Why doesn’t gold get the respect it deserves?

A longstanding curiosity in the investment business has been the disinterest in precious metals among institutional investors. Whether from the handful of consultants now leading the institutional space, or directly from the stewards of our nation’s pension, endowment, and family-office wealth, skepticism over gold’s portfolio relevance remains fairly pervasive. Because investment professionals are generally well informed, competing in an industry in which performance is king, one would assume any asset class deserving of rightful consideration would enjoy a fair hearing.

In this report, we present a collection of empirical evidence we view as compelling support of gold’s productive role as a portfolio-diversifying asset.

Gold Has Generated Consistently Positive Returns in This Millennium

Eight years of zero interest-rate policy (ZIRP) have compressed returns across a wide spectrum of institutional investment regimens. Especially in the pension and endowment world, few portfolios are achieving chartered rates of return. In this environment, we find it puzzling that institutional investors still choose to ignore gold’s market-leading returns. As shown in Figure 1, gold has generated positive annual returns in 14 of the past 17 years. What is even more impressive is gold’s performance compared to the S&P 500 Index, the benchmark for broad U.S. equity performance. Gold’s compound annual

growth rate (CAGR) for the 16.75 years (2001 to 9/30/17) stands at 9.68% versus 6.01% for the S&P 500 Index (dividends reinvested). Indeed, it is fair to say that since the turn of the millennium, any long-term allocation to gold would have improved total returns for the vast majority of pension and endowment portfolios.

What is it about gold’s performance that is so difficult to embrace?

Figure 1: Annual Returns of Gold Versus S&P 500 Index Since 2001 (2001 to 9/30/17)

Source: Bloomberg; S&P 500 Index returns reflect reinvested dividends.

To us, the most interesting aspect of gold’s dogged performance since the beginning of 2001 has been the wide variety of financial, monetary and asset-market conditions that have prevailed during the various years in which gold has advanced. Along the way, every popular variable to which some portion of consensus attributes strong gold correlation has oscillated repeatedly, yet gold has advanced in the overwhelming majority of these years.

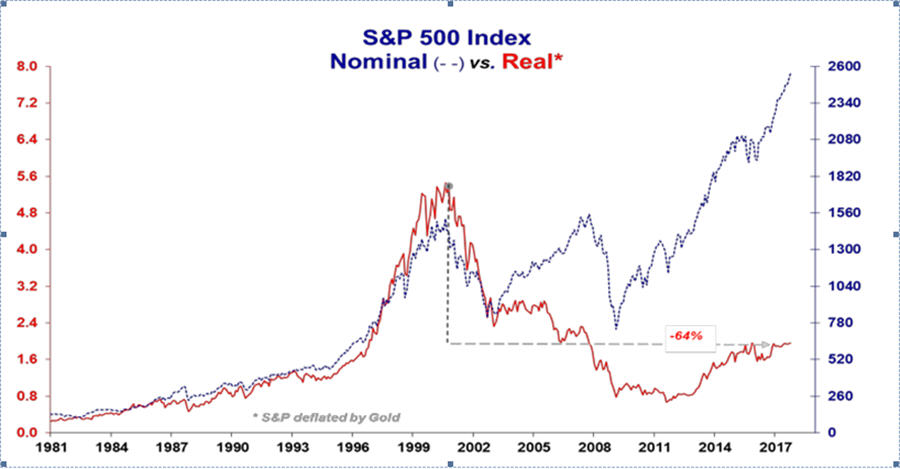

Gold Has Provided Strong Protection of Real Purchasing Power

Now that the S&P 500 Index has almost quadrupled from its 3/06/09 low (666.79), few plan sponsors would equate gold’s potential portfolio “alpha” with that available among U.S. equities. However, as shown in Figure 2, the S&P 500, measured

in gold terms, remains 64% lower today than at its 2000 peak! During the past two corrections in the S&P 500, during which the Index declined 50.50% (2000-2002) and 57.7% (2007-2009), gold provided unrivaled protection of real purchasing power. We are aware of no reasoning to suggest gold’s portfolio-protection benefits will prove any less potent during the next correction in U.S. equities. In fact, the slopes of the lines in Figure 2 suggest gold’s portfolio-insurance value has rarely been more compelling.

Figure 2: S&P 500 Index Performance Since 1981 (Nominal and Deflated by Gold Price)

Source: MacroMavens

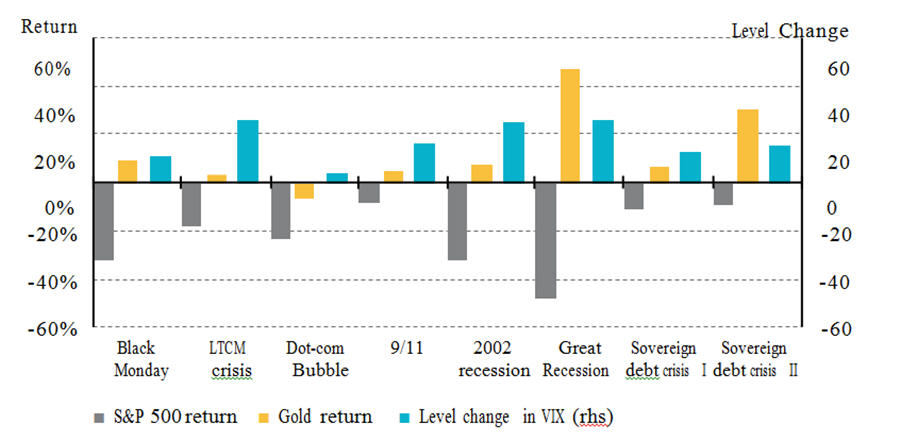

Gold Has a Proven Track Record as a Safe-Haven Asset

In documenting an objective record of gold’s portfolio utility, one logically begins with gold’s traditional profile as a safe- haven asset. It goes without saying that gold’s safe-haven reputation accrues from bullion’s established history of relative outperformance during periods of financial stress. As shown in Figure 3, gold has done a masterful job of insulating portfolio capital from sharp declines in U.S. equities during the past three decades of financial crises.

Figure 3: Percentage Changes for S&P 500 Index and Spot Gold (lhs) Versus Absolute Change in VIX Index Level

(rhs) During “Crisis” Periods (1987-Present)

Source: World Gold Council

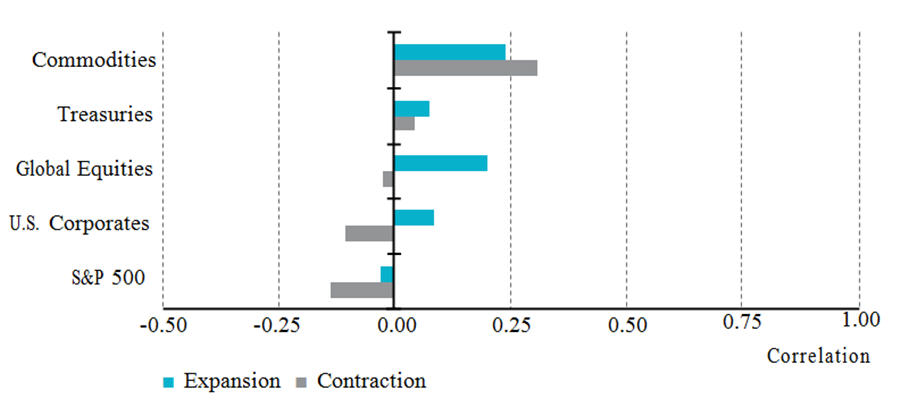

Gold Has Low Correlation to Traditional Asset Classes

As the investment advisory business has become more scientific, amid increasingly frequent financial shocks, the holy grail of portfolio allocation has become the overarching search for non-correlating assets. Methodologies for identifying and measuring non-correlating assets are in no short supply. However, a routine calculation employed by contemporary risk managers is stress-testing portfolio components under simulated conditions of both positive and negative economic trends.

As shown in Figure 4, gold’s correlation to traditional asset classes remains uniquely low during periods of both economic expansion and contraction. In other words, gold’s portfolio-diversification benefits are not solely dependent on bad news.

Figure 4: Correlation of Spot Gold to Traditional Financial Assets During U.S. Economic Expansions & Contractions (1987-Present)

Source: World Gold Council

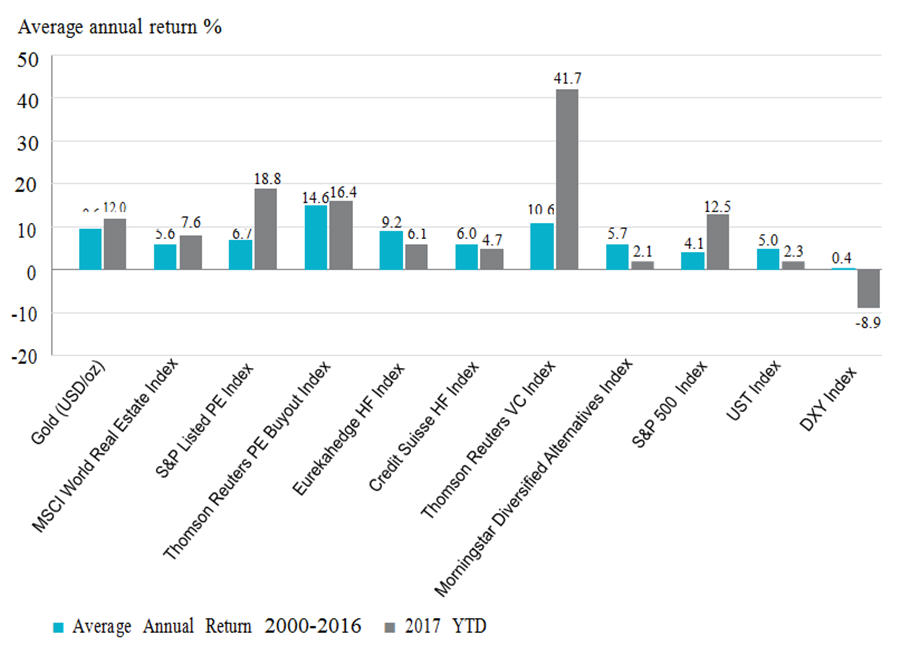

Institutional focus on non-correlating assets has directed trillions of dollars of investment capital towards hedge funds and specialized investment partnerships in disciplines such as real estate, private equity and venture capital. A more recent trend, however, has been mounting investor backlash against elevated fees charged by alternative managers in the context of mediocre investment returns (not to mention onerous liquidity and lockup provisions). In short, a marquee consideration for today’s pension and endowment stewards has become whether the added fees of alternative investments are truly worth it.

Gold Holds Its Own Against Alternatives

Recognizing there will always be outlying homeruns in the ultra-competitive partnership space, it is instructive to compare the performance of gold bullion directly against the performance of prominent indices of alternative-investment vehicles. As documented in Figure 5, gold bullion has more than held its own against returns of high-profile alternative- investment indices, both during the recent past (year-to-date 2017), as well as over the long run (2000-2016).

Figure 5: Average Annual Returns for Spot Gold Versus Selected Alternative Asset Indices

(2000-2016 and 2017 YTD through 9/30/17)

Source: World Gold Council

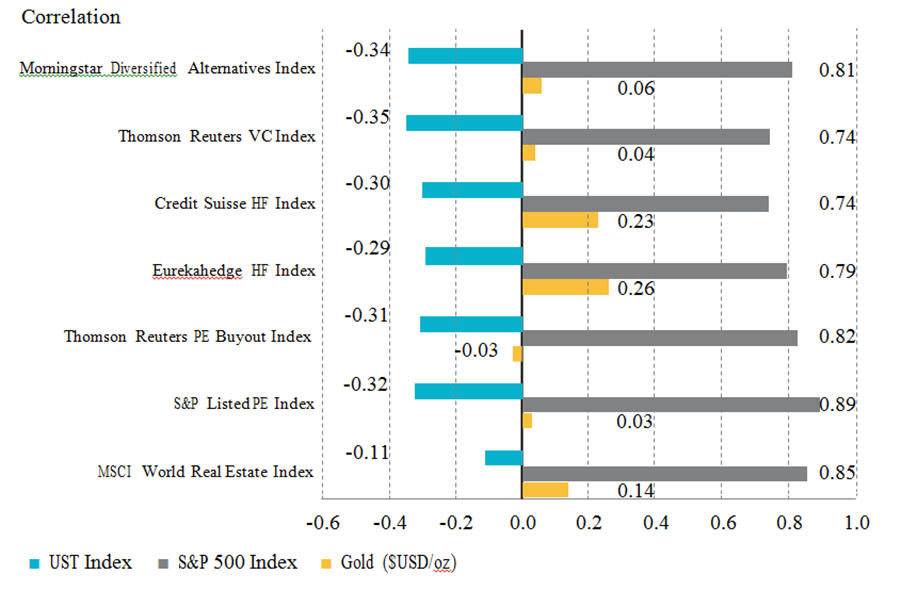

Even more challenging to industry status quo, gold bullion has rivaled the performance of alternative asset indices while simultaneously displaying far lower correlation to these vehicles than either stocks or bonds. As shown in Figure 6, the correlation between prominent alternative asset indices and the S&P 500 Index has averaged 81% over the decade through 9/30/17. By way of comparison, the 10-year correlation between these same indices and spot gold has averaged just 10%.

At an 81% correlation-rate with U.S. equities, are high-priced and unwieldy alternative vehicles worth their freight? What are we missing?

Figure 6: Correlations Between Alternative Asset Indices and S&P 500 Index, U.S. Treasuries and Spot Gold

(Trailing 10-years Monthly Data through 9/30/17)

Source: World Gold Council

Choosing the Right Portfolio Allocation to Gold

Now a highly operative question might be, “Is there a reliable method for investors and institutions to right-size a portfolio commitment to gold?” Given the variables involved, there can never be a single, definitive solution to any portfolio-construction challenge. For a quick answer on the fly, we offer that a 2-10% allocation can make sense in most portfolios.

But let’s dig deep and get a more technical answer. Historically, asset-allocators have favored classical “mean variance optimization” techniques to quantify appropriate portfolio weightings among selected “input” assets to maximize projected portfolio returns within predetermined ranges of risk tolerance. The shortcoming of mean-variance calculations is that they massage historical price trends to calculate (a geometric average and standard deviation for) a likely efficient frontier between future returns and future volatility.

Tapping into the contemporary investment trend of sophisticated quantitative analysis, we cite the considered work of Richard and Robert Michaud (New Frontier Advisors) in developing their “resampled efficiency optimization” approach to portfolio allocation. While resampled efficiency (RE) optimization still recognizes there is some information about future returns and covariance in historical performance, the method of portfolio optimization assumes there are no “fixed known parameters,” and that there will always be a degree of variability in future outcomes. The essence of RE optimization is to establish a portfolio allocation most likely to maximize returns for every unit of undertaken portfolio risk (the “information ratio”) amid any combination of future financial and market conditions.

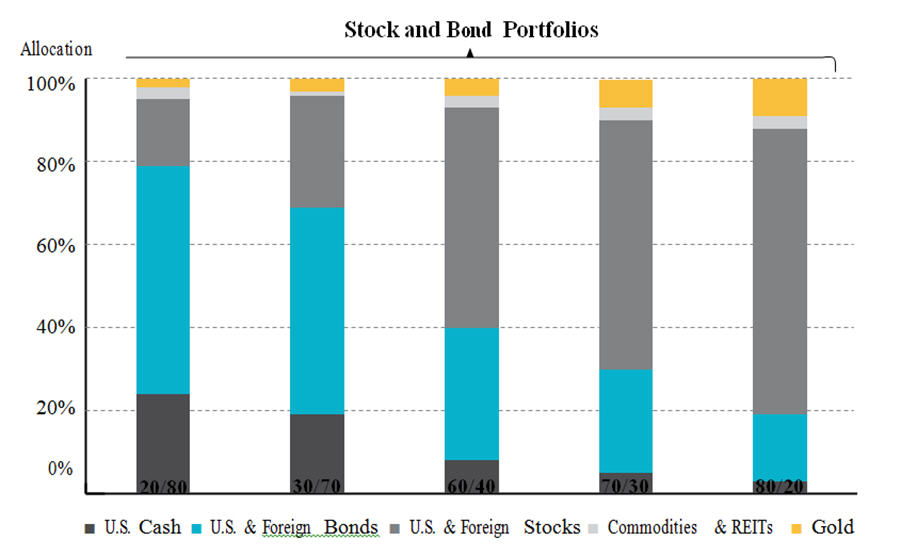

In Figure 7, we present RE optimization outcomes for five different portfolios of traditional assets, each with unique risk- tolerance assumptions. For example, the most conservative portfolio mandates a 20% weighting in stocks (and other assets) versus an 80% weighting for cash and bonds. The most aggressive portfolio mandates an 80% weighting in stocks versus a

20% weighting for cash and bonds. The five asset inputs utilized in this exercise are cash, stocks, bonds, commodities/REITs, and gold. RE optimization suggests a gold allocation between 2% and 9% will maximize risk-adjusted returns across the spectrum of risk tolerances. Broadly speaking, the higher the risk in the portfolio, whether in terms of volatility, illiquidity or concentration, the larger will be the modeled gold allocation to offset that risk.

Figure 7: Optimal Gold Weightings in Basic Stock/Bond Portfolios at Five Risk Tolerance Levels

Source: Based on Michaud&Michaud RE Optimization; World Gold Council

It is one thing to establish that an allocation to gold can augment risk-adjusted returns among basic portfolio building blocks such as stocks and bonds. In the contemporary institutional world, however, so much brainpower and so many resources are directed at synthesizing complex investment strategies, it is difficult for participants to recognize that gold’s passive and seemingly anachronistic profile adds considerable value to modern portfolio dynamics. For example, despite the fact that insitutions are

laser-focused on noncorrelating assets, we believe industry due diligence generally gravitates to alternative vehicles with the highest nominal returns in each product category. In the process, gold’s unrivaled powers of non-correlation are shortchanged.

It is gold’s lack of correlation to all other portfolio assets, as opposed strictly to bullion’s nominal return patterns, which empowers gold’s unique ability to protect against portfolio drawdowns. As we have long maintained, when paper assets perform as advertised, gold’s portfolio utility recedes to average profile. However, when paper ceases to perform as advertised, such as during stress tests like 2008, no alternative asset can match gold’s non-correlating, portfolio-protection power.

Gold Offers Attractive Protection and Improves Risk-Adjusted Returns

As precious-metal investors, we are familiar with the philosophical hurdles confronting gold in institutional circles. Gold is often perceived as a catastrophe asset, and a common line of reasoning suggests no endowment could weight gold sufficiently to insulate an investment corpus from actual catastrophe, so why introduce the distraction? Pension and endowment trustees routinely sidestep the precious-metal debate with the simple observation, “Gold is not what we do.” Finally, many investment advisors and consultants, especially in a late-stage equity bull market, fear a portfolio allocation to gold might be misinterpreted by clients as a signal that “something is wrong.”

On the other hand, to many investors, gold offers attractive protection from financial assets when their quoted prices are perceived as detached from intrinsic value, or, even more importantly, when the integrity of the unit of account in which these prices are quoted (fiat currencies) becomes increasingly suspect. By way of example, some of the world’s most sophisticated investors, including Soros, Druckenmiller, Klarman and Singer, employ gold liberally to navigate fluid market conditions. To these heavyweight investors, gold offers the ability to remove, at a moment’s notice, virtually unlimited amounts of portfolio

capital from the vagaries of overpriced markets or questionable central bank policies. In our experience, the logic of a portfolio allocation to gold is most easily understood by owners of accumulated wealth. Those who have created significant capital are highly sensitive to potential risks of its dissipation, even amid the intoxication of fresh weekly highs for the S&P 500.

Somewhere in the middle rest gold’s true investment merits. In this report, we have presented evidence that a portfolio allocation to gold can improve risk-adjusted returns in portfolios of any risk tolerance. Gold’s long-term returns have rivaled the performance of sophisticated alternative-asset indices, with far lower correlations to traditional asset classes, and without burdensome fee and liquidity frictions. The empirical data suggest a modest gold allocation provides tangible portfolio- diversification benefits in any investment climate. Given the unprecedented monetary, financial and asset-valuation risks now confronting investors, gold’s potent benefit of purchasing-power-protection, which essentially accrues for free, seems to us an incredibly precious commodity.

Authored by Trey Reik, Senior Portfolio Manager, Sprott Asset Management USA, Inc.

Figure 3: VIX Index data is available only after January 1990. For event occurring prior to that date, annualized 30-day S&P 500 volatility is used as a proxy. Dates used: Black Monday: 9/1987-11/1987; LTCM: 8/1998; Dot-com: 3/2000-3/2001; September 11: 9/2001; 2002 recession: 3/2002-7/2002; Great recession: 10/2007-2/2009; Sovereign debt crisis I: 1/2010-6/2010; Sovereign Debt Crisis II: 2/2011-10/2011.

Figure 4: From January 1987 to September 2017. Based on weekly returns of the S&P 500, MSCI ACWI ex-U.S., JPMorgan U.S. Treasury Index, Bloomberg Barclays Corporate Bond Index, S&P Goldman Sachs Commodity Index, and LBMA pm fix. Business cycles defined by National Bureau of Economic Research (NBER). Data for U.S. Corporates starts December 1988 due to data availability.

Figure 5: All figures as of September 30, 2017. UST Index is Barclays U.S. Treasuries Unhedged Total Return Index.

Figure 6: All figures as of September 30, 2017. UST Index is Barclays U.S. Treasuries Unhedged Total Return Index.

Figure 7: Resampled efficiency utilized to maximize returns for each unit of portfolio risk under two scenarios. The “aggressive” portfolio simulates standard allocations of 55 percent equities, 25 percent fixed income, and 0 percent to 5 percent cash, with the remaining 15 percent-20 percent optimally distributed among alternative assets. The “conservative” portfolio simulates allocations of 30 percent equities, 50 percent fixed income, 0 percent to 10 percent cash, with the remaining 10 percent-20 percent distributed optimally among alternative assets.

The risks associated with investing in a Trust depend on the securities and assets in which the Trust invests, based upon the Trust’s particular objectives. There is no assurance that any Trust will achieve its investment objective, and its net asset value, yield and investment return will fluctuate from time to time with market conditions. There is no guarantee that the full amount of your original investment in a Trust will be returned to you. The Trusts are not insured by the Canada Deposit Insurance Corporation or any other government deposit insurer. Please read a Trust’s prospectus before investing. The information contained herein does not constitute an offer or solicitation to anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not resident in Canada should contact their financial advisor to determine whether securities of the Funds may be lawfully sold in their jurisdiction. The information provided is general in nature and is provided with the understanding that it may not be relied upon as, nor considered to be, the rendering or tax, legal, accounting or professional advice. Readers should consult with their own accountants and/or lawyers for advice on the specific circumstances before taking any action. Sprott Asset Management LP is the investment manager to the Sprott Physical Bullion Trusts (the “Trusts”). Important information about the Trusts, including the investment objectives and strategies, purchase options, applicable management fees, and expenses, is contained in the prospectus. Please read the document carefully before investing. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated. This communication does not constitute an offer to sell or solicitation to purchase securities of the Trusts. This article may not be reproduced in any form, or referred to in any other publication, without acknowledgement that it was produced by Sprott Asset Management LP and a reference to www.sprott.com. The opinions, estimates and projections (“information”) contained within this report are solely those of Sprott Asset Management LP (“SAM LP”) and are subject to change without notice. SAM LP makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, SAM LP assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. SAM LP is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Sprott Asset Management LP. These views are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. SAM LP and/or its affiliates may collectively beneficially own/control 1 percent or more of any class of the equity securities of the issuers mentioned in this report. SAM LP and/or its affiliates may hold short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, SAM LP and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

More News

Chile’s Novandino Litio seeks environmental approval for $3B Atacama lithium project

July 03, 2026 | 11:29 am

LME approves Adani’s major copper smelter in India as listed brand

July 03, 2026 | 09:33 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments