Canada’s critical minerals push faces capital gap: RBC

Canada has channelled just 11% of its mining capital into critical minerals over the past 25 years, leaving the country behind global peers as demand for strategic resources accelerates, a new RBC report shows.

More than C$700 billion ($512 billion) has been raised in Canadian mining equity and mergers and acquisitions since 2000, with 70% flowing to gold and precious metals, according to S&P Capital IQ and LSEG data cited by RBC.

Shaz Merwat, the bank’s director of energy policy and author of the report, said that in comparison, Australia channeled more than twice as much capital into critical minerals over the same period.

That gap matters. The International Energy Agency (IEA) projects the global critical minerals industry will grow two to three times by 2040, requiring $500–$600 billion in capital. Demand for cobalt, copper, graphite, lithium, nickel and rare earth elements is rising, driven by electric vehicles, clean energy infrastructure, defence, manufacturing and electronics.

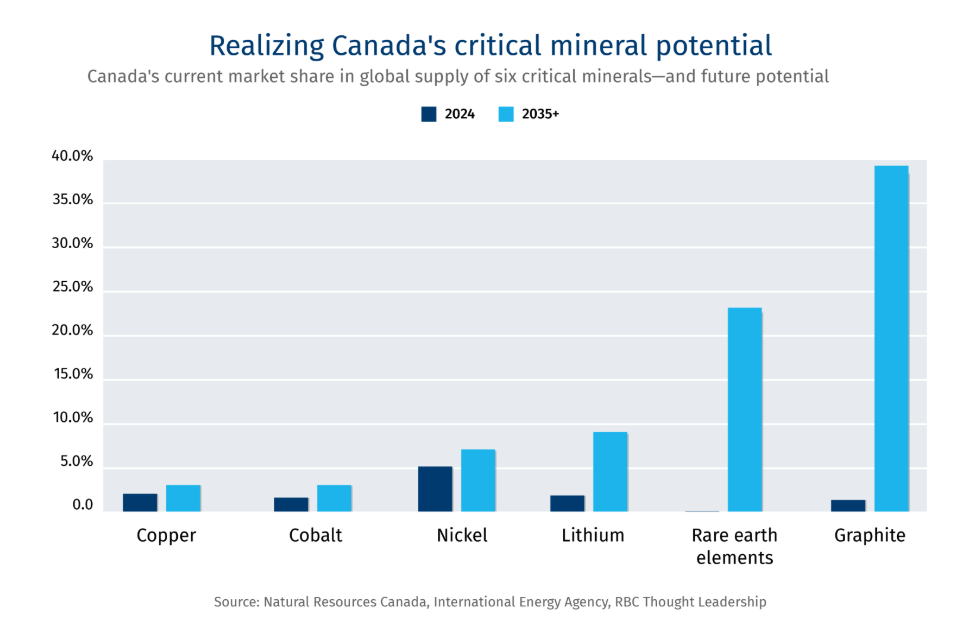

Canada holds significant deposits of those minerals but supplies about 2% of global output. If all identified projects proceed at full capacity, that share could rise to 14% over the next 15 years, according to federal estimates, RBC said.

Ottawa is trying to close the gap. About 67 critical minerals projects, roughly half of all active mining proposals in the country, are planned, proposed or under construction. Together, they represent C$72.4 billion ($53 billion) in potential investment by 2034, according to Canada’s Major Projects Inventory.

Yet the country largely operates as a mine-and-ship jurisdiction. It has only one active copper smelter, Glencore’s (LON: GLEN) Horne facility in Rouyn-Noranda, Quebec, along with its associated refinery.

Producers have to export raw concentrates, primarily to China, for refining into higher-value components. China controls about 70% of global refining capacity for 19 of the 20 most critical minerals, supported by state-backed capital, lower costs and deliberate overcapacity that pressures competitors.

Structural barriers

RBC identifies structural barriers that have left the sector undercapitalized. Between 2005 and 2012, more than C$119 billion ($87 billion) in Canadian base metals and steel assets shifted to foreign ownership, reducing the number of domestically anchored mining leaders. Over three decades, Western countries outsourced energy-intensive refining to China, making it difficult to compete with subsidized overcapacity, especially in standalone processing.

Domestic demand remains limited. Canada’s battery cell manufacturing sector is still emerging, defence procurement operates at a fraction of US scale, and magnet and rare earth processing industries are largely absent. As a result, concentrates flow to markets where customers are concentrated.

This shortfall persists even after Ottawa committed up to C$55 billion ($40 billion) over 15 years to attract electric vehicle and battery manufacturers.

Unlike Germany, France and South Korea, Canada did not impose strict domestic sourcing requirements on subsidy recipients, limiting spillover benefits for upstream miners and processors.

Financing shortfalls also constrain growth. Canada’s flow-through share regime supports early-stage exploration, but funding drops sharply during feasibility, permitting and construction. Companies often face a C$20–C$30 million funding gap before reaching a final investment decision, which encourages asset sales rather than mine development.

Permitting delays add further risk. Federal and provincial reviews can stretch beyond five years without fixed timelines, increasing uncertainty and deterring investment.

Pulling forces

RBC argues market forces alone will not correct the imbalance. It calls for a co-ordinated public-private strategy centred on sovereign co-investment, infrastructure funding and tighter integration with allied supply chains.

Ottawa’s C$2-billion Critical Minerals Sovereign Wealth Fund remains modest relative to global capital flows. The Canada Growth Fund has begun co-investing in projects including Nouveau Monde’s (NYSE: NMG) graphite project in Quebec, Foran Mining’s (TSX:FOM) project in Saskatchewan, soon to be part of Eldorado Gold’s (TSX: ELD) (NYSE: EGO) portfolio, and the Thompson nickel mine complex in Manitoba, signaling federal backing to private investors.

Infrastructure could deliver the fastest gains. Analysis by the Canada Infrastructure Bank suggests co-investment in roads, transmission lines and grid connections to remote regions could reduce a project’s break-even price by 22–24%. Ontario’s Ring of Fire region alone requires up to C$2.4 billion in enabling infrastructure before major deposits become commercially viable.

RBC also proposes developing mineral corridors that cluster mining and shared processing facilities in regions such as Quebec’s lithium belt and Ontario’s Sudbury nickel district. Shared refining hubs, supported by government loan guarantees and anchor offtake agreements with battery manufacturers in Europe and Asia, could improve project economics.

The US is also reshaping supply chains. The US Office of Strategic Capital can deploy $100–200 billion to strengthen defence and industrial supply chains, and Washington’s $12-billion Project Vault critical minerals stockpile is operational.

Closer integration could secure offtake for Canadian producers but carries risks if US export licensing or procurement rules subordinate Canadian supply to American industrial priorities. RBC recommends diversifying trade ties with European and Asian allies to preserve resource sovereignty while anchoring demand.

Australia offers a contrast. Pension funds maintain standing allocations to resources, supporting a deeper pool of mid-tier producers. Statutory timelines reduce permitting uncertainty, and commodity diversification helped build global majors such as BHP (ASX: BHP) and Rio Tinto (ASX: RIO) that now invest heavily in energy-transition metals.

In Canada, decades of capital consolidation around gold reshaped public markets into a precious metals financing platform. That strength did not translate into leadership in battery metals, where processing is more complex and capital intensive.

The country could raise its share of global output in six key minerals to 14% by 2040 from 2% today if projects proceed, according to the report. But only 19% of mining firms on the S&P/TSX Composite are diversified miners, compared with about two-thirds in Australia’s ASX 300 mining index.

After two decades of capital allocation focused elsewhere, Canada has world-class geology but limited downstream capacity and patient risk capital. Without a decisive shift, RBC warns, the country risks remaining a supplier of raw materials while others capture the value-added processing and geopolitical leverage.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments