Aluminum industry faces big decarbonization challenges — report

A new report by Wood Mackenzie analyzes the challenges and opportunities that the future presents for aluminum, as the buildout of low-carbon energy supply and transmission will consume vast quantities of primary aluminum and associated alumina and bauxite.

Although such a forecast seems to be rosy, the market analyst says that the metal’s role in the green economy may be dampened by the fact that the industry will have to secure low-carbon power, which itself requires the use of low-carbon aluminium, among other metals.

“On a global basis, power accounted for close to 60% of greenhouse gas emissions relating to aluminum production in 2020,” the report reads, pointing out that the primary aluminum industry accounted for around 2.6% of global GHG emissions in 2020, of which 70% came from China.

In Wood Mackenzie’s view, decarbonizing power sources offers the greatest opportunity for emissions reduction in the aluminum industry.

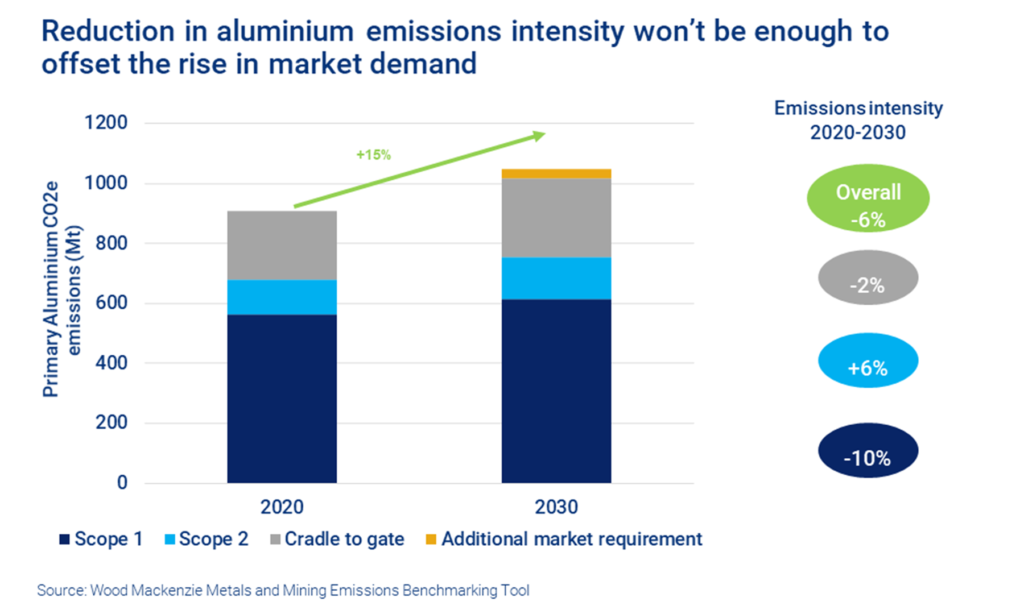

Since cradle-to-gate accounted for 22% of total primary aluminium GHG emissions, with coal accounting for 68% of the energy supply for refining, WoodMac believes that if the alumina refining industry were to switch to gas this would lead to a 26% reduction in emissions.

This is a particularly important solution given that aluminium’s Scope 2 emissions – direct emissions from purchased electricity – are set to rise over the coming decade, which reflects the concentration of expansion in Asia, where coal-based power sources will continue to dominate.

Conversely, Scope 1 emissions — direct emissions from owned or controlled sources — are expected to fall by 10% as producers introduce more efficient smelters into the global fleet, undertake limited switching of power sources, and drive carbon efficiencies.

Yet, when looked at as a whole, the industry’s emissions may rise by 15% in the next 10 years, bolstered by a significant expansion of primary production. This primary production would be driven in large part by energy transition needs.

“Our modelling indicates that, even with a willingness to build or procure low-carbon power and reduce process carbon emissions through inert anode technology, total industry emissions will rise by 15% over the next decade,” the review reads. “The grid will not be able to decarbonise fast enough to allow the aluminium industry to meet the needs of the energy transition while also cutting its emissions.”

According to WoodMac, even though a rapid expansion of recycled supply and use could offer a fast-track solution, given that secondary aluminum has 5% of the GHG emissions intensity of primary, in most of the electrical applications that are critical to the energy transition, secondary material cannot be used.

“The aluminum sector will be part of the problem of carbon emissions for the next decade,” says Julian Kettle, senior VP and vice-chair of metals and mining at Wood Mackenzie. “However, the optimist in me believes that ultimately it will be part of the solution by helping to deliver low carbon energy. But it’s going to take time, and when it comes to tackling the decarbonisation challenge, time is in short supply.”

More News

Vale chairman Stieler pushed out by pension fund

July 06, 2026 | 04:40 pm

South32’s Arizona $2 billion zinc and manganese mine to get US approval

July 06, 2026 | 04:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments