Acid test: IEA warns copper supply outlook has “worsened considerably”

Copper mines producing more than a seventh of the world’s primary supply are now hostage to a sulphuric acid market thrown into chaos by the Middle East conflict and Beijing’s export ban, according to the International Energy Agency, which warns the metal faces “a strong set of near-term challenges” even as its long-term supply picture modestly improves.

In its newly released Global Critical Minerals Outlook 2026, the Paris-based agency says the copper market’s short- and medium-term prospects have deteriorated sharply over the past year:

“Despite a slightly improved long-term outlook, the short- and medium-term supply outlook appears to have worsened considerably. Constraints on sulphuric acid availability pose a significant risk to SxEW production. Coupled with slower-than-expected recoveries from disruptions at major mines and an already tight market, the copper market faces a strong set of near-term challenges.”

The acid problem is a direct casualty of the effective closure of the Strait of Hormuz in February, which choked off the route for around half of global seaborne sulphur trade – the key feedstock for sulphuric acid – from Gulf countries and Iran, which together account for a quarter of world sulphur supply. Compounding the shock, China implemented a ban on sulphuric acid exports from May until the end of the year, cutting off almost a quarter of ex-China acid needs.

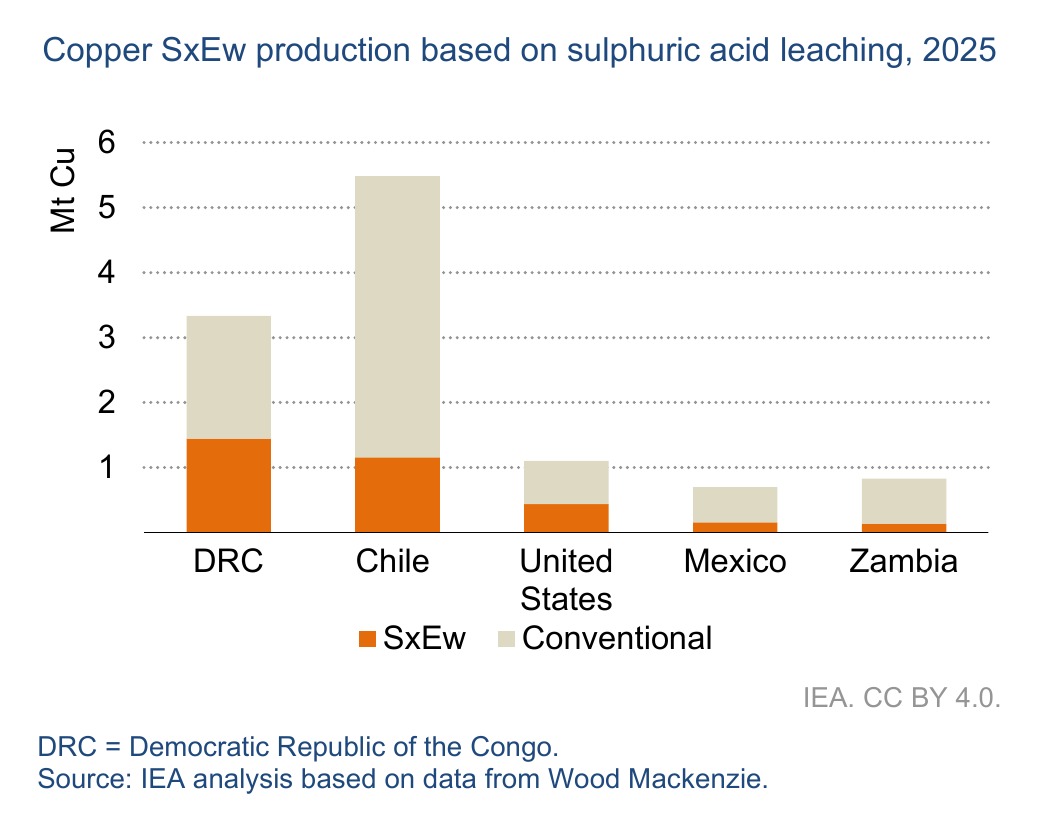

That matters for copper because over 15% of global primary output is produced via leaching, solvent extraction and electrowinning (SxEW) – a route that turns acid-leached ore directly into finished cathode at the mine site. The DRC, where almost 45% of copper production depends on sulphuric acid leaching, and Chile, already facing an acid supply crunch, are the most exposed, with roughly 1.5 million and 1.2 million tonnes of leached output respectively:

