Venezuela mining reset meets ground-level challenges

Venezuela’s attempt to revive its mining sector after Nicolás Maduro’s ouster is colliding with decades of institutional decay, illegal extraction and investor skepticism, even as the country moves to open one of the world’s most resource-rich frontiers to foreign capital.

The capture of Maduro by US forces in January marked a dramatic break with decades of political and economic isolation and could reshape Venezuela’s economic model. Alongside the country’s oil wealth, Caracas is now repositioning vast reserves of gold, iron ore and critical minerals as central to the nation’s recovery.

The push has been accelerated by US President Donald Trump’s administration, which moved quickly after Maduro’s removal to ease sanctions, reopen financial channels and encourage American firms to re-enter Venezuela. Washington has framed the country not only as a geopolitical project but as a strategic resource opportunity spanning oil, gold and critical minerals.

Caracas has responded by dismantling parts of its old resource nationalism framework under acting President Delcy Rodríguez. Her government has actively courted mining firms, pitching the country’s underdeveloped mineral belt as one of the last largely untapped resource frontiers in the Americas, even as security and governance risks remain acute.

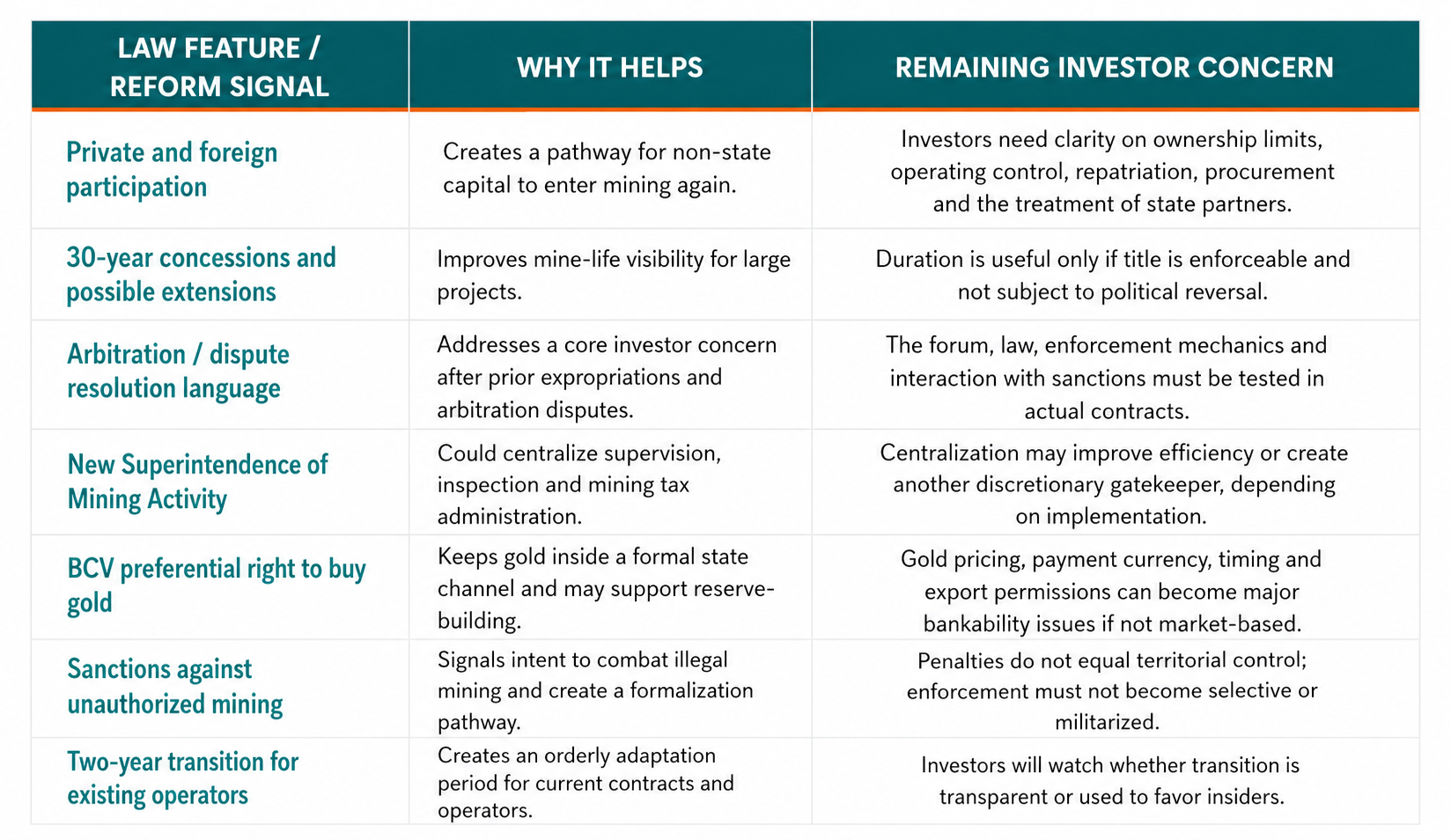

“The law creates a clearer formal framework for investment and longer concessions,” Ed Zamanillo and Marta Rivera Muñoz, analysts at Geopolitical Mining, told MINING.COM.

The clearest sign of the shift came in April when lawmakers approved a sweeping new mining law designed to attract international participation. Analysts at GEM Mining Consulting said the legislation creates “a legal route for domestic and foreign companies,” formalizes concessions for large-scale projects and signals an effort to regularize operators while cracking down on unauthorized mining.

A sector built in oil’s shadow

For most of the 20th century, mining existed in the shadow of oil despite major iron ore, bauxite, coal and gold deposits. While Venezuela built significant iron ore operations in regions such as Ciudad Guayana, petroleum revenues dominated state planning and left the broader mining sector underdeveloped.

Early expectations for the sector were far more ambitious. By the 1950s and 1960s, Venezuela had emerged as a major iron ore exporter supplying the US market. Early optimism was substantial.

In 1956, The New York Times reported that newly identified mineral reserves could “approach [the] nation’s oil in importance,” reflecting a period of optimism following major iron ore discoveries in the Guayana region.

These discoveries—alongside earlier finds such as Cerro Bolívar and El Pao—positioned Venezuela as a potential global iron ore powerhouse, attracting significant US investment and sparking large-scale industrial development tied to export markets.

Even so, mining never fully escaped the gravitational pull of oil. Despite its geological potential, the sector remained underdeveloped relative to its resource base, with limited diversification and a heavy reliance on foreign expertise and capital. This early pattern—strong resource endowment paired with uneven institutional development—would prove persistent.

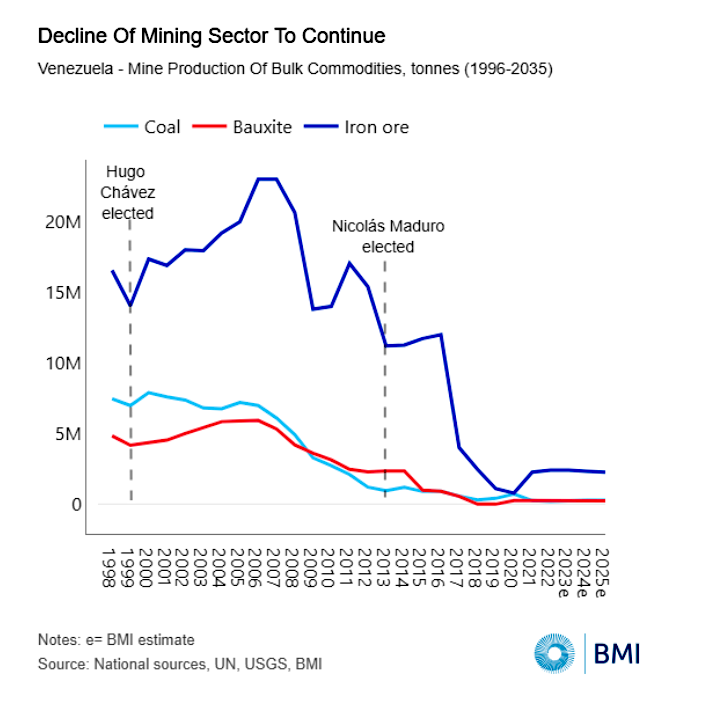

That balance began to shift in the years leading up to—and especially following—the rise of resource nationalism under Hugo Chávez in the late 1990s. While Chávez’s policies focused primarily on asserting state control over oil, the broader approach to natural resources set the tone for mining as well: greater state ownership, tighter control over foreign operators and an increasingly politicized regulatory environment.

Over time, investment slowed, infrastructure deteriorated and institutional capacity weakened—laying the groundwork for the collapse that would follow. By the time Nicolás Maduro took office in 2013, the mining sector was already losing coherence.

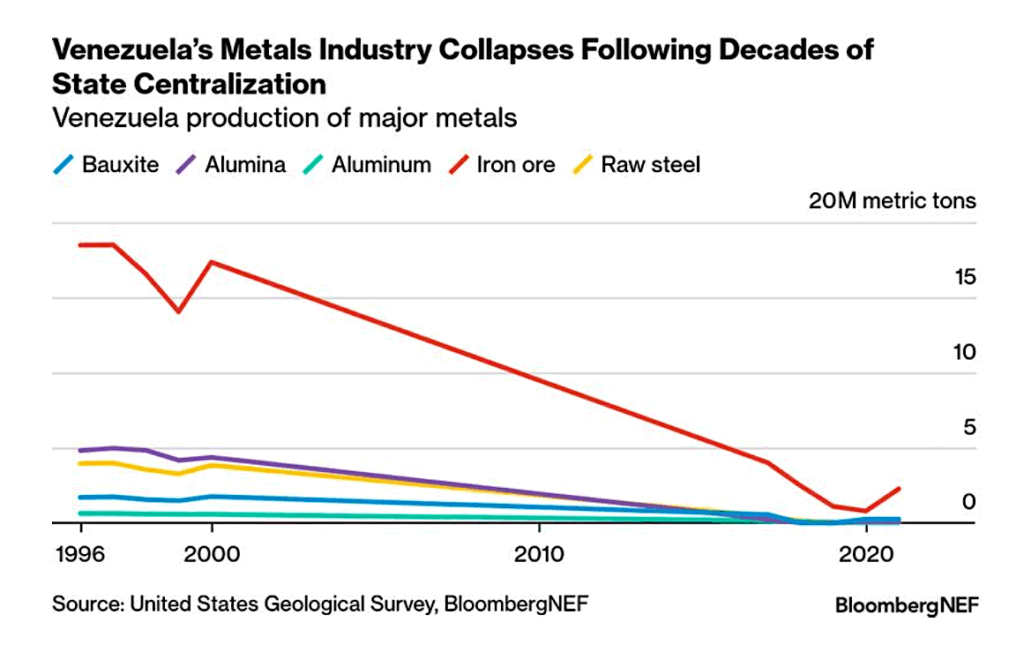

In the decades that spanned the two regimes, Venezuela’s mining output cratered. According to data compiled by BMI, a unit of Fitch Solutions, the minerals that anchored Venezuela’s mining sector — coal, bauxite and iron ore — had a dramatic decline. BloombergNEF estimates that its metals production shrank by more than 90% over the past 20 decades.

What had once been a modest but functional industrial base was beginning to fragment, setting the stage for the “informalization”, illegal extraction and security challenges that now define much of Venezuela’s mineral economy.

Any reform, including the recent mining bill, will “depend on the state’s ability to enforce standards, secure the territory, and give credibility to the larger mining environment,” Geopolitical Mining’s Zamanillo told MINING.COM, adding that the nation can become “a genuine future supplier” of critical minerals, providing the establishment of secure and governable conditions for formal mining under the current regime.

Broad, but undeveloped resource

Setting political reform aside, what exactly does Venezuela bring to the table—and is its mineral wealth as strategic as current headlines suggest?

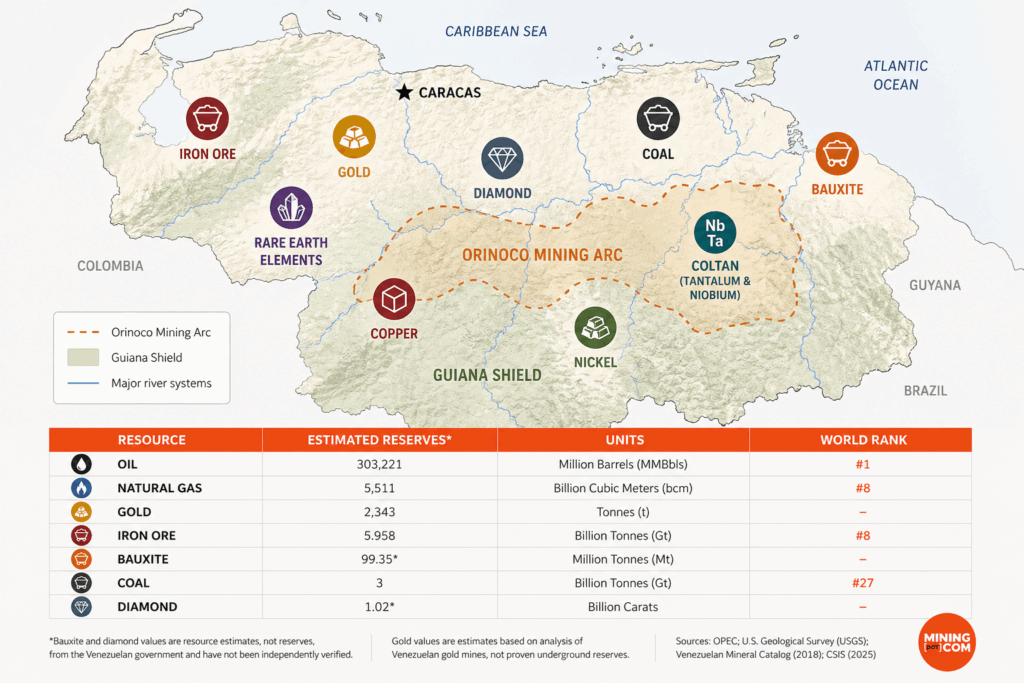

According to a 2026 analysis by the Center for Strategic and International Studies (CSIS), Venezuela holds an estimated 75 million oz. of gold, placing it in the same broad range as major South American producers like Brazil and Peru. Much of this wealth is concentrated in the Guayana Shield and the vast Orinoco Mining Arc, a 112,000-square-kilometre zone in Bolivar state that is believed to contain over 7,000 tonnes of gold.

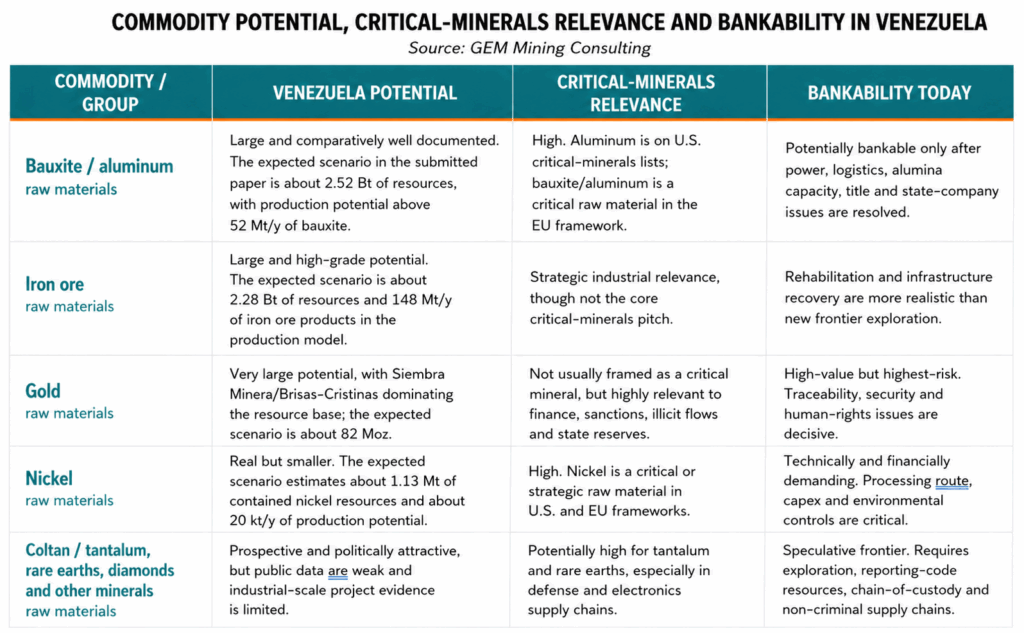

Beyond gold, Venezuela hosts a wide mix of industrial and critical minerals that, on paper, align with global supply chain needs. These include iron ore, bauxite (for aluminum), nickel, and coal, as well as lesser-developed but increasingly strategic materials such as coltan (tantalum-niobium), rare earth elements and potentially copper.

GEM pegged the estimated gold, iron ore and bauxite resources at 82 million oz., 2.3 billion tonnes and 2.5 billion tonnes, respectively. These, it said, have the most near-term potential of all minerals, supporting annual production of 52 million tonnes for bauxite, 148 million tonnes for iron ore products and 2.1 million oz. of gold.

The Guayana region in particular is often cited as one of the most mineral-rich geological formations in the Western Hemisphere. Back in 1990, the US Geological Survey had already documented occurrences of some of the aforementioned minerals within the Guayana Shield.

These findings more or less align with official data. In 2018, the Venezuelan government published a mining catalogue that listed a wide spectrum of resources, some with substantial volume (albeit speculative in nature). These include a massive iron ore resource that is pegged at nearly 6 gigatonnes and a coal resource half that size.

The government also published in 2021 a map of mineral reserves based on data compiled years ago, showing reserves of antimony, copper, nickel, coltan, molybdenum, magnesium, silver, zinc, titanium, tungsten and uranium, but did not list volumes.

Yet these reports all temper the headline potential with a critical caveat: Venezuela’s mineral wealth is broad rather than dominant. Unlike Chile’s copper or Bolivia’s lithium, the country lacks a single globally leading commodity position, meaning its strategic value lies in diversity rather than scale leadership. In other words, Venezuela is not a cornerstone supplier of any one critical mineral—but it could become a supplementary source across several.

That distinction matters. In a world increasingly defined by supply chain security, Venezuela’s minerals are less about overwhelming volume and more about optionality. The country offers a rare combination of gold, industrial metals and emerging critical minerals within a single jurisdiction—an attractive proposition for governments and companies seeking to diversify away from dominant producers.

Whether that potential can be translated into reliable output, however, remains a far more uncertain question.

Sector taken by disorder

But if Venezuela’s mineral potential is undeniable, its recent mining history tells a far more complicated story—one defined less by development than by disorder.

Over the past decade, the sector has been reshaped by the rise of illegal and informal mining, particularly after the creation of the above-mentioned Orinoco Arc in 2016. Originally designed to attract large-scale investment, the initiative instead accelerated unregulated activity. Gold output today is driven largely by informal operations rather than state-controlled projects.

The consequences have been profound. In many mineral-rich regions, control has shifted from the state to a patchwork of armed groups, criminal networks and informal syndicates. These actors now compete for key deposits—especially gold, coltan and diamonds—effectively creating a parallel mining economy. A report by the International Crisis Group highlights that illegal mining in southern states like Bolívar and Amazonas is generating vast revenues for these groups, fueling violence and entrenching their territorial control.

In practice, this has turned mining zones into fragmented, quasi-governed territories. Armed groups regulate access, tax production, and enforce their own rules—often violently. Crisis Group notes that this system not only sustains criminal economies but also deepens humanitarian pressures, particularly on Indigenous communities who face displacement, coercion, and environmental degradation.

Conditions on the ground underscore the scale of the challenge. Those that operated in Bolivar believe meaningful foreign investment will remain difficult without major improvements in security, where local criminal groups operate alongside Colombian rebels and where security forces have been accused of colluding with illegal mining networks.

“The syndicates control the mines. They’re the ones who set the rules and enforce the law in many of the mines where we work,” an informal miner in El Callao said in a Reuters interview earlier this year.

The result is a sector with fragmented sovereignty. Even where the state retains formal ownership, enforcement is weak, and alleged official complicity further blurs the line between legal and illegal activity. For investors, mining rights on paper rarely guarantee control on the ground.

Environmental and social impacts have only deepened the challenge. According to Crisis Group, mining activities have penetrated 27 of the 41 protected areas in Venezuela’s Amazon region, while a 2022 decision to lift restrictions on river mining further contaminated the waterways of Bolívar state, which provide 90% of the country’s fresh water.

Faced with hazardous conditions, many Indigenous communities were forced to leave their homes for a safer, better future. It is estimated that over 1,500 Indigenous communities currently reside in the southern Bolívar and Amazonas states, many of which are facing pressure to acquiesce to mining activity in their territories, Crisis Group said.

These are not side effects—but an endemic within Venezuela’s mining sector that would take time to cure. This “would require a sustained institutional effort and a much clearer understanding of present conditions in Bolívar and the Orinoco Mining Arc,” analysts at Geopolitical Mining told MINING.COM.

“In our view, what currently exists in important parts of the territory, and what could persist even under a legalized framework, is anomic mining: a setting in which extraction continues without a coherent alignment between authority, legality, enforcement, and legitimacy,” they added.

Venezuela’s core challenge is that much of the gold economy is not simply “unregulated.” It is embedded in local survival economies, criminal taxation, militarized control, mercury-dependent processing, weak state services and cross-border illicit trade, GEM analysts also said.

Taken together, Venezuela presents a stark paradox: vast geological potential paired with a mining industry defined by instability, opacity and risk. Any effort to rebuild the sector will have to contend with this deeply entrenched informal system that now dominates much of the country’s resource extraction.

America-led rebuild

For the next decade, the big question is whether a Venezuela reset translates into real investment—or stall at the policy level.

“At present, Venezuela is better understood as a mining proposition in an early stage of reconstruction. Its long-term significance could be considerable, given the scale of its resource base and the strategic relevance of minerals such as gold, iron ore, and bauxite,” analysts at Geopolitical Mining said.

The immediate outlook depends on whether recent reforms can deliver basic stability. The newly passed mining law stipulates all entities — not just domestic or state-owned ones — can exploit gold and other “strategic minerals” for 30 years.

While the move essentially opens Venezuela’s mining sector to foreign participation, investors remain focused on security, contract enforcement and operational control.

There are already signs of tentative re-engagement. Gold Reserve, long linked to the Brisas–Las Cristinas project, is viewed as a potential first mover if conditions stabilize. Bloomberg News reported a group backed by Vancouver businessman Richard Warke could invest as much as $200 million into reviving the Siembra Minera project, estimated to host more than 52 million oz. of gold.

Rusoro Mining, whose Venezuelan assets were nationalized years ago, is also considered a possible return candidate.

Earlier this year, US Interior Secretary Doug Burgum brought prominent mining executives to visit Caracas as he vouched for Washington’s backing for Venezuela’s mineral sector. Trading houses like Trafigura have also begun testing the waters, reopening limited gold flows and signaling cautious commercial interest.

For now, however, most miners are holding back, waiting for clearer evidence that risks on the ground are manageable. “For real investment to take place it is essential to resolve supply‑chain transparency and security,” an anonymous source from state-owned miner Minerven said, cited by Reuters.

Washington has played a central role in this shift. The Trump administration has already moved to ease restrictions, including the issuance of “general licenses” that allow certain transactions with Venezuelan entities, with the aim of reopening commercial channels and facilitating foreign participation in the sector.

A Venezuela rebuild would also be welcomed by its Latin American peers. Speaking to Reuters, Brazil’s Finance Minister Dario Duriga reaffirmed that “Venezuela is a relevant regional player and should turn the page to regain economic strength.”

A long road back

Still, the country may be embarking on what could be a long road back to its former glory. BMI estimates that its production of iron ore alone fell ten-fold from 20 million tonnes to 2 million, while its bauxite and coal outputs shrank even more.

According to Luis Rojas Macha, president of the nation’s mining chamber, Venezuela may need as much as $50 billion to rebuild its mining and metals sector from the ground up after years of neglect. “One thing is the mineral wealth, another thing is the ability to develop it,” he told BNAmericas.

The recovery, if any, is likely to be gradual. The country reportedly restarted coal production last year and is seeing a resurgence in its iron ore output. Any progress in other minerals will likely come through selective project restarts and small-scale partnerships rather than a rapid return to large industrial operations. The bigger test is whether the state can reassert control over mining regions and formalize production.

“Given the opaque nature of Venezuela’s official and black-market economy, we cannot say for sure what the real prospects are for critical mineral development,” Michael Cembalest, chairman of market and investment strategy for JP Morgan Asset & Wealth Management, said in a note earlier this year.

“But it’s notable that China, which controls the vast majority of critical mineral mining and processing activities around the world, is active in Venezuela.”

Then comes its future place in the global critical minerals race. While the potential is there, analysts are skeptical of the country’s ability to become a genuine near-term supplier in the way that Chile is for copper and lithium, or Brazil for its vast rare earths.

“It remains speculative for rare earths, coltan/tantalum and other critical minerals until exploration and chain-of-custody improve,” GEM consultants told MINING.COM, noting that the country is still less investable than Argentina, Brazil, Chile, Peru, Ecuador or Guyana today.

Still, with a new mining law, Venezuela’s mining story has nevertheless changed in 2026 because legal, sanctions and geopolitical signals moved almost at the same time, they stressed. “These changes make Venezuela look different from the Venezuela that most mining investors avoided after expropriations, sanctions and the collapse of formal production. However, they do not erase the country’s democratic and institutional discount.”

Venezuela’s resource base is not in question. The challenge now is execution.

———

Latin America is heading into 2026 with resources at the centre of a growing global power struggle, as governments and investors focus on who controls critical minerals and the supply chains behind them. If the region matters to you, don’t miss MINING.COM’s new series tracking the geopolitical forces reshaping it and why markets are increasingly driven by global alliances as much as local politics.

Other countries in the series:

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments