Tinka Resources: Ayawilca could grow into a world-class zinc asset

Ayawilca Project, Drilling Location

1. Introduction

When a zinc junior manages to hit 63.9m @ 5.6% Zn and 51.9m @ 10.1% Zn in the very first stepout drill hole of a new exploration program, you know they could be on to something very special. Until then, the markets were largely unaware of Tinka Resources Ltd. (TK:TSX.V; TKRFF:OTCPK) and its Ayawilca zinc project in Peru, but this changed very quickly after this, and other intercepts. They were even one of the hottest exploration stories at this year’s PDAC.

After doing my due diligence, talking to management, comparing the company with peers, and calculating different scenarios, it appears to me that Tinka could become one of the best zinc juniors around, and the strong drill results so far seem to be underlining my opinion.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

The views, opinions, estimates or forecasts regarding Tinka’s performance are those of the author alone and do not represent opinions, forecasts or predictions of Tinka or Tinka’s management. Tinka has not in any way endorsed the information, conclusions or recommendations provided by the author.

2. Company

Tinka Resources Ltd. is a junior exploration company based in Vancouver, Canada, that is developing its 100%-owned Ayawilca zinc project.

The project is located in the richly mineralized silver-lead-zinc belt of Central Peru, in hilly/moderately mountainous terrain. Peru was named the most attractive jurisdiction in Latin America in the last Fraser Survey of Mining Companies, ranked #28 out of 104, surpassing Chile (#39).

Ayawilca; location map

Tinka has one of the few significant grass-roots zinc discoveries anywhere in the world in the last decade. Since the chance first discovery of zinc back in 2013 at its Ayawilca project in Peru, Tinka has now outlined a substantial zinc resource containing 2.45 billion pounds Zn, which is likely to grow as current drilling progresses. Under new management since 2014, the company has shifted gears and right on time it seems, with a zinc supply/demand deficit driving up zinc prices. A very important drill permit was issued in February 2017, enabling Tinka to drill several large prospective targets that were previously out of reach. The first drill program of 2017 is well underway now, delivering excellent results so far.

The company is managed by members of a talented, experienced and modest group of Australian executives, most of them very knowledgeable geologists. Tinka is headed by President and CEO Graham Carman, who has a PhD to his name. Carman has extensive experience in Peru and more in particular with zinc-led projects, as he worked for the likes of Rio Tinto and Pasminco in Peru, and assessed, discovered and advanced significant deposits over there.

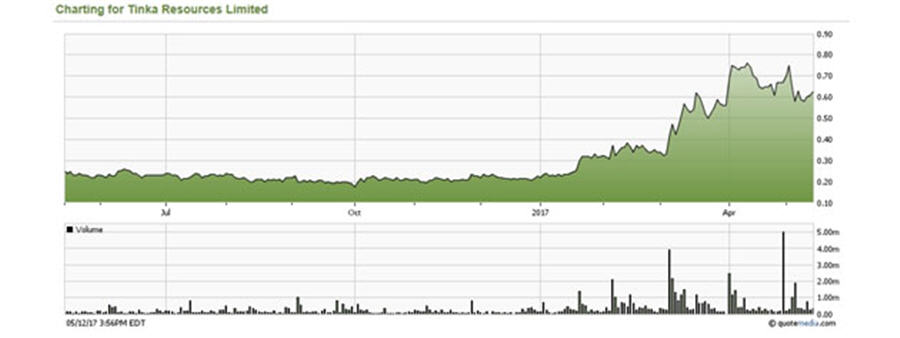

Some basic information on share structure and financials: Tinka Resources has 208M shares outstanding. The fully diluted share count stands at 248.8M shares, as there are 14.4M options, 0.5M shares reserved, and 27.2M warrants (all comfortably in the money: 12.6M @ CA$0.30 expiring Nov 2017, 12.6M @ CA$0.45 expiring May 2020). The cash position is estimated at CA$10M, with no debt. The current share price is CA$0.63, resulting in a current and fully diluted market cap of CA$156.7M (as all warrants are well in the money).

The stock sold off on the latest drill results, which weren’t as stellar as the big intercept mentioned earlier, but were according to my expectations as I will explain later on, and didn’t have much implications for exploration upside as I see it, so I view this dip as an excellent buying opportunity.

Management has decent skin in the game as it holds 3%, and major shareholders are the Sentient Group with 25% (since its latest transaction on April 28, 2017) and the International Finance Corp (IFC, part of the World Bank) with 8.7% (it sold off 5.3% recently, presumably to allow room to exercise its large warrant position and at an opportune time, see also the 5M shares block trade in the chart at the end of April). JP Morgan Asset Management has 7.3%, and other institutions hold about 10%. So at least 50% of the stock is tightly held by long-term institutional shareholders.

3. Zinc

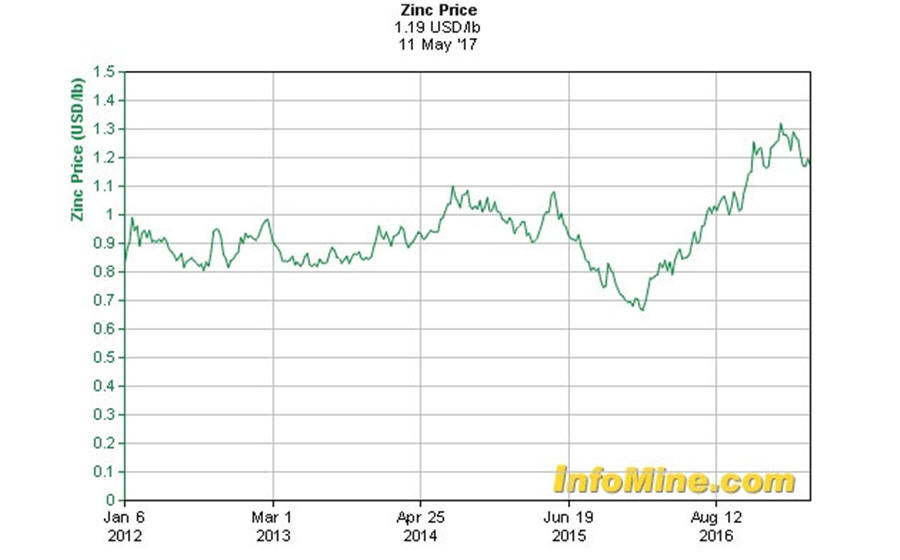

The primary metal for Tinka Resources is zinc. A chronic shortage of supply of zinc is being forecasted. The coincidental closure of major zinc mines (Brunswick, Perseverance, Century, Lisheen, Skorpion) through depletion, taking 500kt per annum off the table, and this, coupled with a very limited number of new zinc mines in the near-term development pipeline set to come on-line, is expected to lead to a robust zinc price for the next few years. The price of zinc already ran up from US$0.67 to US$1.32/lb, is forecasted to go to US$1.50/lb levels, and has been correcting lately on a bit of cooling down of global demand, which is believed to be temporary regarding the structural issues for zinc supply. This is a healthy and much needed break by the way, in my view, after doubling in 1.5 years:

Latest input on zinc fundamentals indicate a decline in Chinese inventories, and LME warehouse levelsto multiyear lows, so the current zinc price might prove to be a support level for a possible next leg up. This story on Kitco.com seems to confirm this, and would reinforce the strength of the ongoing zinc deficit thesis.

The zinc market has been in deficit for a long time (since 2012), but only since the end of 2015 did the zinc price start to appreciate, probably due to covert stockpiles that finally seem to be depleted. So, despite the current modest correction, the long-term zinc case looks pretty convincing in my view, and playing into the hands of Tinka Resources.

That’s it for zinc fundamentals, let’s continue with Tinka’s flagship project, Ayawilca.

4. Project

The Ayawilca property is located 200km northeast of Lima in the Department of Pasco, Central Peru, at altitudes of between 3,800 and 4,300 metres. The property is 40km northwest of the world-class Cerro de Pasco zinc-lead-silver mine, and 100km south of the giant copper-zinc Antamina mine. It is no coincidence that infrastructure is not an issue, for example a powerline runs right across the Ayawilca property. A lot of large miners are surrounding Ayawilca, which is never a bad thing when looking for a buyout. Another interesting thing is that the Cajamarquilla smelter (La Oroya is on care and maintenance for now) handles indium, which opens up the possibility for by-product credits, as Ayawilca has high-grade indium. Nearby city Cerro de Pasco is the regional capital and an important mining centre with approximately 50,000 inhabitants, so local labor isn’t a problem either.

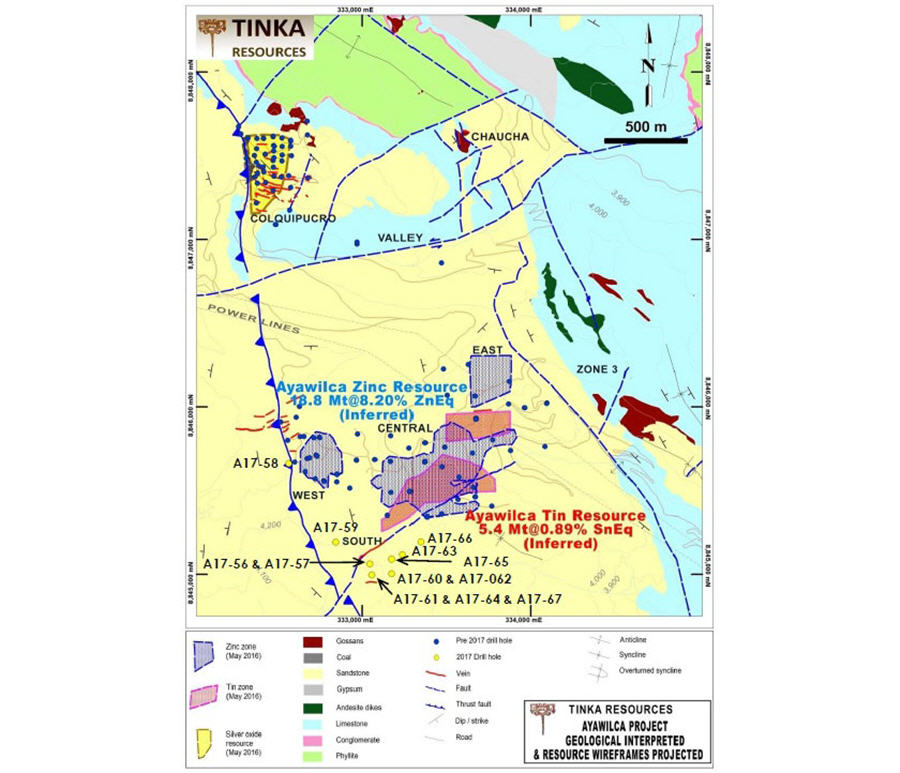

The Ayawilca project consists of three different mineralized zones, the Zinc Zone, the Tin Zone and Colquipucro (silver):

Ayawilca Project; mineralized zones

All three zones have NI43-101 compliant resource estimates being completed on them. The Zinc Zone has an Inferred Mineral Resource (May 25 2016) of 18.8Mt at 8.2 % ZnEq (5.9 % zinc, 74 g/t indium, 15 g/t silver, 0.2 % lead) containing 2.4B lbs of zinc, 1,385t of indium, 8.8M oz of silver, and 82M lbs of lead. All zinc mineralization is sulphide. The Tin Zone has an Inferred Mineral Resource (May 25 2016) of 5.4Mt @ 0.89 % Tin Equivalent (0.76 % tin, 0.31 % copper, 18 g/t silver) containing 90M lbs of tin, 37M lbs of copper, and 3.1M oz of silver. The Colquipucro Silver Zone has a Mineral Resource (February 26 2015) of 7.4 Mt at 60 g/t silver for 14.3 Moz silver (Indicated) and 8.5 Mt at 48 g/t silver for 13.2 Moz silver (Inferred) as silver oxide, but seemingly uneconomic for now at current silver prices although the deposit is heap leachable (my back of the envelope estimate would be a needed $20/oz Ag in order to be economic).

After this quick description, let’s focus on the main story, which is the exploration potential of Ayawilca.

5. The 2017 exploration program

After receiving the long-awaited drill permits for a three times larger exploration area in February this year, Tinka wasted no time and started drilling the same month. The company raised CA$11M at the end of 2016, and expects to see proceedings of numerous warrants and options during this year, providing enough cash to complete all drilling necessary for this year, an updated resource estimate and possibly a PEA, depending on drill results.

The geologists determined their targets based on three surface exploration methods: gravity-magnetics, geology-structure, and soil sampling, to increase their chances of success. Zinc mineralization at Ayawilca is ‘blind,’ lying beneath 100 to 200 metres of sandstone cover.

Magnetics seem to indicate a 3-km long southwest to northeast trend, and justifying the current stepout drilling in the Ayawilca South area:

Ayawilca; magnetic anomaly in red

On a side note about this surface exploration: personally, I’m very intrigued by the huge gravity anomalies north and just south of the recently permitted area (see NI43-101 report figure 9-2 on p. 9-7), and if the company ever plans to apply for permits there things could get even more interesting.

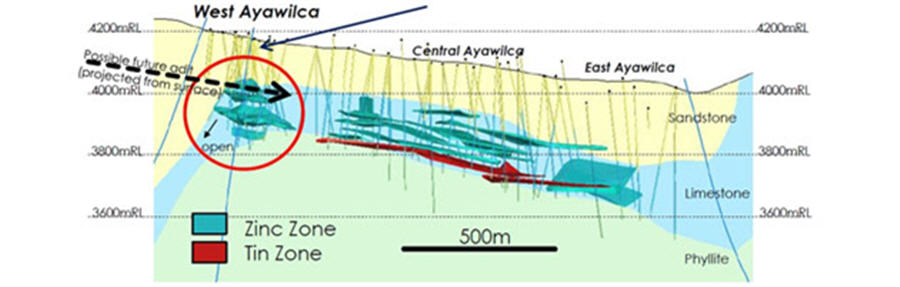

The Ayawilca Zinc and Tin Zones are hosted within a brecciated limestone unit approximately 200m thick belonging to the Pucará Group that hosts other zinc deposits in the belt including Cerro de Pasco and Morococha. The Zinc Zone mineralization is in the form of multiple, gently dipping lenses, or “mantos,” within three structural areas (West, Central, and East). This mineralization is sulphide hosted and there is no oxide component, which is important (and positive) for zinc economics.

Ayawilca project mineralized zones; long section

Almost all of the zinc mineralization is contained in the limestone, with minor mineralization in the overlying sandstone. At West Ayawilca, mineralization occurs in vertical pipe (or “chimney”), and in the easterly direction at Zone 3, the limestone crops out:

Ayawilca project resources and targets; schematic cross section

One could think that the “chimney” like structure could function as a feeder system for the limestone mineralization, but this has to be tested first of course. The light blue areas indicate the limestone coming to the surface, and clearly show why Zone 3 could be a very interesting target, based on the other promising geophysical and geochemical data.

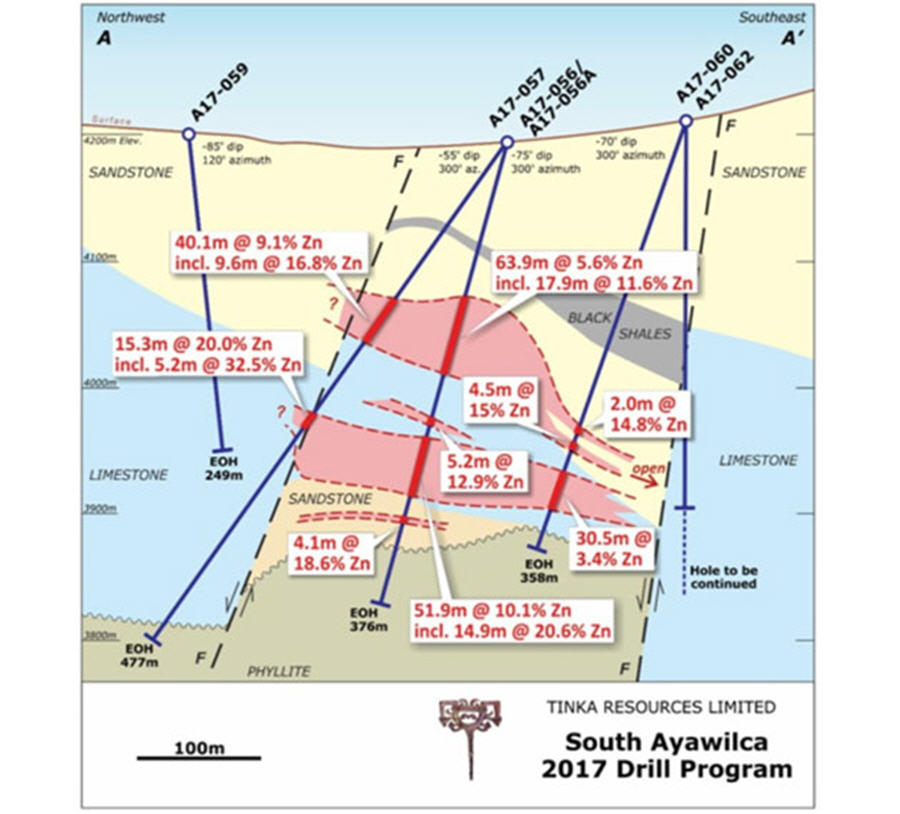

Let me first discuss the drill results of the current program so far, and the exploration potential as I see it, as a non-geologist. The first results came out on March 6 during PDAC on the South target and were very impressive: the first 238m of drill hole A17-056 intercepted 17.9m @ 11.6% as part of a 63.9m @ 5.6% intercept from 126m depth. The next round of drill results on April 3 was even better: the follow-up part, labeled A17-056A, reported another 52m @ 10.1% Zn, 62 g/t Ag, and 233 g/t In from 242m depth, which truly makes A17-056 a monster. The intercept features a higher-grade part that generated 14.9m @ 20.6% Zn, 15g/t Ag, and 441 g/t In. Drill hole A17-057 also reported impressive numbers with 40.1m @ 9.1% Zn, 22g/t Ag and 168g/t In. The third batch of drill holes was reported on May 3, showing slightly less spectacular results, although for example hole A17-061 returned 13m @ 19% Zn and 19m @ 10% Zn, accompanied with decent lead, silver and indium grades. This hole is located approximately 80m to the southwest of the section A-A’, showing the results of A17-060, the rest of A17-057 and A17-056A:

The markets didn’t act very enthusiastic about this as mentioned, but looking at the available information there wasn’t much that disappointed me, or it must have been A17-060, of which the longer intercept (30.5m @ 3.4%) didn’t return the higher grades encountered at other holes. Another thing is that Tinka had to suspend and redrill A17-062, no assays are pending here, but the geologists did notice another fault, which could both indicate not too much mineralization south of this new fault line, and basically limiting mineralization between these two fault lines.

Otherwise the drill core would have been assayed anyway in my view, as it hit the targeted limestone, and as it is relatively easy to visually recognize high-grade zinc mineralization. To date there is no further information about the trajectory of this second fault. As this fault line seems to be located very close to the southern edge of the magnetic anomaly, I am willing to guess that it could more or less run parallel to the SW/NE fault line, possibly creating a 50-250m wide mineralized zone towards the Main Zone, and I will use this to a certain extent for my hypothetical tonnage estimates later on.

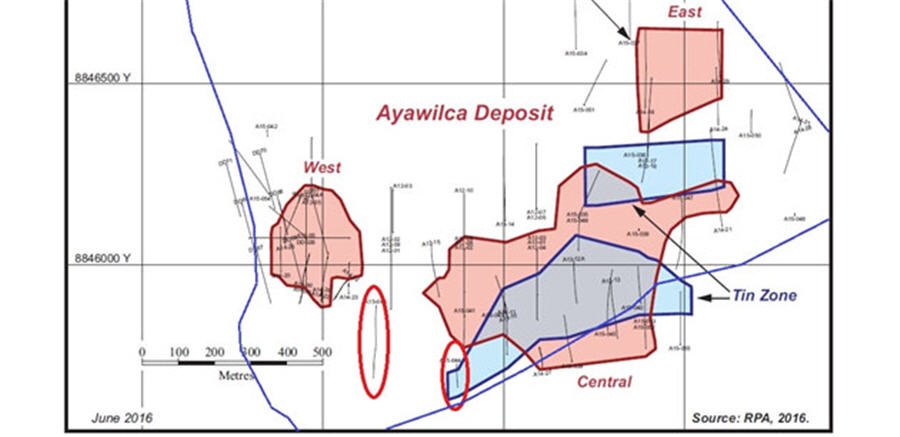

The small mineralized intercept of A17-056A beyond the fault line (left fault in the section) could mean not too much mineralization at depth to the north of the fault but maybe at higher elevation. Hole A17-059 will reveal more, as assays are still pending for this, but I don’t expect too much of this hole. I have my reasons for this. Here is an interesting piece of information, and it is a map of drill collars of drill programs prior to the current one, taken from the NI43-101 report:

I added the blue lines (left one is a thrust fault, others are known faults), and the red ellipses, to indicate drill holes that didn’t return economic mineralized results for zinc according to the NI43-101 report. As the current results are south of the southwest to northeast (SW/NE) trending fault, I’m not readily expecting a lot of zinc mineralization north of this fault and west of A15-046 and A15-044 (small ellipses). In my opinion, the best chance of success for the South Zone would be south of the SW/NE trending fault. Again, being a non-geologist and just speculating.

Speculating a bit more, let’s have a look at a potential size for the mineralized envelope. The density is, according to the resource estimate report, 3.6t/m3 for the Zinc Zone and even 3.9t/m3 for the Tin Zone, which is considerably higher than average limestone density (2.3t/m3). This is due to the presence of heavier sulphides. I will use 3.3t/m3 to be conservative. Looking at the section, a mineralized zone of on average 60m thick and an average grade of 6-7% Zn seems present, which is probably (very) economic as mining in Peru is much cheaper compared to for example Canada. More on this later. Considering the two fault lines, a width of 250m can be derived. As it is just a few holes, a 25m area of influence on both sides of each hole seems justified for now. This results in a mineralized envelope of 130m x 250m x 60m x 3.3t/m3 = 6.4Mt, and would increase the current deposit with 34%.

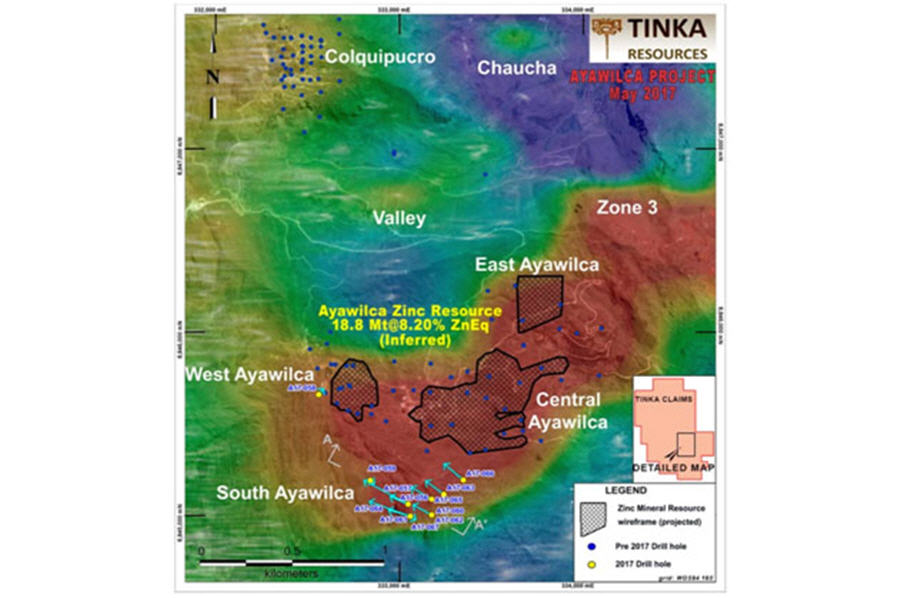

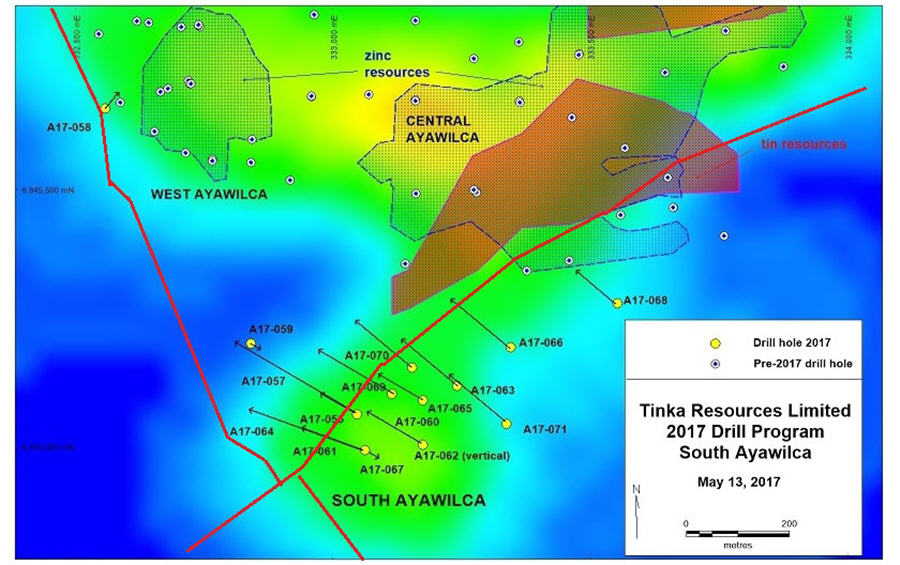

All this is just the beginning of the South Zone I might add. I don’t expect a strong connection between the Main Zone and the South Zone yet, but a connection is very well possible, and if there could be something like it, it might be happening most likely along and southeast of the SW/NE fault line. Again, speculating as a non-geologist. The company seems to think this way as well, when looking at this very recently updated drill hole location map (I added fault lines in red):

Ayawilca magnetic anomalies modeled at 4000 m RL (approx. 150 m depth)

If stepout holes A17-063, A17-065 and A17-66 would be equally as successful, and assuming the same patterns of mineralization extending between parallel faults towards Central Ayawilca (let’s call it trend), this would increase the envelope roughly to 500m x 250m x 60m x 3.3t/m3 = 24.75Mt, assuming continuous mineralization between holes estimated 100m apart of course. This shows the importance of long mineralized intercepts, as tonnage increases incredibly fast this way. The other mineralized envelopes of Ayawilca weren’t this thick, so it could be substantial, but confined to a relatively small area, capable of easily doubling the existing resource with a few similar holes as we have seen. If the average thickness decreases when following the “trend” to for example 40m, and the 250m wide zone narrows down to for example 50m, we still get 500m x 150m x 50m x 3.3t/m3 = 12.37Mt, which would still mean a very healthy tonnage increase to 31Mt.

Besides this, to me the biggest upside, after looking at the recon test results and especially the magnetics, seems to be located in Zone 3. Everything appears to look aligned in this area, and if Tinka hits big there, I can see Ayawilca easily going to 50-60Mt or more, making it a world-class zinc deposit. So as much as I am looking forward to more South Zone results, I am even more excited about Zone 3. I view Chaucha as interesting too at some distance, and as past drilling and recon testing indicate a smaller chance of success for Valley, everything coming out of this last target I regard as a bonus.

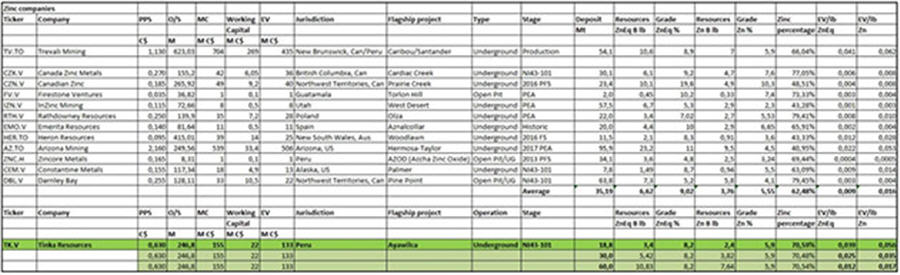

To get something of a feel for resources and figures of its peers, I lined up Tinka against 12 zinc juniors:

Considering the averages, Tinka isn’t anything special yet. Based on its EV/lb Zn ratio alone, Tinka has a rather rich valuation, and will continue to look expensive for optics unless it surpasses a 30-40Mt target. However, what this comparison doesn’t tell you, are the specific circumstances for each company valuation, and how economic these pounds all are. And, as always, every company in this table has its own unique story with positives and negatives, so be cautious. At least it gives you a quick impression. The two most important reasons for Tinka to have this high valuation are a. its pounds could probably be very economic, and b. expectations on much more exploration upside are high, being reinforced by the latest drill results.

6. Economic potential

As I am relatively new to zinc juniors and zinc mining, I didn’t have a very grounded and thorough idea about mining economics for this metal. Therefore I analyzed a number of economic studies to get an idea, and looked elsewhere for information. One of these sources is a retired mining engineer named Doug Beattie, who has considerable experience in zinc mining projects, but also designed Cameco’s flagship McArthur uranium mine, using the revolutionary combination of raise boring and a ground freezing method. Fortunately, Doug is so kind, being retired, to write down a lot of interesting information, links and thoughts on CEO.CA, a very useful mining platform for investors. He even madean impressive 12-part exposé about zinc mining in different jurisdictions, which can be found here, below the linked article in the commentary section. This information put me on the right track regarding looking for information one doesn’t come across very easily.

Before I get to actual economic estimates, I wanted to have a good impression of a number of variables myself. After analyzing various mines and projects, it can be seen that Peruvian operations do have lower mining costs per tonne compared to other jurisdictions, UG mining and processing are cheaper to the tune of almost 30-40%. This is likely due to cheap labor and power, and possibly positive FX-inflation effects.

With all this gathered information of numerous projects it should be possible to make very broad assumptions for Ayawilca economics.

I used three possible tonnage scenarios, ranging from very conservative to optimistic: a 20, 30 and a 60Mt resource. As mentioned, it isn’t very hard to imagine, if Tinka would be very successful, that even higher tonnage targets aren’t out of the question, but let’s stick with these three for now.

– LOM of 12/15/20y

– capex/tpd: $55k/$53k/$50k (economies of scale), I used the cheapest figures from Canadian studies as a reference, and this seems conservative since Peru is supposed to be cheaper no matter what (looking at opex numbers, my guess is capex numbers actually could come in 20-25% cheaper, as most equipment comes from abroad but there is still a decent amount of labor involved, which should be able to bring capex down)

– mill feed 75-80% of Reserves & Resources grade

– production tonnage 75-80% of resources

– recoveries Zn 90%, Pb 90%, Ag 60%, In 60%

– payability Zn 85%, Pb 95%, Ag 75%, In 55%

– concentrate Zn 52%, Pb 60%

– opex $/t ore: $40/$38/$37 (economies of scale)

– AISC $/ZnEq lbs: $0.75/$0.70/$0.72 > US$0.60/US$0.56/US$0.57

– metal prices Zn $1.1, Pb 1, Ag $17.5, In $500 (comes from NI43-101 Ayawilca, spot In is lower)

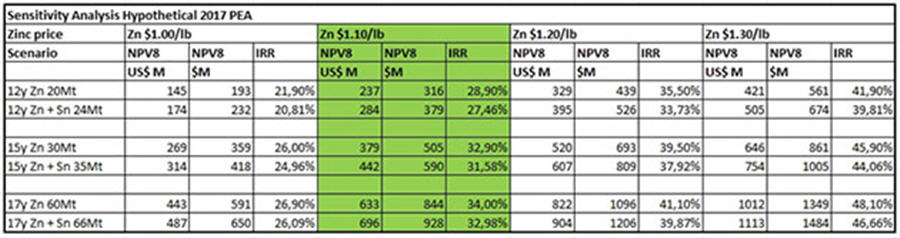

After running my models on the 3 scenarios, I constructed a sensitivity analysis, which indicates a viable project at all scenarios including US$1.00/lb Zn, signalling a very profitable base metal project:

At a current F/D market cap of CA$158M, it will be clear that Tinka could already be trading close to 40-50% of my hypothetical post-tax NPV8 based on its current resource, without any economic study being completed, but this resource is just the beginning in my view. The sensitivity analysis shows what could happen with a larger resource and a higher zinc price. For the zinc bulls among us, a zinc price of US$1.50/lb could result for example for the 30Mt scenario in a hypothetical post-tax NPV8 of US$896M, which is CA$1195M. Let alone the 60Mt scenario or even more.

A share price target is something of a stretch at this early stage, but as Arizona Mining already traded at close to half NPV8 @ US$1.10/lb Zn before the PEA came out and before its (largely unjustified as they had to be more transparent about the presence of deleterious elements, but penalties are very unlikely to materially impact economics) manganese penalty circus started, there seems to be enough room to appreciate on a larger resource. As economics of Ayawilca look destined to be very good, there is no doubt in my mind that the surrounding producers are fixated on any drill results being published by Tinka, probably feeding them enthusiastically to their own models. With zinc fundamentals being strong well into 2018, a possible take over doesn’t seem unrealistic at all, and I would be surprised if Tinka is still around at the end of 2018.

7. Conclusion

Tinka Resources is rapidly turning into the market darling of zinc juniors, as the first drill results already look very promising, and indicate a strongly mineralized South Zone as anticipated by management. However, this seems to be only the beginning of stepout drilling, and my expectations for especially Zone 3 are equally substantial, and could elevate Tinka into the realm of Tier I asset owners, and would likely generate interest from nearby suitors by doing so.

It is the possible exploration upside combined with possible future economics that will make the big difference here, as mining in Peru is much cheaper than in most of the other peer’s jurisdictions. As the possible resource update comes out depending on outcomes of the current drill program and a PEA shortly after this, this will be the time for Tinka Resources to really set itself apart from peers in my view. It looks like 2017 is shaping up to be an exciting year for Tinka, and I would suggest to at least follow it closely from now on.

The extended version of this article will be published soon on criticalinvestor.eu

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter at http://www.criticalinvestor.eu/, in order to get an email notice of my new articles soon after they are published.

The Critical Investor Disclaimer:

The author is not a registered investment advisor, and has a long position in this stock, Emerita Resources and Darnley Bay. Tinka Resources is a sponsoring company. The views, opinions, estimates or forecasts regarding Tinka’s performance are those of the author alone and do not represent opinions, forecasts or predictions of Tinka or Tinka’s management. Tinka has not in any way endorsed the information, conclusions or recommendations provided by the author.

All facts are to be checked by the reader. For more information go to https://www.tinkaresources.com/www.tinkaresources.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long term commodity pricing/market sentiments, and often looking for long term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

Streetwise Reports Disclosure:

1) The Critical Investor: The author, or members of the immediate household or family, own shares of the following companies mentioned in this article: Tinka Resources. The author’s company has a financial relationship with the following companies mentioned in this article: Tinka Resources.

2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Source: The Critical Investor for The Gold Report (5/15/17)

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments