Copper price is going nowhere

Credit ratings agency Moody’s warned at the beginning of the year that the current downturn in raw materials was like no other and that defaults among mining and metals companies could reach levels last seen during the height of the financial crisis.

As a result, Moody’s embarked on a sector-wide review of the 87 global mining majors that it covers. The review started off with a bang in January when the agency dropped the world’s biggest listed copper mining company Freeport-McMoRan deep into junk territory. By the end of the first quarter 30 companies had their debt ratings axed including marquee names like Rio Tinto, BHP Billiton and Chile’s state-owned Codelco. The likes of Anglo American and Vale also lost their investment grade rating for the first time.

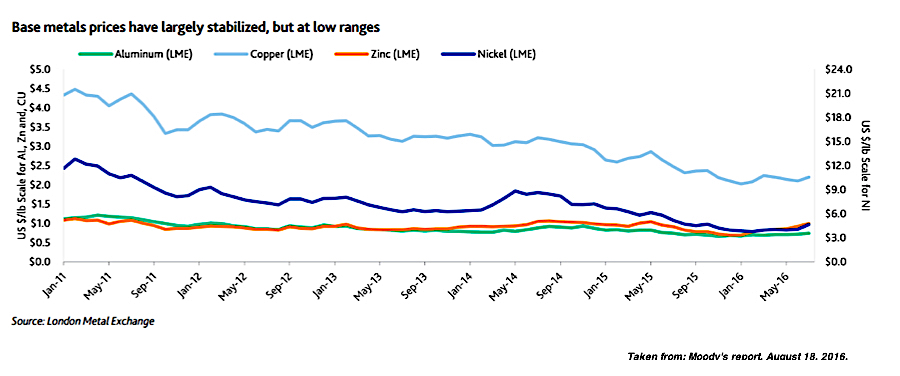

Today, Moody’s issued a new report on the global base metal sector, changing its outlook from negative to stable. Clearly, the New York-based firm is not heralding a new bull market for miners, but after its stark warnings at the beginning of the year, stable is more than welcome.

“Challenging industry conditions should continue through at least 2018 until the industry can recalibrate the supply levels to match demand”

Moody’s says its assessment reflects the expectation that prices for aluminum, copper, nickel and zinc are unlikely to deteriorate further over the next 12-18 months, but Carol Cowan, a Moody’s Senior Vice President and the author of the report added a warning:

“That being said, challenging industry conditions should continue through at least 2018 until the industry can recalibrate the supply levels to match demand.”

The major driver of the recent price stabilization and positive investor sentiment towards base metals are growth expectations from China says Cowan: “Stimulus measures from the government including easing of credit, reducing reserve requirements and increasing infrastructure spending have helped offset the country’s decelerating GDP trajectory.”

Moody’s recently revised upwards expectations for Chinese GDP expansion to 6.6% and 6.3% in 2016 and 2017 respectively from 6.3% and 6.1% before, but says downside risk for the world’s number two economy remains.

Apart from a stumble in China or a deterioration in US and European manufacturing sabotaging the recovery, fundamentals in the base metals sector are also limiting any meaningful upside for the industry. All base metals, with the exception of zinc, will remain oversupplied for some time and exchange inventories have also remained stubbornly elevated (again zinc is the exception) according to the report.

This is especially true for industry bellwether copper – the market is set stay in surplus despite some curtailment by Freeport and Glencore as new production enters the market.

Base metals companies and those with exposure to the sector are likely to see earnings fall again year-on-year

Additional supply includes increased production from Freeport’s Cerro Verde mine and the ramp-up of the Chinese-backed Las Bambas mine in Peru, increased output at Vale’d Salobo mine and the

ramping up of Southern Copper Corp’s Buenavista mine in Mexico. Canada’s First Quantum Minerals also continues to proceed with the development of the Cobre Panama project, with full production expected in 2018, while BHP Billiton this week announced increased guidance at Escondida, the world’s largest copper mine by some margin.

Only 19 organizations retain investment grade ratings in the sector although Moody’s has more recently changed a number of companies’ outlook to positive, notably Anglo American thanks to its asset sales. But don’t expect the better operating environment to show up in base metal miners’ financials just yet says Moody’s:

The modest improvement in base metal prices and cost benefits from low oil prices and currency depreciation against the dollar will soften earnings degradation in 2016, yet base metals companies and those with exposure to the sector are likely to see earnings fall again year-on-year.

Moody’s has adjusted the price sensitivities by which it measures mining companies’ operating performance over the medium term and the agency now sees copper bottoming at $2.00 a pound to trade in a range of $2.15 – $2.35 ($4,740–$5,180) through 2018, in line with recent price bands.

Moody’s see nickel at between $4.20 and $5.00 a pound ($9,250–$11,000 a tonne), aluminum at $0.70-$0.75 ($1,540–$1,650) and zinc at $0.80–$90 ($1,765–$1,985), which is below the spot price despite the fact that the metal enjoys the best fundamentals of all base metals.

Looks pretty flat

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments