Chile mining sector faces policy test under Kast government

Chile’s mining sector faces a policy reset as President José Antonio Kast took office on March 11, raising expectations of regulatory reform and stronger security in the world’s largest copper-producing nation.

Kast, leader of the Republican Party, assumed the presidency in Santiago today after a transfer of power from outgoing president Gabriel Boric, marking another swing in Chile’s long-standing political cycle between left- and right-leaning governments.

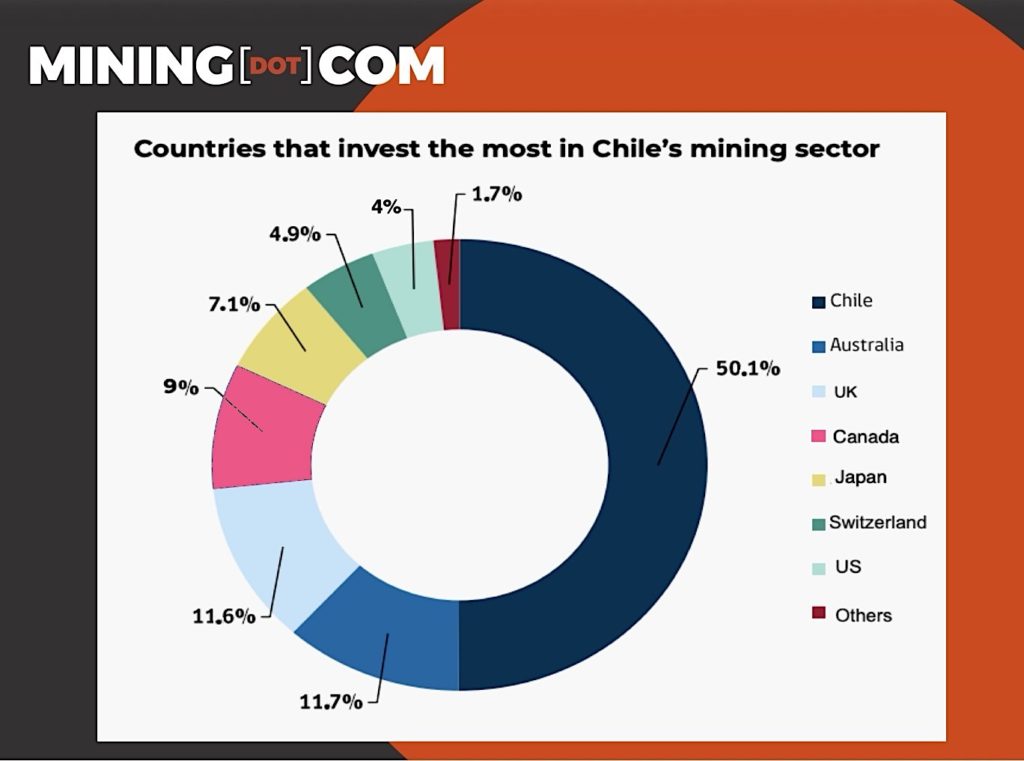

For the mining industry, the change in government could shape the regulatory and geopolitical environment for a sector that underpins Chile’s economy. Mining accounts for about 11% to 12% of GDP and more than 20% when indirect effects are included.

Ministries merger

One of Kast’s first structural changes was merging the ministries of Mining and Economy into a single portfolio. He appointed agronomist Daniel Mas to lead the combined ministry, a choice that surprised parts of the industry given Mas’s lack of mining experience.

Carlos Piñeiro, a copper analyst at Benchmark Mineral Intelligence, said the merger could improve coordination across economic policy but risks weakening technical focus. “Mining has very particular challenges, especially the non-renewability of resources,” he told MINING.COM. “If this model is going to work, specialists need to be involved in decision-making.”

Industry groups are more critical. “Mining, despite being our national emblem and the activity that contributes the most resources to the public purse, is treated as second-rate,” Manuel Viera, president of the Chilean Mining Chamber, said. Previous attempts to place mining under broader economic portfolios “have not been positive,” he added.

“Cursed” system

Mas takes charge of a sector expected to attract about $105 billion in investment by 2034. Companies are also pushing for reforms to Chile’s permitting and environmental assessment systems, which industry groups say have slowed project approvals and increased costs.

Viera described the permitting system as “cursed,” noting that a single mining project can require more than 500 permits before construction begins.

Analysts say the government’s credibility with investors will depend largely on whether it can shorten approval timelines and reduce procedural delays.

Copper strain

Chile remains the world’s largest copper producer, accounting for roughly a quarter of global mined supply. Yet growth has been constrained by declining ore grades, ageing deposits and regulatory complexity.

Production fell 2% in 2025 compared with 2024, according to the state copper commission Cochilco, and declined year-on-year in every month of the year.

“Deposits are becoming deeper and lower grade,” Piñeiro said, adding that jurisdictions such as the Democratic Republic of Congo benefit from higher grades and lower costs.

Kast’s team has floated boosting mining output by as much as 20% within a year or two, but analysts say that target is more a political signal than a realistic timeline.

Mariano Machado, Americas analyst at risk intelligence firm Verisk Maplecroft, said the goal “signals urgency, not an immediate step change,” noting that Chile’s mature mines and long project timelines limit how quickly production can increase.

Cochilco projections suggest national copper output could rise modestly before peaking mid-decade and gradually declining to about 4.4 million tonnes by 2034 unless new projects advance.

Before the Iran war, experts estimated Chile could receive up to $4 billion in additional revenue from soaring copper prices, but the metal has been volatile in recent weeks, dropping as much as 8% from recent highs. As of Tuesday, copper had rebounded to $13,098.

Energy Pressures

Chile is also one of the largest oil importers in Latin America due to its lack of domestic production, increasing the impact of rising oil prices, which have climbed to nearly $120 a barrel since the start of the war.

“The Iran war has increased inflation risks considerably,” Oxford Economics said in a report surveying emerging markets published on Monday.

A spokesperson for Kast’s economic team said no economic contingency measures were planned for now, but did not elaborate on how recent developments could affect the government’s economic agenda.

Critical minerals

Beyond copper, Chile is seeking to broaden its mining base. In the final weeks of Boric’s administration, the government released the country’s first critical minerals strategy, aiming to expand production beyond copper and lithium to 14 additional minerals tied to the energy transition and resilient supply chains.

These include molybdenum, cobalt, rare earth elements, antimony, gold, silver, iron ore and boron.

Piñeiro said Chile’s mineral base is already more diverse than commonly assumed, citing strong output of molybdenum, rhenium, iodine and nitrates, as well as a recovery in gold production. Projects such as Salares del Norte could lift national gold output by about 25%.

Still, copper remains the backbone of Chile’s economy and will likely remain so through at least 2035.

“Depending almost exclusively on copper exposes the country to market cycles and uncertainty,” Viera said.

Lithium outlook

Lithium is another area of opportunity, but policy uncertainty persists. Chile remains the world’s second-largest lithium producer and hosts some of the lowest-cost brine deposits, particularly in the Atacama Salt Flat.

However, a national lithium strategy unveiled in 2023 increased state involvement in the sector and reshaped project development pathways.

Piñeiro said Chile’s cost advantage remains significant, while Viera argued that restrictions in the Mining Code reserving lithium for the state have discouraged private investment.

Several projects could influence future output, including Nova Andino Litio, a joint venture between Codelco and SQM, and Salares Altoandinos. Codelco is also pursuing a lithium partnership with Rio Tinto (ASX: RIO) at the Maricunga salt flat, pending antitrust approvals in Chile and China.

Geopolitical shift

Chile’s mining outlook is also increasingly shaped by geopolitics. Global demand for copper, lithium and other critical minerals is rising as the US and its allies attempt to secure supply chains for the energy transition.

On the international stage, Kast comes to power at a geopolitical crossroads, caught between Washington seeking to reassert influence in Latin America and China, the main trading partner for Chile and much of the region.

The lawyer and leader of the Chilean Republican Party has already begun signalling his foreign policy direction. He drew criticism over the weekend for attending the launch of US President Donald Trump’s “Shield of the Americas,” a security alliance aimed at coordinating regional action against organised crime and drug cartels.

Kast has also cultivated ties with conservative leaders abroad. He spoke at a Conservative Political Action Conference summit in Hungary last year and previously met El Salvador’s security minister during the country’s controversial crackdown on gangs.

While Kast has largely avoided detailed comment on contentious issues at home and abroad, he has made overtures to the Trump administration and praised the US operation that led to the capture of former Venezuelan president Nicolás Maduro.

Eduardo Zamanillo and Marta Rivera, authors of Mining is Dead. Long Live Geopolitical Mining, say Chile could strengthen its position by moving beyond concentrate exports toward more refined copper production and midstream processing.

Trade data show that much of Chile’s copper still goes to China as bulk concentrate, while smaller volumes of refined copper are exported to the US and other allied markets.

Security concerns may also influence mining regions. Rising public anxiety over crime and migration, particularly in northern regions such as Antofagasta and Tarapacá where copper and lithium production is concentrated, played a role in Kast’s election campaign.

For investors, the key issue is whether the new administration can deliver reforms.

“The resources exist,” Viera said. “What is missing is a promotional and development plan that encourages exploration, investment and production.”

———

Latin America is heading into 2026 with resources at the centre of a growing global power struggle, as governments and investors focus on who controls critical minerals and the supply chains behind them. If the region matters to you, don’t miss MINING.COM’s new series tracking the geopolitical forces reshaping it and why markets are increasingly driven by global alliances as much as local politics.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments