The future of uranium: A story of supply and demand

The Future of Uranium: A Story of Supply and Demand

The uranium market is at a tipping point.

Since the Fukushima accident in 2011, uranium prices have been on a downtrend, forcing several miners to suspend or scale back operations. But nuclear’s growing role in the clean energy transition, in addition to a supply shortfall, could turn the tide for the uranium industry.

The above infographic from Standard Uranium outlines how uranium’s demand and supply fundamentals stack up, and how that balance could change the direction of the market in the future.

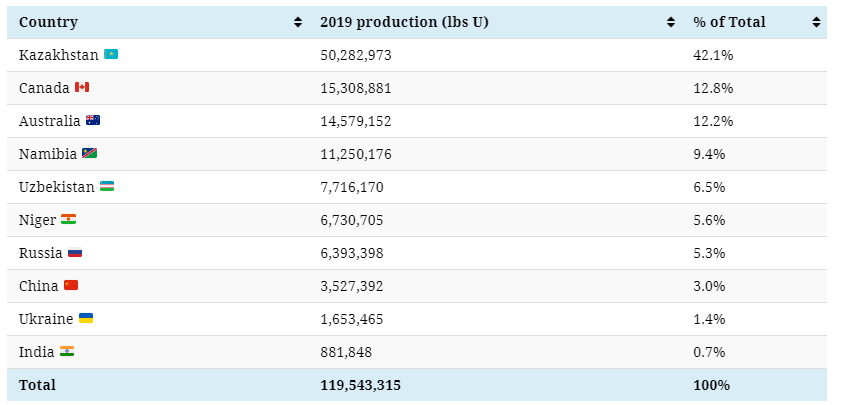

The Uranium Supply Chain

The supply of uranium primarily comes from mines around the world, in addition to secondary sources like commercial stockpiles and military stockpiles.

Although uranium is relatively abundant in the Earth’s crust, not all uranium deposits are economically recoverable. While some countries have uranium resources that can be mined profitably when prices are low, others do not.

For example, Kazakhstan hosts roughly 1.2 billion lbs of identified recoverable uranium resources extractable at less than $18 per lb, more than any other country. On the contrary, Australia hosts a larger resource of uranium but with a higher cost of extraction. This varying availability of resources affects how much uranium these countries produce.

It’s not surprising that Kazakhstan is the largest producer of uranium given its vast wealth of low-cost resources. In 2019, Kazakhstan produced more uranium than the second, third, and fourth-largest producers combined.

Canada produced around one-third of Kazakhstan’s production despite the suspension of the McArthur River Mine, the world’s largest uranium mine, in 2018. Australia was the world’s third-largest producer with just two operating uranium mines.

However, production figures do not tell the entire story, and it’s important to look at how the market price of uranium impacts supply.

How Uranium Prices Affect Supply

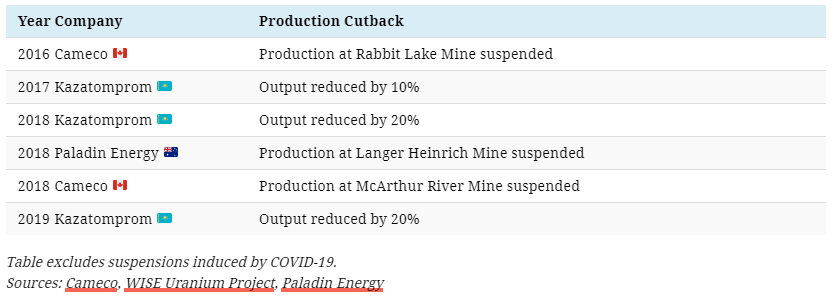

Low uranium prices have had a twofold effect on uranium supply over the last decade.

Firstly, miners have cut back on production due to the weakness in prices, reducing the primary supply of uranium. Here are some production cutbacks from major uranium mining companies:

In addition, low prices have also blocked new supplies from entering the market. Around 46% of the world’s identified uranium resources, 8 million tonnes, have an extraction cost higher than $59 per lb. However, uranium prices have hovered close to $30 per lb since 2011, making these resources uneconomic.

As a result, the supply of uranium has been tightening, and in 2020, mine production of uranium covered only 74% of global reactor requirements.

Going Nuclear: The Future of Uranium

The world is moving towards a cleaner energy future, and nuclear power could play a key role in this transition.

Nuclear power is not only carbon-free, it’s also one of the most reliable and safe sources of energy. Countries around the world are beginning to recognize these advantages, including Japan, where all 55 reactors were previously taken offline following the Fukushima accident.

With more than 54 reactors under construction and 100 reactors planned worldwide, the demand for uranium is set to grow. Unlocking new and existing supplies is critical to meeting this rising demand, and new uranium discoveries will be increasingly valuable in balancing the market.

Standard Uranium is working to discover uranium with five projects in the Athabasca Basin, Saskatchewan, Canada, home of the world’s highest-grade uranium deposits.

(This article first appeared in the Visual Capitalist Elements)

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments