Iron ore price correction delayed as global steel demand tops 2bn tonnes for first time ever

Iron ore prices climbed again on Friday to nearly $220 a tonne and back to within shouting distance of all time highs hit last month.

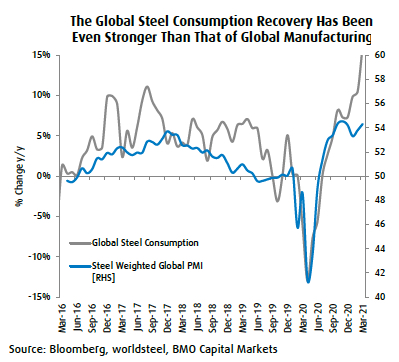

A new research note by investment bank BMO Capital Markets argues shifts in China’s steel industry, responsible for more than half of global crude output, will bring to an end a prolonged period of low margins and low capacity utilisation.

BMO points out that with global crude steel demand exceeding 2 billion tonnes for the first time ever and Beijing’s emissions curbs reportedly being extended into the second half of the year, Chinese exports will be significantly lower than in recent months:

With a robust global demand environment and very little spare hot-end capacity available to restart, we see an environment where global prices and industry margins remain well above through-cycle norms for the next 12-18 months at least.

Certainly, there is potential for ‘China annex’ steel capacity to be built, with China-funded carbon-heavy hot ends build in ASEAN and Africa shipping semi-finished product to China, but there will be a lag before these are up and running.

Market tightness will be most acute in the US with hot rolled coil prices already at all time highs near $1,600 a short tonne. BMO expects US HRC prices will remain well above historical averages this year and next although prices may cool slightly from today’s record levels in H2 2021.

While BMO upped its near term forecast iron ore by more than 25% from previous estimates, the bank still expects benchmark prices for the steelmaking raw material a full $100 a tonne below today’s by this time next year.

More News

Column: Battery metals recovery runs into stop-start EV market

Prices of lithium, cobalt and nickel have all recovered from their 2024-2025 lows.

July 05, 2026 | 10:09 am

Zimbabwe lab sees regional gold hunt accelerate as prices soar

July 03, 2026 | 11:49 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

2 Comments

ADERINTO TAIWO ADETUNJI

We are mining company in Nigeria,base on export of the minerals resources,such as iron ore both Magnetites and Heamatite,silica sand, Manganese Ore and others,we looking for reputable buyers globally, thanks.

Tony France

Is the world really looking to underground methods for extracting metallurgical coal.

The UK has a prime prospect but society cannot distinguish between thermal and metallurgical coals. Its a mind set.