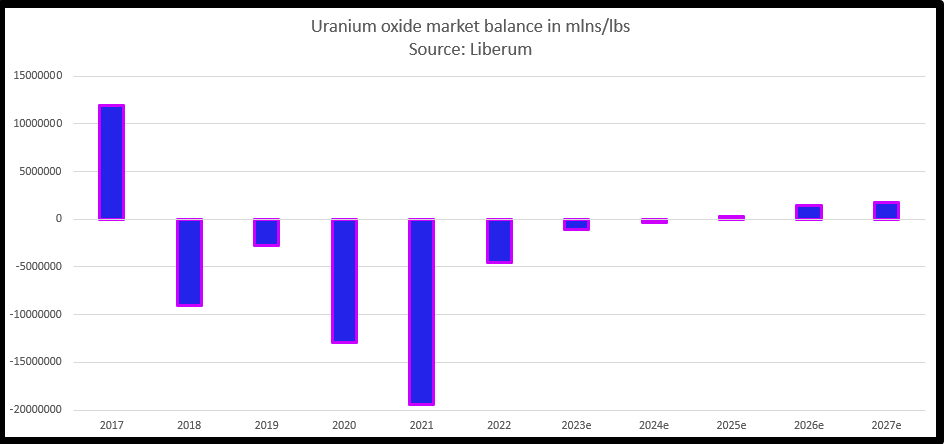

Liberum forecasts a 300,000 lb deficit this year, down from a shortfall of 1.1 million lbs in 2023, and estimates 2024 demand at 174.7 million lbs, up from 170.4 million lbs last year.

However, “while we recognize upside price risk, we also expect Kazatomprom and Cameco to eventually reactivate their dormant mine capability, as the price rallies – to secure market share and deter entrants,” Price said.

He did not give a timeline for re-starting mothballed capacity.

Toronto-listed Cameco is expected to be the world’s second largest uranium producer this year after Kazatomprom.

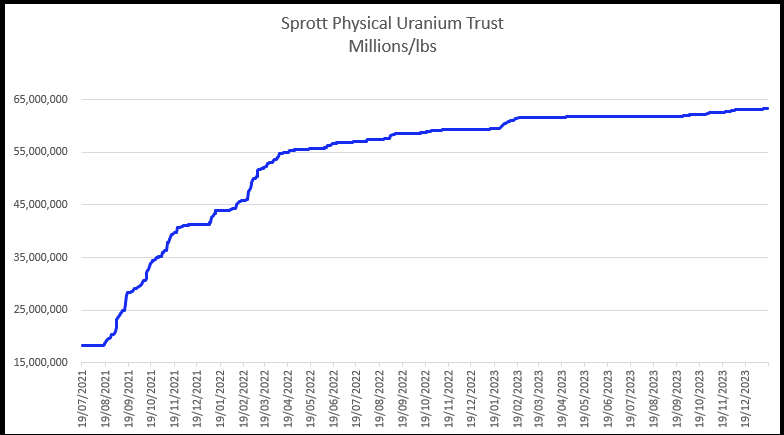

Uranium purchases by companies including the Sprott Physical Uranium Trust and Yellow Cake have contributed to the price surge in recent months, but this, industry sources say, would be due to demand from investors looking at supply/demand imbalances.

Resistance to nuclear power after Fukushima remains, but the need to cut emissions and a growing belief that it would make the energy transition safer and cheaper is expected to drive uranium demand higher over the coming years.

“Uranium is having a moment on the demand side. It is cost effective. If it isn’t green, it is certainly green adjacent,” said Jay Tatum, portfolio manager at Valent Asset Management.

“It would be hard to call a top in uranium prices, but five, six, seven years down the line, I don’t think it will be making new highs.”

(Reporting by Pratima Desai; Editing by Jan Harvey)

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments