Trump last week said he would impose tariffs of 25 percent on steel and 10 percent on aluminum, sending countries scrambling to negotiate exemptions. (Image courtesy of Shutterstock)

(Bloomberg Prophets) —The 10-year Treasury yield is one of the best metrics for predicting the direction of commodity prices. Its increase in recent months indicates that commodities have more room on the upside. The correlation between commodity price and the 10-year has been strong over time, for a number of reasons.

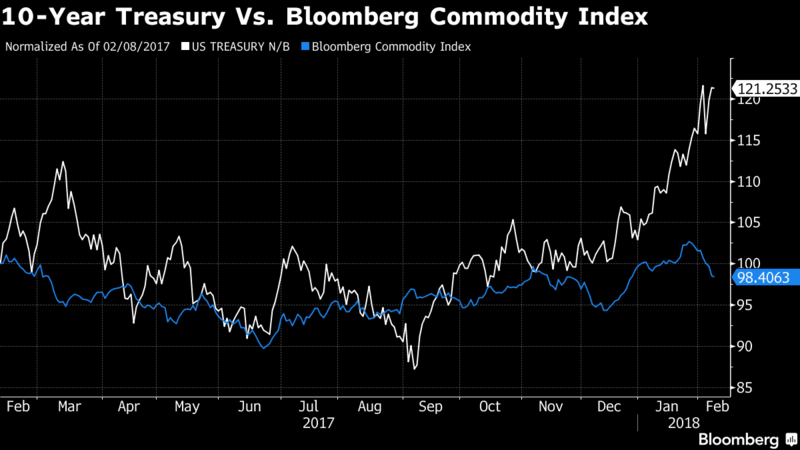

Interest rates are one of three elements that help determine the intrinsic price of a commodity. The other two are storage costs and insurance, because there’s a “cost of carry” to both store and insure commodities. These three factors determine the price of a commodity at each point along its forward (physical) curve or futures (financial) curve. Prices then move based on fundamental factors (global supply and demand), macro drivers (including the strength of the dollar), and technical factors (charting price and volume), which all influence each price along the curve. The chart below tracks the 10-year and the Bloomberg Commodity Index.

So, why focus on the 10-year? It can take that long if not longer to develop a gold mine, construct an aluminum smelter or cultivate a timber plantation, particularly given the legislative and environmental roadblocks that can delay a project. That means it could be a decade before new supply comes onto the market to potentially pressure prices downward. For this reason, the 10-year is a more reliable indicator than shorter-term interest rates.

Treasury yields show how investors feel about the economy in the future, which influences spending habits today. Rising yields are generally a reflection of a stronger economy and heightened confidence. Manufacturers then build plants and grow inventories to respond to greater demand.

Why not just look at the U.S. federal funds rate or a basket of global money market rates such as the London interbank offered rate or the Euro interbank offered rate? As most global commodities are priced in dollars, it makes sense to focus on U.S. rates. But that decision has more to do with the relative value between today’s rates and long-term ones than with individual yields. The higher the yields on 10-year relative to short-term rates, the better the economic outlook. The rise of the 10-year at the present indicates expectations of a strong economy and a greater desire to spend today in order to avoid paying higher prices in the future, which, in turn, drives up the prices of raw materials.

As with interest rates, the vast majority of activity in commodity markets takes place along the forward curve. In the physical markets, producers and consumers plan ahead by entering into forward purchase and sales contracts. But what if there’s urgent demand for a commodity? Say, for example, an industrial food processor has run out of soybeans and requires an immediate shipment. It generally takes time to get that delivery to the processor’s door. As a result, a very small share of commodities futures is traded on the spot month.

As most global commodities are priced in dollars, it makes sense to focus on U.S. rates. But that decision has more to do with the relative value between today’s rates and long-term ones than with individual yields

The spot contract is generally traded when a futures position, long or short, is being closed out or rolled to a longer-dated contract. Producers and consumers may have leeway as to when to ship or take delivery, and can choose to store the commodity, based on forward prices and expectations. That latitude, along with market expectations, will vary among suppliers, processors and investors, as each seeks to either hedge or profit from their respective decisions. While most commodities are traded out in less than 10 years, the 10-year bond is a liquid, reliable instrument.

Should long-term rates rise enough that inflation becomes a concern, investors will turn to commodities like gold and crude oil as havens. In addition, governments of heavy commodity-importing nations may hoard inventory as they did in 2008, severely driving up prices of commodities such as wheat and copper. And portfolio managers will turn to commodities as a way to diversify as they sell equities, which tend to suffer in high-interest rate environments as borrowing costs for businesses rise.

The recent surge in volatility across all financial markets reflects a fear of an overheating of the U.S. economy, which would be a signal of inflation to come. So, keep an eye on the 10-year Treasury and consider increasing commodity investments should the rate continue to rise. The Federal Reserve is expected to raise interest rates approximately three or four times in 2018.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Comments