Lithium price: Hydroxide back on top

The price for lithium hydroxide is once again trading at a premium over that of lithium carbonate following a period that saw the historical price relationship inverted, new analysis by London-based Benchmark Mineral Intelligence has found.

Hydroxide has typically traded above carbonate in the international and Chinese markets due to the chemical’s traditional production method of being a product processed from lithium carbonate, rather than directly produced from spodumene feedstock as is common in today’s market. Consequently, a conversion cost of $1,000 to $1,500 per tonne has historically been priced into hydroxide throughout the market’s history, BMI explains in a new blog post.

BMI says demand for lithium hydroxide continues to rise as production of high-nickel cathode cells ramps up

BMI says demand for lithium hydroxide continues to rise as production of high-nickel cathode cells ramps up. Chemical processors have also been preferentially sourcing hydroxide – where possible taking advantage of the comparatively cheaper chemical – boosting demand for hydroxide and reversing this short-lived discount to carbonate.

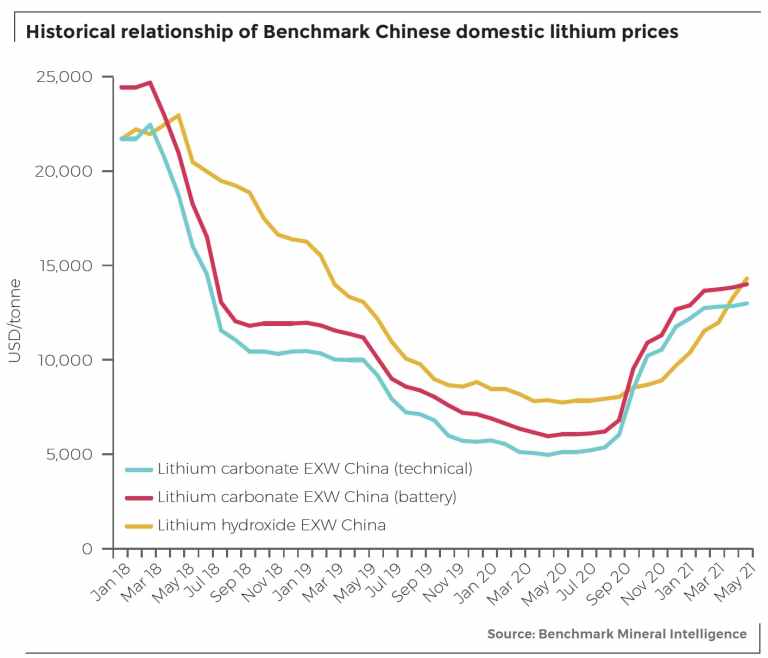

According to BMI’s May price assessment, Chinese domestic hydroxide prices sat at an average of $14,275 per tonne, compared with $12,950 per tonne and $13,975 per tonne, for technical and battery grade carbonate respectively, on an EXW China basis.

Demand for nickel-containing battery chemistries has gone from strength to strength in the year to date, according to BMI, with an average of 6.1 GWh of lithium nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminium cathode cells produced every month in China, compared with the two-year average across 2019 and 2020 of 4.3 GWh per month.

“Downstream demand from Japan and South Korea supports this notion, with lithium hydroxide exports out of China to the rest of Asia increasing by an average of 5% per month so far in 2021 compared to average monthly exports in 2020,” according to BMI.

Carbonate price increases have tailed off as the market holds off buying further inventory at elevated prices and added supply from Qinghai brine projects in China has begun to filter through to the market. As such, supply tightness is now being eased by additional carbonate supply, whereas the same is not happening for hydroxide, the analyst says.

Lithium prices set to soar

Looking forward, BMI is not so sure the historic price relationship between hydroxide and carbonate may be as clear cut as it has been in the past. The reason being is that newer Chinese conversion facilities are able to produce hydroxide directly from the rapidly expanding spodumene feedstock market, therefore removing some of the additional conversion cost by skipping the carbonate step and theoretically reducing the premium over carbonate.

Both hydroxide and carbonate prices are set to rise as the market tightens against surging battery demand

“Whilst there will always been a price relationship between the two chemicals due to their reliance on common feedstocks, the hydroxide premium may narrow over time, especially as newer Chinese conversion capacity is flexible and therefore able to favour the premium product and bring prices back to parity by adding additional supply to the market,” says BMI.

BMI forecasts NCM cathodes to represent over 75% of cathode market share by 2030, with well over half of these being the 811 high-nickel variety, meaning demand for lithium hydroxide is only set to rise further and challenge the already delicate supply-demand balance, supporting the analyst’s expectations of further rising prices in the Chinese domestic hydroxide market.

“Ultimately, whilst the higher price environment has started to incentivise supply investments, there is still a long way to go to meet the looming deficit that is already becoming evident in the market today,” says BMI. “As such, both hydroxide and carbonate prices are set to rise as the market tightens against surging battery demand.

{kind=link}

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments