Cuba’s cobalt exposes a Western supply chain weak spot

Canada’s only cobalt refinery has become an unexpected casualty of US sanctions on Cuba, exposing a critical weakness in Western mineral supply chains that extends well beyond geology.

The shutdown of Sherritt International’s refinery in Fort Saskatchewan, Alberta, illustrates how political and regulatory risks can disrupt strategic mineral processing even when facilities are located in allied countries, Patricio Faúndez of GEM Mining Consulting wrote in a recent research note.

The refinery depends on mixed sulphide precipitate produced at the Moa nickel-cobalt operation in eastern Cuba. Following a US executive order issued in May that broadened sanctions affecting Cuba’s metals and mining sectors, the refinery lost access to feedstock and will remain idle until production resumes at Moa.

The episode highlights how sanctions can ripple through banking, insurance, auditing and commercial relationships without directly targeting industrial assets.

“The case sends a warning signal to the West: mineral security does not depend only on having plants, technology or political allies, but also on having supply chains that are traceable, financeable and legally viable,” Faúndez wrote “Restrictions do not come only from the East. They can also emerge from within the Western regulatory architecture itself.”

The broader lesson extends beyond one refinery, the analyst said. Governments across North America and Europe have invested heavily in processing capacity to reduce dependence on China for critical minerals, yet refining plants remain vulnerable if they cannot secure legally compliant sources of raw materials.

The Fort Saskatchewan case, according to Faúndez, suggests that building refineries alone is insufficient unless governments also ensure stable, diversified and politically secure feedstock supplies.

Nickel-cobalt rich

Although Cuba attracts little attention in global mining, it holds one of the world’s more significant lateritic nickel-cobalt districts. Deposits around Moa, Nicaro, Mayarí and Holguín account for virtually all of the country’s strategic mineral importance. Unlike many undeveloped deposits, Moa combines mining with high-pressure acid leaching and produces mixed sulphide precipitate for refining in Canada, allowing Cuba to capture more value than exporting raw ore alone. A smaller zinc-lead-barite project at Castellanos demonstrates some additional mineral potential, but nickel and cobalt remain the country’s defining assets.

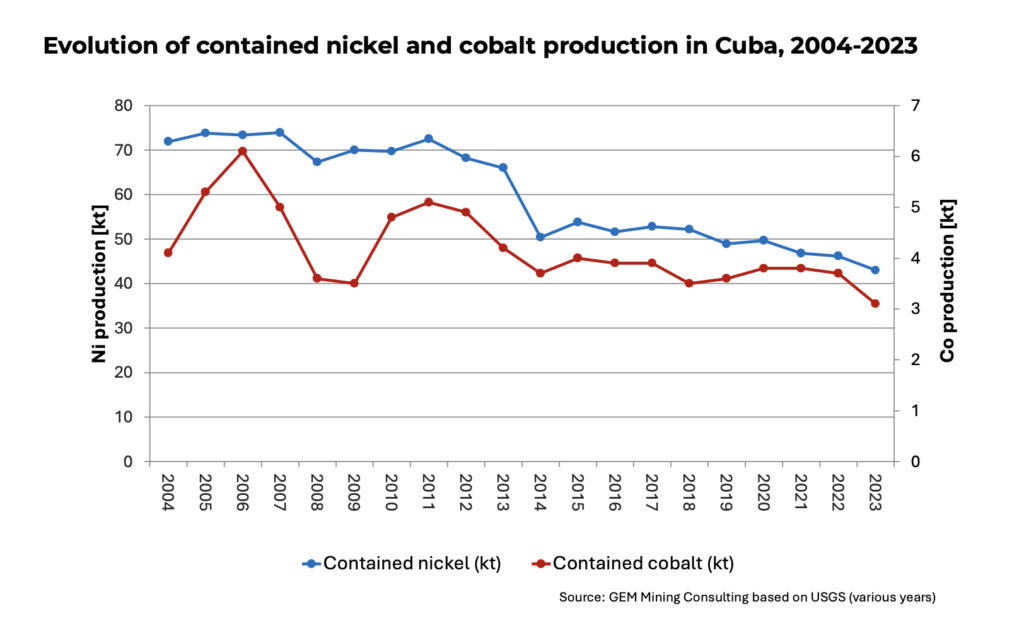

Cuba’s geological endowment has not translated into growing production. Nickel output held relatively steady between 2004 and 2013 before entering a prolonged decline, falling to about 43,000 tonnes by 2023. Cobalt production followed a similar path, dropping from peaks near 6,000 tonnes in the mid-2000s to roughly half that level. The trend reflects an industry with significant mineral resources but limited investment and expansion, leaving much of the country’s potential undeveloped. The production chart in the report shows both metals trending lower over the past decade despite sustained global demand for battery materials.

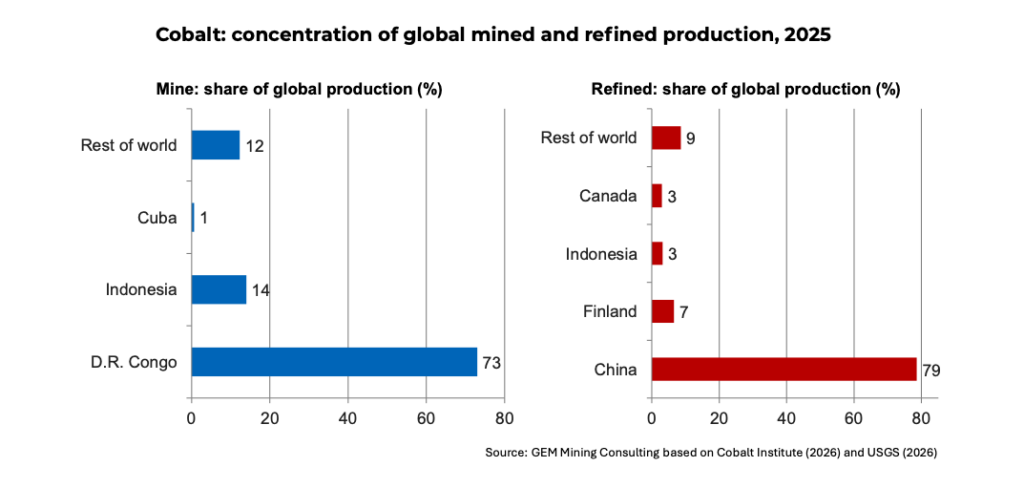

The report argues that cobalt presents a two-tier supply chain challenge. Mining remains heavily concentrated in the Democratic Republic of Congo and Indonesia, which together accounted for nearly 90% of global mine production in 2025. Refining, however, is even more concentrated. China produced almost 79% of the world’s refined cobalt last year, while Canada accounted for only about 3%.

That imbalance leaves Western governments with limited room to manoeuvre. The US, Canada and Australia together contribute only a small share of global cobalt mine supply, while North America’s refining capacity remains modest. The temporary closure of Fort Saskatchewan therefore represents more than a local industrial setback. It underscores how easily one of the West’s few refining facilities can be disrupted when upstream supply becomes politically or legally constrained.

Western wake-up

The report also challenges the prevailing assumption that critical mineral supply risks originate primarily from China or other geopolitical rivals. China has imposed export controls on several strategic minerals in recent years, while Indonesia continues to restrict exports of unprocessed nickel ore and the Democratic Republic of Congo has moved to manage cobalt exports through temporary bans and quotas. The Cuba case demonstrates that Western sanctions can create similar disruptions by making financing, insurance and commercial transactions increasingly difficult for companies linked to sanctioned jurisdictions.

For Cuba, the country’s lateritic nickel-cobalt deposits remain a strategic asset, but realizing their value will require more than favourable geology. Sanctions, weak economic conditions and limited infrastructure continue to constrain development.

Gem Consulting’s report estimates that if Cuba increased production to better reflect its estimated share of global reserves, the country’s economy could receive a meaningful boost.

For Western policymakers, the lesson is broader. Building new refineries and processing plants will not, on their own, secure critical mineral supply chains. Governments must also ensure access to diversified, legally secure sources of feedstock that can withstand geopolitical shocks and regulatory changes.

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments