Australia expects sharp lithium price pullback in 2024

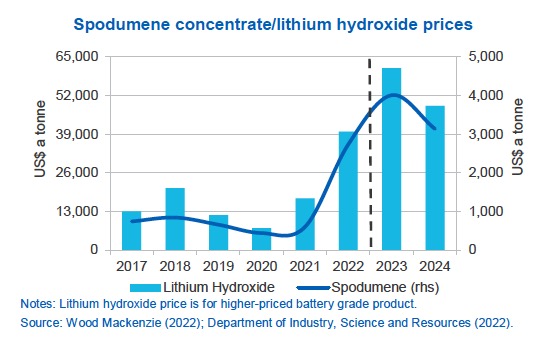

In its quarterly report released on Monday, the Australian government said it expects spodumene prices to rise from an average of $2,730 a tonne in 2022 (from just $598 in 2021) to average $4,010 a tonne in 2023 as record spot prices feed into contracts. However, 2024 will see a softening in the market to $3,130 in 2024.

Lithium hydroxide prices are set to follow a similar pattern and are expected to lift from $17,370 a tonne in 2021 to $39,900 in 2022 and $61,200 in 2023, moderating to an annual average of $48,500 in 2024.

Rapid price movements and the relative immaturity of the market will likely lead to ongoing uncertainty, according to the Department of Industry, Science and Resources, adding that should supply concerns ease prices could fall more quickly:

“While expansions to production are already underway in Australia and overseas, there are long lead times for lithium mine and brine operations. Moreover, the potential for delays in bringing such large volumes of lithium into production, mean risks remain of persistent supply shortages over the next few years.

“However, one of the drivers of recent high spot prices appears to be a push by refiners and battery makers to build up inventories, due to concerns about global supply chains. The lack of data on global lithium stocks makes it difficult to judge how well battery producers have built up stockpiles.

“If these concerns ease, prices could moderate more rapidly over the outlook period. Prices may also ease if global economic growth slows more sharply than the IMF has forecast.”

Production surge

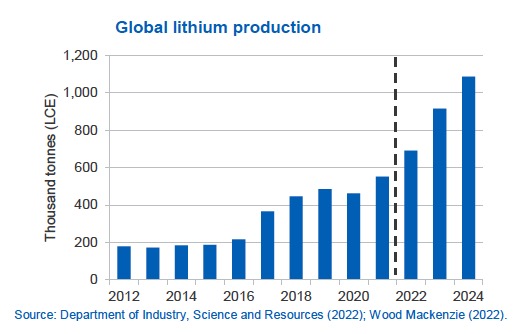

The Department expects global output to rise from 551,000 tonnes lithium carbon equivalent (LCE) in 2021, to an estimated 691,000 tonnes in 2022. Next year 915,000 tonnes are forecast, a 32% jump from 2022.

In 2024 production would climb above the 1m tonnes mark for the first time with Australia’s share coming to nearly half the global total at 470,000 tonnes, thanks to a pipeline of projects.

This includes the almost complete expansion of Mineral Resources and Ganfeng Lihtium’s Mt Marion mine, Liontown’s Kathleen Valley project which received a final investment in June and all major approvals in Q3 this year, and Core Lithium’s Finniss project near the city of Darwin where first concentrate production is expected in the first half of 2023.

The sharp production rise will also be boosted by expansions to SQM and Albemarle brine operations in Chile while state-owned copper miner Codelco is undertaking exploration in the Salar de Maricunga, with drilling due for completion early next year.

In Argentina, new and expanded brine operations by Allkem, Livent and Minera Exar will add to output Elsewhere. Piedmont Lithium has completed a pre-feasibility study for its Ewoyaa project in Ghana with first production expected late next year while European Lithium is progressing arrangements to secure additional capital to progress its Wolfsberg hard rock project located 270km south-west of Vienna, Austria.

Spot prices turn down

Last week spot Chinese lithium prices fell for the first time since May as uncertainty grows about demand in the world’s second-largest economy following the easing of covid-19 restrictions and the looming end to electric vehicle subsidies.

Lithium prices have defied predictions of a sharp pullback, however, and ex-works Chinese battery grade lithium hydroxide is still up 170% year-to-date averaging $81,000 a tonne during the first two weeks of December, according to Benchmark Mineral Intelligence. Lithium carbonate prices have followed a similar trajectory according to the London-headquartered battery supply chain and pricing specialists.

Benchmark data show spodumene prices up 257% this year averaging some $5,900 a tonne for 6% concentrate FOB Australia in November. Benchmark commented that spodumene contract pricing mechanisms tied to the lithium chemicals spot market had been successfully renegotiated, allowing for a shorter lag time for pricing movements in the chemicals market to be reflected in spodumene pricing.

More News

Northern Star replaces CEO, activist investor Elliott wants more

July 01, 2026 | 08:29 pm

Ukraine urges swift publication of Irish investigation into alumina exports

July 01, 2026 | 01:22 pm

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Christina Dian Parmionova

An important growth driver is its use in the batteries of electric vehicles. However, lithium is also used in the batteries of laptops and cell phones, as well as in the glass and ceramics industry.