For an average SxEW facility acid accounts for 13% of costs, the IEA notes, but the figure rises to 20% in the DRC due to the higher carbonate content of the ore. Some producers’ sulphur or acid inventories are reportedly down to just 30-60 days, “with warnings of potential production cuts growing.” The agency does not mince words on what happens if the squeeze persists:

“At the global level, reduced acid availability from a prolonged acid ban or sustained high prices would result in global SxEW production curtailments, adding considerable supply stress to an already tight copper supply market.”

The acid shock lands on a market still nursing the wounds of 2025, when disruptions wiped out 1.5 million tonnes – over 6% of global mined supply – and tipped the refined market into deficit. Grasberg, hit by a deadly mudflow in September 2025, produced around half its 2024 volumes last year and is not expected to fully recover until 2028, while flooding at Kamoa-Kakula cut output by almost a third relative to guidance and leaves 2026 production below 2024 levels.

Copper prices, which topped $12,000 a tonne for the first time in December, went on to exceed $14,000 in May.

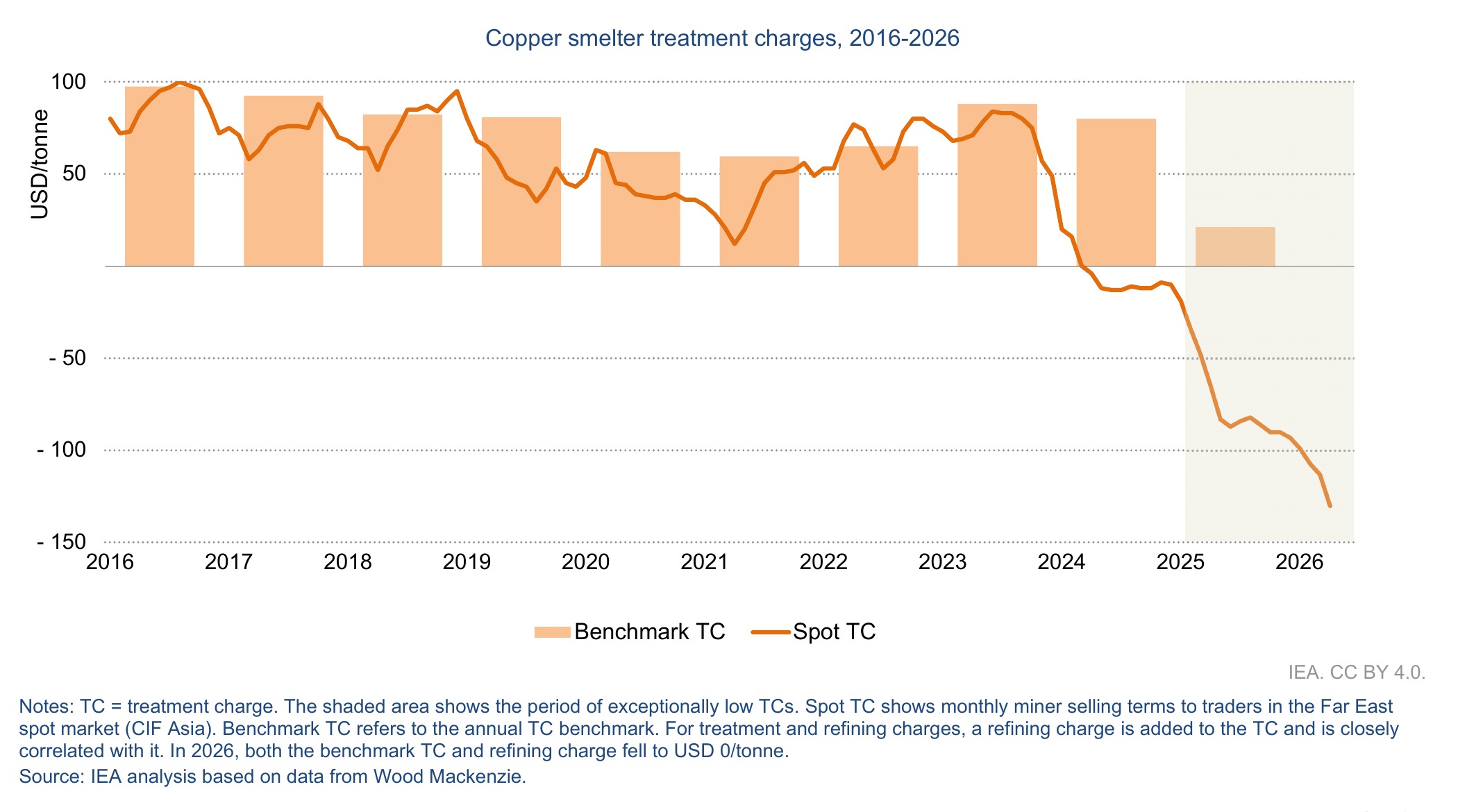

Zero fees, shrinking buffer

The strain is just as visible in the midstream. Despite record copper prices, the annual treatment charge benchmark settled at $0 per tonne for 2026 – the lowest ever agreed – while spot fees have been negative since 2024 and keep plumbing new depths:

A surge in Chinese smelter capacity is behind the collapse: China has accounted for over 90% of global smelter output growth since 2005, lifting its share from around 15% to half of world supply, and utilisation rates outside the country have sunk below 70% versus 85% inside.

China’s top smelters have agreed to cut production capacity by more than 10% this year and Beijing has halted around 2 million tonnes of planned new capacity, but the IEA says the cuts “are not enough to meaningfully balance the market” – and warns copper could follow nickel’s path, where oversupply drove production outside the dominant supplier out of business and concentration deepened:

“It is becoming increasingly crucial to pay close attention to growing midstream concentration risks in copper supply chains. Consideration may also need to be given to whether the current TC/RC framework remains fit for purpose in a changing market structure.”

The gap that won’t close

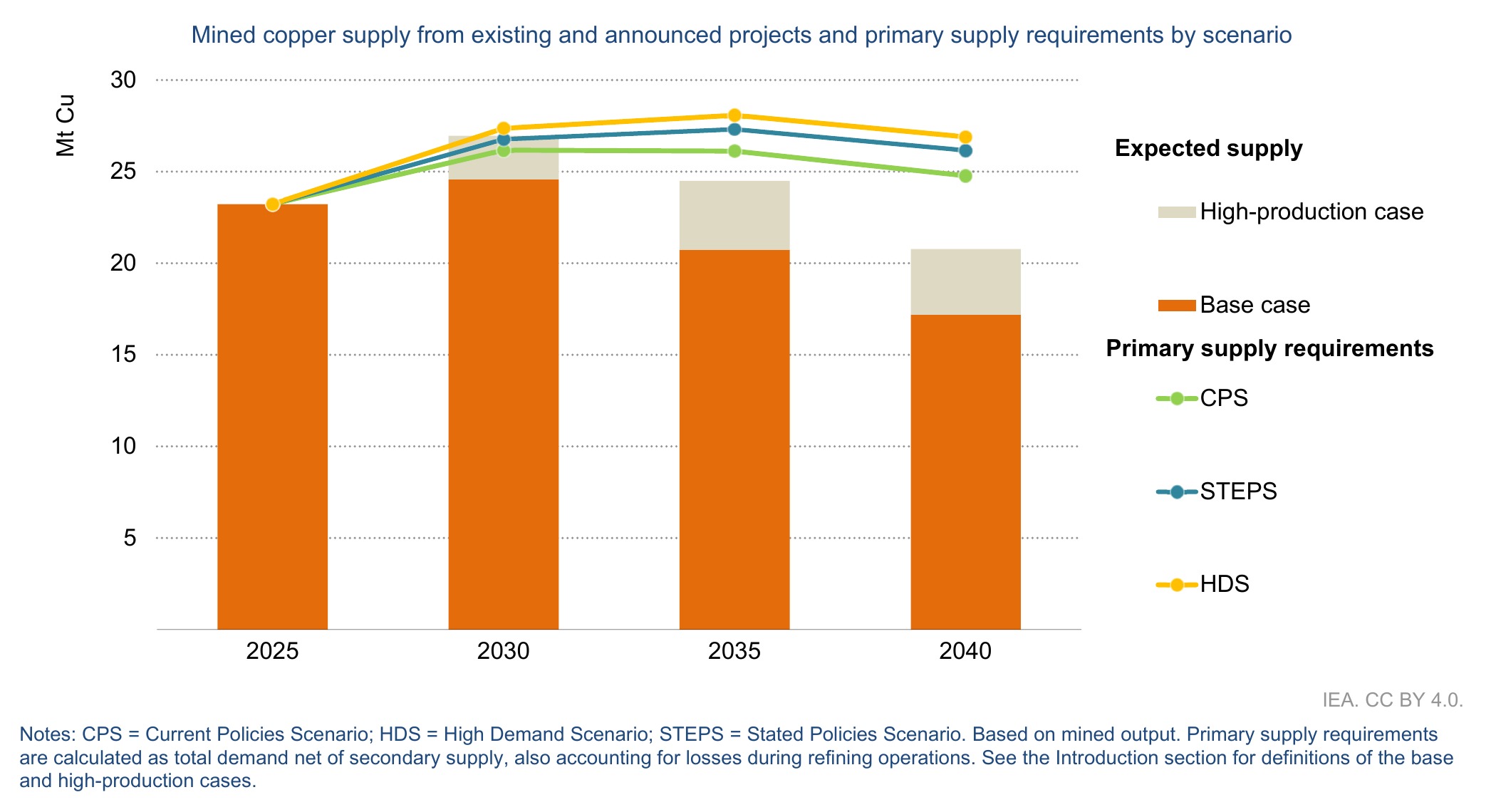

The long-term arithmetic has actually improved – just not by much. Based on the current project pipeline, the IEA projects primary copper supply will fall about 25% short of requirements in 2035 under today’s policy settings, narrower than the 30% gap in last year’s edition:

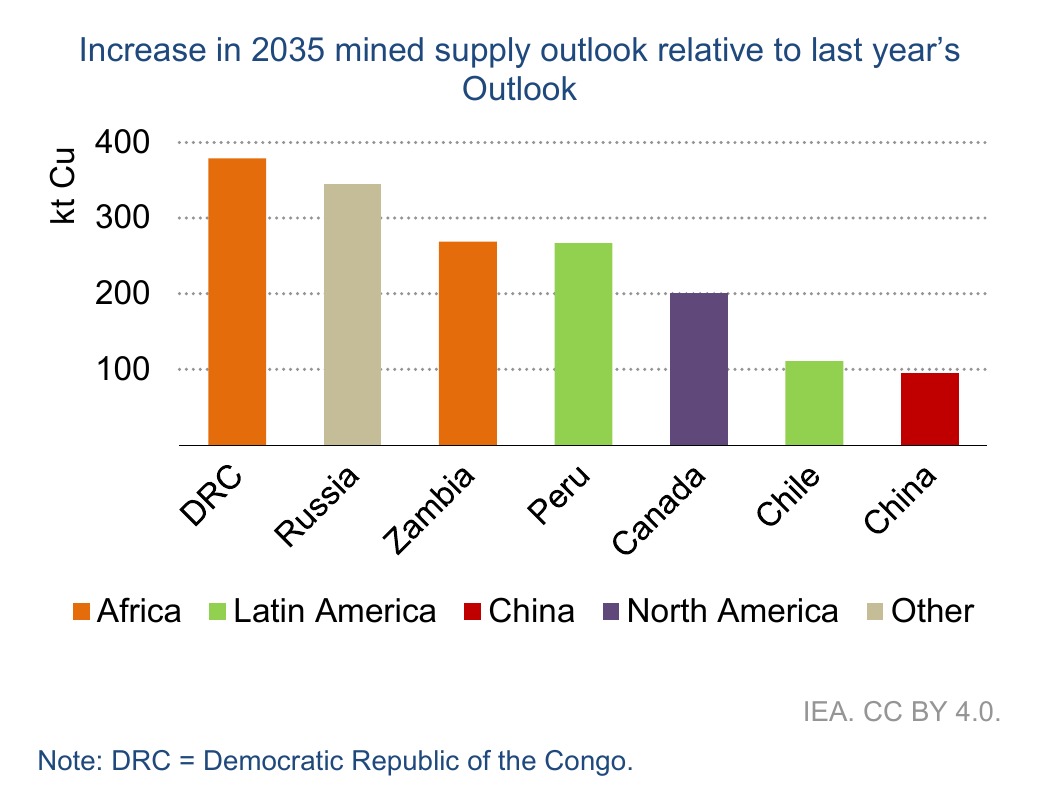

Africa accounts for most of the upgrade, with the DRC and Zambia together adding almost 650,000 tonnes to the 2035 outlook – helped by Chinese-backed Malachite ore operations, CMOC’s Kisanfu expansion and Barrick’s Lumwana expansion, where first production from the Super Pit is targeted for 2028.

Peru adds almost 300,000 tonnes through the Antamina life extension and Southern Copper’s Tia Maria SxEW project – though the IEA pointedly notes Tia Maria’s permit was revoked in April before being reauthorized 11 days later, “demonstrating the uncertainty and challenges in bringing major new copper projects online.” Russia’s Baimskaya could add almost 350,000 tonnes, and Canada contributes 200,000 tonnes via the life extension approval at Teck’s Highland Valley. The Resolution project in the US remains too tangled in legal proceedings to count in either supply case:

The forces keeping the gap open are familiar and getting worse. Average ore grades have fallen 40% since 1991, capital intensity for brownfield expansions has jumped 65% since 2020 to levels usually associated with greenfield builds, lead times run around 17 years from discovery to production, and only 5% of all copper deposits found in the past 35 years were discovered in the last decade.

Closing the gap carries the heaviest price tag of any mineral the IEA tracks: roughly $310 billion of the more than $750 billion in mining and refining investment needed through 2040.

Miners appear to have received the memo – while overall critical mineral investment fell 9% in 2025, spending by copper-focused companies rose 8%, and hunger for quality copper assets drove a 20% jump in global mining M&A value.

Copper price

The demand side of the IEA’s ledger explains why the market is willing to pay up: global refined copper consumption hit almost 28 million tonnes in 2025, up 3.7%, and is projected to grow by more than 25% by 2040 – around 7 million tonnes of new demand from grids, EVs and data centres – under the agency’s Stated Policies Scenario, with recycling only partly riding to the rescue.

Copper in New York traded at $6.32 per pound ($13,930 a tonne) on Thursday, holding near three-week highs, while LME cash copper, which started 2026 at $12,571 a tonne, settled at $13,537 on Wednesday – up nearly 8% year-to-date.

Forecasters remain split on whether the rally has run ahead of itself: BMI this week lifted its 2026 average to $12,700 a tonne with a $17,000 call for 2035, Macquarie sees $13,165 even while arguing prices are ahead of fundamentals, Goldman Sachs is holding at $12,650, UBS tops out at $13,000 by year-end and Chile’s Cochilco pegs 2026 at $12,235 – but on the IEA’s numbers, a market a quarter short of requirements by 2035 suggests the structural story is only getting started.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments