China’s Plenum promises cues for commodity bulls and bears

Chinese commodities markets entered the second half with a bearish tilt, raising expectations that next week’s big policy meet in Beijing will show how the government plans to approach problems around overcapacity and faltering demand.

The Third Plenum is typically a forum for longer-term political and economic reforms, and the general sense among observers is that major initiatives are unlikely this time around. But tweaks to the policy framework could still be consequential.

There’s a view that China is likely to provide more support for its economic recovery, but investors don’t have a clear idea of how raw materials-heavy it will be, said Paul Bloxham, HSBC Holdings Plc’s chief economist for global commodities. “We are watching and waiting to see what gets delivered in the property, infrastructure and manufacturing sectors,” he said.

China is the world’s biggest importer of commodities and its dominant supplier of clean energy, so decisions taken in Beijing ripple across the world. Policies that address the energy transition, President Xi Jinping’s “new productive forces” in high-tech industries, and unified national markets are likely to have a direct impact on commodities supply and demand. Other areas that could provide cues for bulls and bears alike include the housing crisis, tax and debt issues, and rural reform.

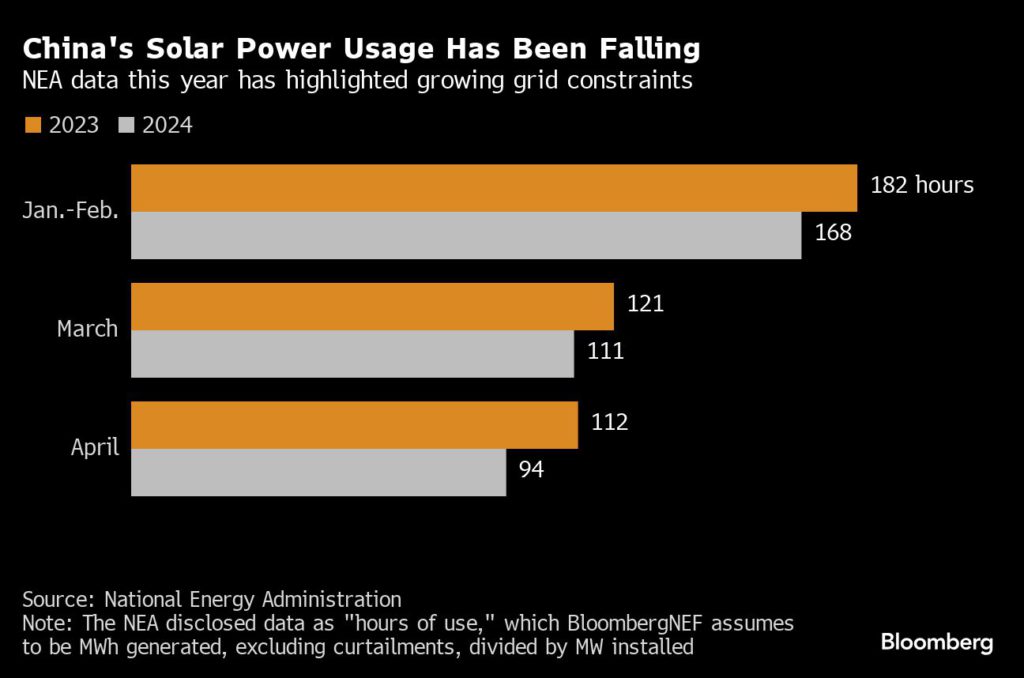

Solar

The solar sector is going through a rough patch. Excess capacity and fierce competition have pushed prices to record lows. At the same time, the grid is struggling to cope with all the electricity generated by China’s world-beating rollout of renewable energy. Solving the industry’s problems has become a leading priority for Beijing, which is counting on solar as one of the “new three” drivers of economic growth.

If the Plenum focuses on unifying China’s highly regional markets, then the electricity grid would be a great place to start. A lot of China’s solar power comes from mega-bases in the interior, far from the country’s major cities. Nationwide trading that allows clean power to be delivered to where it’s needed, based on market prices, would help solve the industry’s issues with bottlenecks and wastage.

That could mean more spending on grid connections, which would also help raise demand for metals like copper and aluminum.

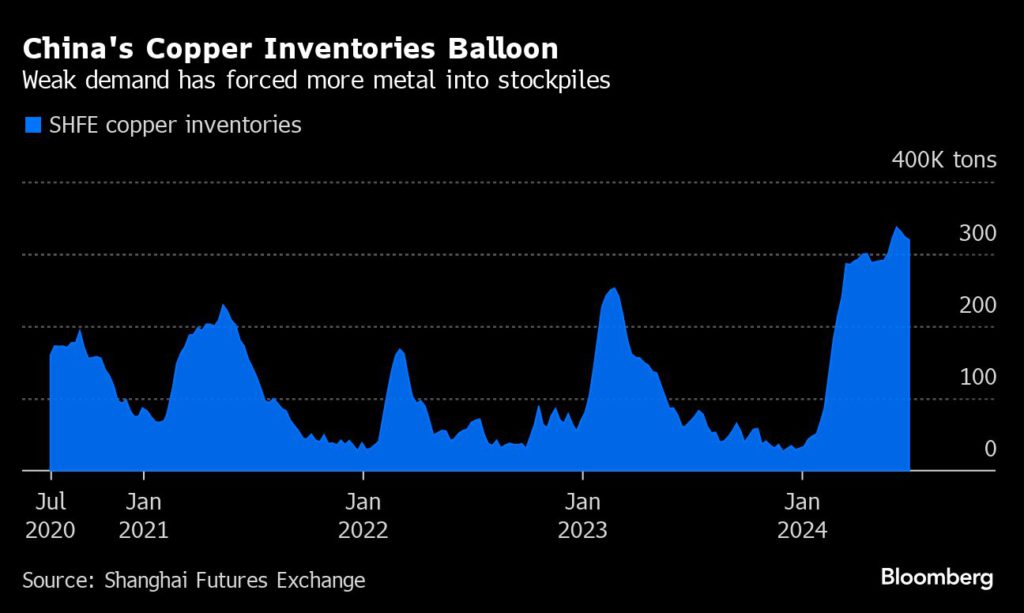

Copper

Copper has retreated from a record high in May after buyers in China balked at higher costs while the economy is gripped by factory deflation and a protracted property crisis. The pullback in prices has restore consumption to some degree. But to sustain that, the market may need to see more evidence that copper demand is central to Beijing’s plans to revive the economy.

Citigroup Inc. expects the Plenum to deliver greater support from investment in the grid and clean energy, as well as more help for the property market. For all of copper’s green credentials, housing is still a major source of consumption, including from the appliances that often accompany a home purchase.

Xi’s plan to nurture emerging tech-heavy industries that will help China pivot from the old economy to the new could also be a focus. In the transport sector, that means electric vehicles, for sure, said Li Xuezhi, head of Chaos Ternary Research Institute. But measures to foster growth in the so-called low-altitude economy – read drones and even flying cars — as well as more prosaic initiatives, like digital traffic management systems, would also boost demand for metals like copper and tin, he said.

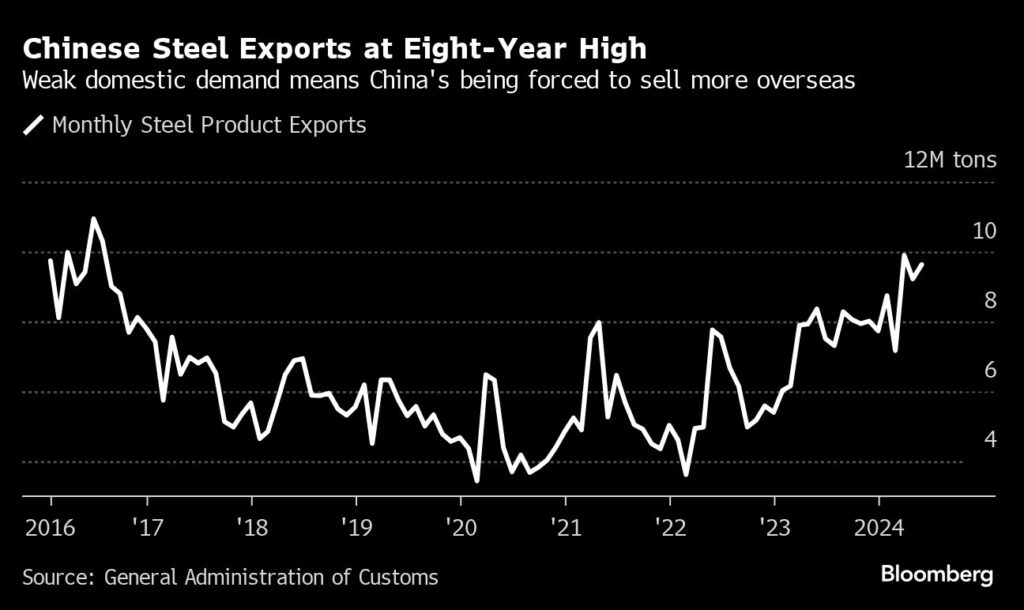

Steel

The steel market remains a bastion of the old economy and has taken one of the biggest hits from the nation’s real estate woes. Even more property support at the Plenum would hardly move the dial, because steel demand relies on new construction rather than cheaper mortgages or clearing unsold homes. And China simply doesn’t need as many houses as it used to.

But restructuring the country’s finances away from heavily indebted local authorities could deliver a win for the market, according to Vivek Dhar, an analyst at Commonwealth Bank of Australia. “A shift toward more central government debt and less local government debt opens up more spending potential,” he said.

That could mean more powder for state spending on public works — catnip to steel markets — although it must be said that Beijing has so far avoided the massive splurges that have characterized previous downturns. And infrastructure spending is becoming less steel intensive as the economy matures in any case.

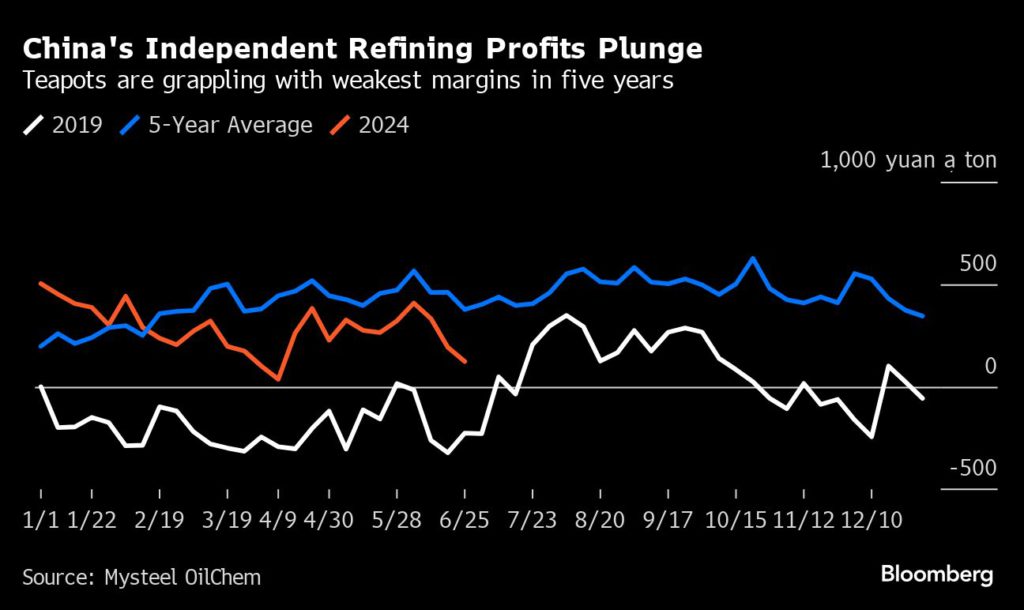

Oil refining

Few markets are as threatened by China’s swing to clean energy as crude oil. The nation’s rapid acceptance of EVs means demand in the world’s top importer may already have peaked. Further policy support for EVs won’t be popular among oil refiners staring at unprecedented overcapacity.

But the Plenum could have another nasty surprise under the bonnet. Beijing may be considering measures to raise funds by broadening the tax take, an unwelcome development for the shadier corners of the industry that have already drawn scrutiny over their tax affairs, said Amy Sun, a project manager at GL Consulting in Guangzhou.

China’s independent refiners, or teapots, have a history of skirting taxes to shore up their razor thin margins. About 40% of gasoline and diesel sold by teapots wasn’t properly taxed last year, according to research from China National Petroleum Corp., the nation’s biggest oil company.

Reform would “motivate local authorities to monitor tax compliance by the independent refiners, leaving limited space for tax evasion,” Sun said. That could crush profits even further in a sector that accounts for about a quarter of the nation’s oil processing. The upshot may be fewer teapots, according to Sun — and a solution of sorts to the nation’s capacity glut.

Grains

Rural reform and food security continue to top Beijing’s agenda. The long view is that, as vast as the country is, it doesn’t have enough farmland relative to the number of its citizens. China has just 7% of the world’s arable land but feeds about 20% of the global population, according to research from JPM Morgan Chase & Co., with any shortfalls made up by imports.

But there are short-term stresses that Beijing may need to address. Farmers have seen their incomes slump as ample supply combines with poor demand to weaken prices for staples like wheat and corn. At the same time, an increasingly erratic climate — in recent weeks there have been floods in the south and drought in the north — poses a longer term threat to domestic output, which could force the country to lean more heavily on imports.

Freeing up more arable land, giving farmers the financial backing to take advantage, and buttressing the country’s ability to swiftly recover from extreme weather events, could all be among measures announced at the Plenum.

More News

Canada unleashes wave of oil drilling permits in next big play

July 06, 2026 | 08:19 am

Congo sees no major threat from Middle East crisis to copper, cobalt output

July 06, 2026 | 07:30 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments