Mining industry inertia will come at a price

Juniors have a mountain to climb to access exploration financing. Source: Rio Tinto Simandou

PwC’s John Gravelle on the mining industry’s austerity drive, price realities and declining exploration spending

The latest annual report by management consultants PwC about global trends in the mining industry shows just how sharp the decline has been.

Mine 2015 examines the 40 largest mining companies in the world and at just under $800 billion, their aggregate market value is now back to 2005 levels and half of what it was four short years ago.

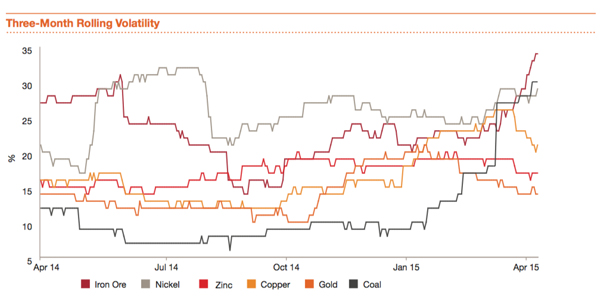

The report titled The gloves are off also notes that despite a relatively stable gold market, 2014 was another year of heightened price volatility. It warns the stormy conditions in the sector may only intensify as supply and demand are knocked more out of kilter.

John Gravelle, global mining industry leader for PwC, tells MINING.com current weakness is probably more of a supply issue than a demand one, with many of the Tier 1 assets bought when the going was good now coming on stream.

Apart from a resurgence in demand – not expected in the short term – the only thing that could see prices spike is if more production comes off line, says Gravelle, adding that the realities of the current environment has now set in for executives and boards.

John Gravelle: PwC Global Mining Leader

“Mining companies are now making decisions on where prices are now. They no longer consider, as they were a couple of years ago, the drops to be temporary and that prices are simply going to rebound 25% next year. If and when they do go up we’ll be happy to increase margins, but in the meantime we’ll make sure we can operate profitably at current price levels,” says Gravelle.

Miners’ cost-cutting efforts were helped by falling oil prices and weakening local currencies last year, but much of those saving have been realized. Last year the top 40 miners by market cap lowered operating costs by 5% despite increasing production.

There’s definitely more cost cutting to come and companies are having to innovate to find ways to do so, says Gravelle citing the examples of smaller players able to squeeze more out of the divested assets of majors: “If it’s their only assets they get really focused and find new ways to save. ”

Asset impairment charges were cut in half in 2014 from 2013’s record tally but at $27 billion writedowns are certainly still eye-watering. As for a new wave of spending, that’s not going to happen any time soon.

Source: PwC

Source: PwC

Source: PwC

“Shareholders are just not letting companies do the big acquisitions. The mining companies would like to do the groundwork in order to take advantage of the next upswing, but the reality is that shareholders still remember those big write-offs.

“They’re saying let’s not go back there again – show us you can operate profitably with what you have. Once they’ve proven that to the market, that’s when they start looking at the next opportunities. But, were just not there yet.”

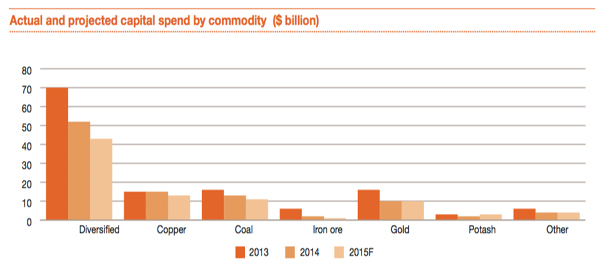

The top 40 companies slashed capital spending 20% in 2014, with most shying away from greenfield projects, focussing on a handful of tier-one projects or developing smaller brownfield assets.

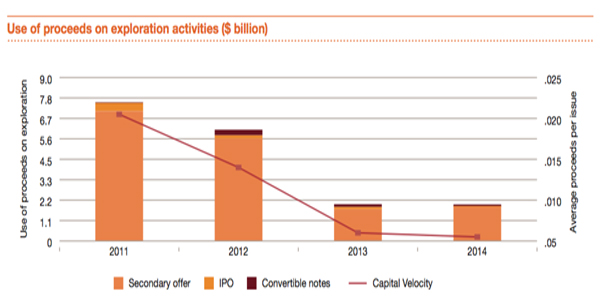

Nowhere is shift away from an investment and growth mindset to austerity and shareholder returns more visible than in exploration budgets.

Over the last two years, the majors cut back their exploration spending by more than half to a “miserly” $4.9 billion in 2014. That’s down from the $6.3 billion allocated in 2013 and $12 billion in 2012.

The report notes that the smaller exploration budgets at the 40 largest companies isn’t in itself a reason for concern for the long-term sustainability of the industry – the concern comes from the increasing difficulty of junior miners to raise capital targeted for greenfield exploration activities.

And that won’t change unless the mid-tier and top producers start attracting capital back to the sector first, says Gravelle:

“You need to get investors excited about the mining industry overall. Once the mid-tier and major producing companies can show sustained profitability that’s when you get some excitement back in the sector.

“The money will flow into low risk companies first. There’s always going to be the investor that wants to get in early, but the junior market would only really start to benefit once producers have instilled investor confidence. And that may take a couple of years.”

The industry’s inertia on exploration will come at a price PwC says in the report. If reserve levels continue to decrease, it may further exacerbate the demand and supply volatility witnessed in recent years.

The reductions in capital raised and spent on exploration also call into questions miners’ ability to respond to eventual increases in commodity demand. A generous interpretation of current industry conditions and lack of ambition is that it is setting the stage for the next supercycle.

And while it’s definitely a long term expectation and many factors would have to fall into place to make it happen, Gravelle believes three major trends will lead to a resurgence in demand:

Successful structural reforms in China, rapid Indian urbanization and infrastructure investment growth and the building of a new Silk Road which would dwarf even what China achieved over the last decade in terms of its impact on mining.

More News

BHP seeks to restart Cerro Colorado mine with $1.5B investment

The copper mine has been closed since late 2023 after it was denied its water permit.

July 02, 2026 | 10:43 am

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

4 Comments

Robert S. Stewart

If you believe in 60,000 foot altitude observations dished out by the folks who helped to bring about the biggest meltdowns in the global economy, of which the mining industry was but one victim and assailant, then swallow this codswallop. People who work at accounting firms, like the accountants who work in the mining industry, like the lawyers who work in governments, like the brokers who work on the stock exchanges, not one of these fools is involved in the supply chain between producers and consumers.

They are mere promoters of OPM, “Other People’s Money”, of which they dish out and swallow misinformation with ample delight. If anyone of these people actually produced a piece of machinery, built a mine, mill or smelter, extracted ore from the Earth, loaded it onto a form of transport to a market, converted the mineral into a metal and thence into a machine, and sold it into the global market, they would know that analyses like these aren’t worth the time of day to write or read them.

It is like listening to some jackass on the radio saying “The Earthquake in the Andes caused a rise in the price of gold today”. Or worse, read a press release at the conclusion of a G7 Conference that as written before it started (saying nothing), and equate that back to the job security you hold working in a gold mine in Uzbekistan.

Pretend a doctor diagnosing a patient on the basis of remembering a symptom he might have learned in medical school forty years ago. Without asking a single question of how the condition started fro the patient, he pulls out the prescription pad and slaps on an anti-biotic that is sure to make you dizzy, miss the targeted virus, and cost you $100 for doing nothing. He will have pocketed 20%, the drug manufacturer made $50, and the distributors and transporters all the rest. What about the patient?

What about the investors who willingly walk up to the Cliff of a steep valley and are told, “buy this stock because of these global conditions?” It sounds good, so the sheep jump off the cliff and throw their money at all the accountants, brokers lawyers, huckters, promoters and analysts who couldn’t tell you how bauxite is turned into an aircraft. Some of them run mines, others run aircraft manufacturing corporations. What happened to the miners?

They have mainly disappeared from the scene, except for those few who continue to toil with the canaries at the bottom of the mine shafts. However, their bosses are now the accountants and CEO’s without mining backgrounds who are juggling the stock price to figure out where to make their profits.

Investors have all since learned that the entire swindle over raising funds to build mines, didn’t just start with Bre-Ex. It started when these so-called “professional manipulators” of evaluating a mineral prospect, a mine, a production schedule, a supply chain or production and consumption, and a global market place got disconnected, one from the other.

Anti-competition laws, insider trading, lies passed on from one accountant to another, from CEO to CEO, from lawyer to lawyer, bamboozled the markets with strategic mis-information that led everything to implode and destroy the confidence that everyone once had in orderly markets. The juniors were inundated by fraudsters out to make a fast buck. The mid-tiers were ousted chiefs of former majors, trying desperately to get back into a sound market. The majors decided to swallow up everyone and tried to control all the sectors, by squeezing the start-up’s with low commodity prices, flooding markets with products on which the mid-tiers couldn’t compete, and now overproducing to the point of farcical explanations about lowering the cost of production. Soon they will all be working driver-less trucks and miners will only be found in museums.

This is nothing more than finding an alternative method of hosing the fools who are investors into thinking they are moving out of the 16th Century and into the 21st on improved and more efficient mines. Nothing could be further than the truth. If you can read the balance sheets of any of these fools, you’d know how far-fetched their analysis is. Who said China is slowing down? Who said India is far behind the West? Who said South America is stuck in their mud?

If miners worked their 24/7/365 shifts and brought their ores to the surface in harmony with those in their communities, and others ventured across the Earth to study the needs of others, newer methods to mine the minerals, transport them to markets as metals and invent new means of production and consumption would have been sorted out long ago. That process stopped many decades ago, and nothing new, really new, has been brought into play for a long time, except maybe these driver-less trucks.

The blind leading the blind is what we have today. Miners are being led by accountants who think they understand mining. Governments are led by bureaucrats who think they understand raw material production and employment. Did any ever work in a mine? The Courts are run by lawyers who simply milk the system of pulling the tea cosies over their clients’ heads and running away with the profits of the industry.

Mining is in crisis because the leadership ran out of control a few years ago and turned the industry on its head. Fools disguised as miners milked the entire industry of all its profits and stuffed them into their pockets, ably aided by the accountants and brokers, and egged on by the governments to milk excess profits from false accounting.

Investors lost touch with how the world works, and relied on the grotesquely false information spewed out every day in the media by those who would profit from it, and left the investors with nothing to show for their hard-earned pensions, their decades of toil, and the false promises of “good or better days to come”.

The industry will never correct itself until miners retake control over their industries and quietly bring in the strategic reforms to improve efficiencies. Those are technological improvements, not accounting, legal, promotional or political changes.

ExPat

“when the going was good” the miners spent like drunken sailors, taking on questionable projects, ignoring geopolitical risks and awarding their (often incompetent) executives hugely generous pay packages. Now many of these mining companies are paying the price for their 2010-2012 spree. The painful throbbing hangover will last a few more years (at least). But no one should expect that the miners will be any smarter coming out of this experience – They will do the same thing again next time there is a cyclical peak in demand.

Chat.CEO.ca for real time news

So the thesis for the next bull market is structural reform in China, rapid Indian urbanization and infrastructure investment growth. Did he read My Electrician Drives a Porsche? and reverberate Gianni Kovaciviec? See what people are saying about CopperBank and sign up for free insider trades at chat.ceo.ca/CBK and check out chat.ceo.ca for general discussion amongst professional investors in mining

schnabel

With non technical CEO lawyers and accountants running the companies the write downs are no surprise. The technical staff is stuck pretending that the company can actually mine a resource that is 20 Mt of 1.3 g/t gold on the top of some remote mountain or similar. You can’t make a solid case for even the operating costs let alone the capital investment but the consultants of the world still play along knowing they are out of a job as soon as the inputs result in a project below the return threshold – say 15%. To make it worse they use unrealistic commodity price projections but -hey- who’s to say what’s realistic. RESULT – cost overruns and write downs that even the biggest companies cannot finance. No wonder investors/shareholders don’t want to invest. They push for growth but they get projects with unrealistic assumptions. The management and board either don’t realize the folly because they are lawyers and accountants or the techies among them let it go as long as possible to collect handsome paychecks, perhaps even with golden parachutes.

What’s killing mining is the promotion of uneconomic projects to enrich a few execs. We may have 43-101s and other optically beautiful “safeguards” but it seems that if you recognize a bad project you dare not say anything or you’re “not a team player”. Instead it is promoted for years and, if the money can be raised, even developed before financial disaster strikes.