Tesla’s reluctant commitment to cobalt a warning to others

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

The unpredictable Elon Musk strikes again.

Just when his electric vehicle (EV) company Tesla seemed to be pivoting away from using cobalt in its batteries, it signs a long-term supply deal for the controversial metal with Glencore.

This from the man who has vowed to eliminate cobalt from the Tesla product mix because of its financial cost and the reputational cost of a metal associated with child labour and poor safety conditions at artisanal mining operations in the Democratic Republic of Congo, the world’s dominant producer.

Tesla’s not the first auto company to lock in future cobalt supplies with a miner. BMW did the same last year, also with Glencore as well as with the Bou-Azzer mine in Morocco.

But Tesla is the standard-bearer for the EV revolution and its deal with Glencore has strategic significance for the global battery raw materials supply chain.

It’s a boost for cobalt’s prospects, both in terms of physical demand and, more importantly, in the apparent admission that cobalt isn’t going away as a battery material any time soon.

It’s also a warning to other auto companies that if they want cobalt, they’re going to have to take control over their own supply chain.

Battery choice

Tesla and its battery partner Panasonic have until now largely used a nickel-cobalt-aluminium (NCA) formula in their lithium-ion batteries.

Other automotive companies targeting the passenger vehicle market have adopted nickel-manganese-cobalt (NMC) technology.

Tesla is the standard-bearer for the EV revolution and its deal with Glencore has strategic significance for the global battery raw materials supply chain

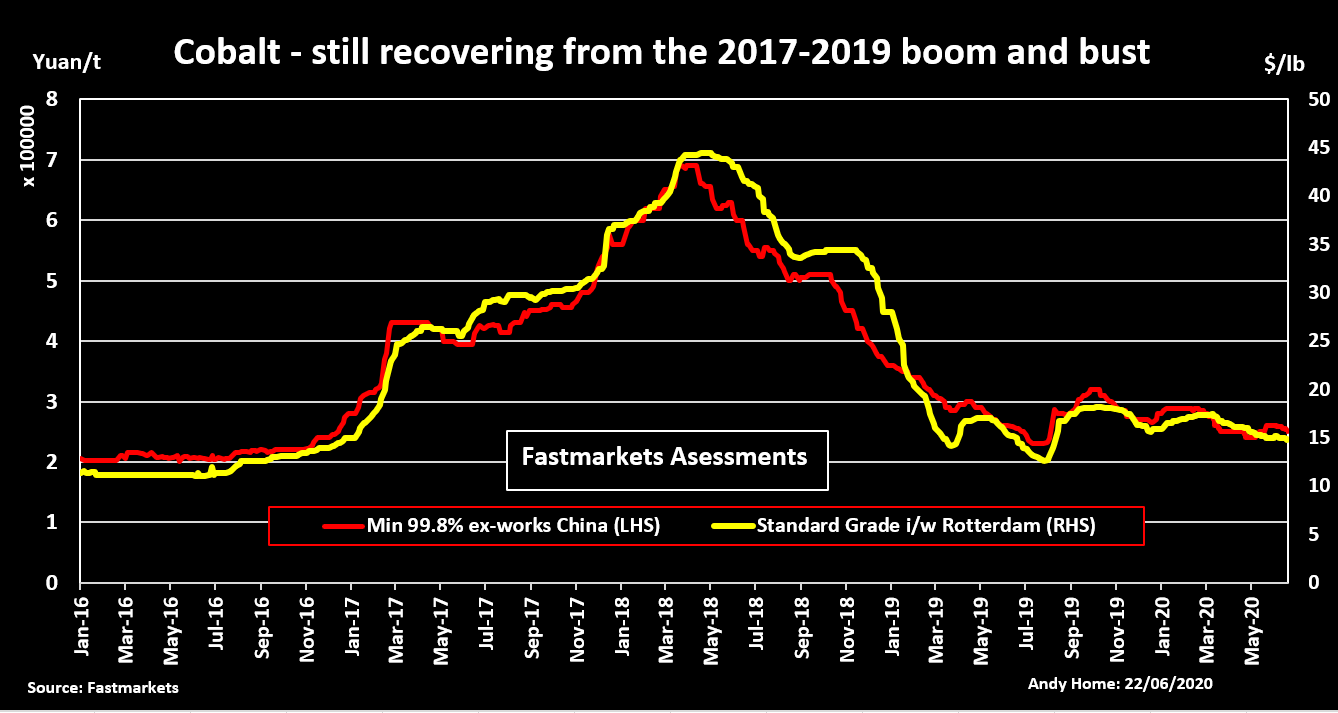

Everyone has been trying to reduce the amount of cobalt in the metallic mix. Cobalt is expensive, currently trading around $33,000 per tonne on the London Metal Exchange. It has a history of volatility both in terms of price and supply, which is dominated by production, both official-sector and artisanal, in the Congo.

The human cost of artisanal mining also weighs heavy on an industry that is driving towards a green and socially responsible future.

Tesla’s desire to shift away from cobalt usage seemed to be borne out by the revelation its new Chinese plant would use cobalt-free batteries.

Lithium-iron-phosphate (LFP) batteries have been around a long time, are cheaper than cobalt-containing batteries, but lack energy density. The biggest market is China, where they are used in vehicles that don’t need extensive range or high performance, such as municipal garbage trucks.

However, it seems that Chinese LFP battery makers such as Contemporary Amperex Technology Co Ltd (CATL) have been quietly improving the technology to the point that Tesla is now interested in using it in its Model 3 cars in China.

But it’s also clear from the Glencore deal that Tesla, however reluctantly, is going to continue using cobalt in other markets.

Tesla’s willingness to consider a range of battery types is testament that the EV revolution is going to be characterised by multiple chemistries depending on vehicle type and geographic market.

And some of them at least are going to use cobalt.

Cobalt blues

Tesla’s deal to buy 6,000 tonnes per year of cobalt from Glencore’s Congo operations is a double boost for the market, representing a long-term affirmation of demand and a short-term way of clearing excess stocks.

The cobalt market has yet to recover from the crash that followed the price boom of 2017-2018 as too much supply, particularly from the Congo’s artisanal sector, swamped demand.

Glencore last year placed its Mutanda mine in the Congo on two-year care and maintenance, while its Katanga mine was carrying stocks of almost 13,000 tonnes at the end of 2019.

Those stocks have weighed heavily on the price. Fastmarkets’ assessment of standard-grade cobalt currently sits at an 11-month low of $14.75 per kilogram ($30,250 per tonne)

However, Glencore has recently concluded a flurry of supply deals with battery-makers and now with Tesla, signalling the company “has placed a strategic focus on forward selling its built-up hydroxide stocks,” according to analysts at Roskill.

The research house estimates that Glencore has now locked in sales representing around 82% of production at Katanga. That, combined with Mutanda on care and maintenance, “significantly reduces the volumes of cobalt available in the open market”.

That may translate into an accelerated price recovery when the next EV-led demand surge happens.

It also means there’s potentially less around for everyone else. There are several new cobalt mines in the planning or development stage but the Congo and its artisanal miners are going to remain the dominant supplier for the foreseeable future.

That simple fact explains why Tesla has moved directly to ensure its own supply with the largest non-Chinese producer in the country.

Other automotive makers may well take heed.

Supply security

Tesla’s move directly to take responsibility for its cobalt supply isn’t without risk.

Glencore may be a London-listed multinational, but it’s not immune to the negative headlines that go with doing business in the Congo.

It is under intense regulatory scrutiny; the Swiss Attorney General’s Office (OAG) last week joining the list of ongoing investigations into its conduct in the country.

Last year saw the death of 43 “illegal” miners on Glencore’s Kamoto concession, a human tragedy that was compounded by the government’s decision to send in the army to forcibly clear the area.

Tesla, though, has evidently decided the risk of not getting enough future cobalt outweighs the potential reputational risks of taking supply directly from the Congo.

Such direct mine sourcing is not the norm for auto companies. They don’t, for example, directly buy the iron ore that goes into the steel they use. Or the bauxite that makes the aluminium.

But cobalt is different. There’s not much around and too much of what is around comes from the Congo.

The EV revolution may have been stalled by covid-19, but the build-out of battery manufacturing capacity has continued uninterrupted.

And with the European Union in particular focusing its industrial stimulus package on “green” technology, the next EV wave may already be building.

Tesla’s reluctant commitment to cobalt is a warning sign for other automakers they may have to do the same if they want to be sure they’ve got enough of the stuff to meet that coming demand surge.

(Editing by Mark Potter)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments