Nickel, cobalt prices benefit as electric car action shifts to Europe

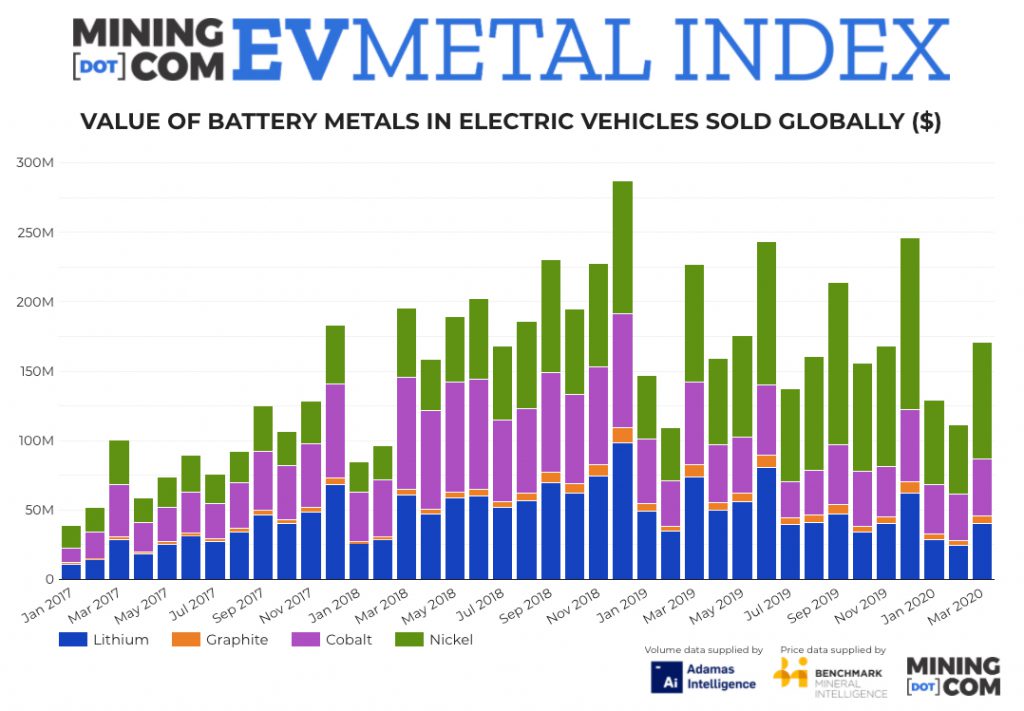

MINING.COM EV Metal Index tracking value of battery metals in newly-sold EVs globally rebound as nickel and cobalt-rich batteries favoured in the EU and US gain traction.

While electric car sales were crashing in China, the world’s largest EV market by a country mile, customers were still busy kicking tires in Western Europe.

Year to date sales of battery-powered vehicles in the world’s second-largest car market surged 37% compared to last year to 142,000 units, according to Schmidt, a market researcher.

Preliminary data from Schmidt show EVs made up 6.7% of total car sales on the continent in April – in countries like Norway seven out of 10 new cars sold are now electric (mostly thanks to radical incentives – you even pay half-price for ferry rides and until recently, free parking anywhere). In the UK it was one in three.

Total auto sales in Europe (excluding the UK) fell by 80% with cities under lockdown. EU EV sales dropped by a comparatively healthy 30% last month.

Sales in China also slumped by almost a third during April, but that figure constitutes a bounce-back – sales of electric cars slumped 80% compared to 2019 the month before.

Tesla’s boss may be running afoul of the law, but its mass-market Model 3 continues to find buyers (despite a mysterious 64% drop in sales in China and unexplained closure of its new Shanghai factory even as covid-19 wanes in the country), not least in Europe where the Model 3 tops the charts. And with the first Model Ys being delivered, the EV pioneer looks set have a much better year than its ICE rivals.

Upstream, the news is not quite so rosy.

Benchmark Mineral Intelligence, a battery supply chain pricing agency and megafactory tracker, shows a deteriorating market.

Prices for the raw materials tracked by the MINING.COM EV Metal Index are all down: The price of lithium dropped 40% year-on-year in March, cobalt (–15%), nickel (–2.4%) and graphite (–26.2%).

That leaves the volumes of raw material in batteries of newly sold EVs to do the heavy lifting in the index.

Indeed, data from Adamas Intelligence which tracks passenger EV and hybrid registrations (and the metals contained in their batteries) around the world, shows deployment of lithium (down just 2.7% in Q1 on a year-on-year basis), cobalt (+0.5%) and graphite (–1.3%) holding up. The tonnes of nickel in EVs joining the global car parc jumped by 10.4%.

Overall, the value of battery metals in electric cars sold globally reached $411 million during the first quarter, a drop of 14.7% compared to the same period in 2019, a record year.

Nickel rich, unthrifty cobalt

European carmakers favour higher energy density, longer-range NCM (nickel-cobalt-manganese) cathodes, which together with Tesla’s NCA (nickel-cobalt-aluminum) technology account for over 90% of batteries in passenger EVs.

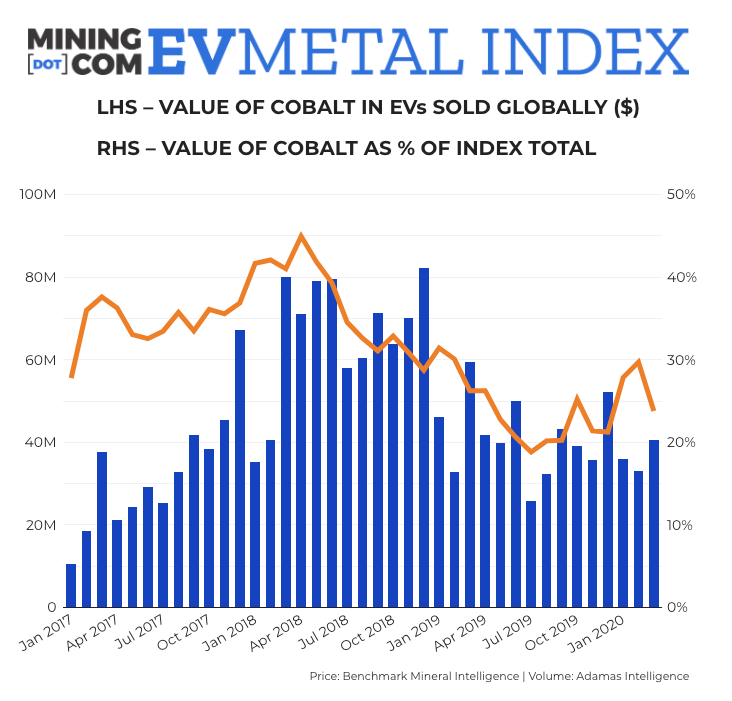

Despite further falls in the cobalt price in March, the EV Cobalt Subindex is down just over 20% in the first quarter of 2020 compared to the same three months last year.

Consider that cobalt entering the battery supply chain was trading within shouting distance of $50,000 per tonne this time last year, but has since slumped to the low $30,000s.

And on top of price declines, automakers continue to thrift the use of cobalt – by far the priciest raw material – in cathodes. While NCM111 (equal parts nickel, cobalt, magnesium) are being phased out in the latest models, cobalt is proving a sticky component of cathodes.

Ingolstadt vs Fremont

For example, the only electric car competing with Tesla at the luxury end in terms of volume is Audi’s e-tron.

Adamas Intelligence head of data and analytics, Alla Kolesnikova, explains that with a battery capacity of 95kWh and a NCM622 battery, the 55 Quattro, uses more than three times the amount of cobalt than Tesla’s Model 3 in the US.

In turn, the 75 kWh Performance AWD Model 3 sold in the US with an NCA battery (Tesla claims less than 1 part cobalt and around 9 parts nickel for its batteries) and the made-in China 56kWh NCM811 version, translates to 20%–30% more nickel per unit of battery capacity than the Audi.

Nickel-rich cathode chemistries like NCM811 now boasts a 9% market share worldwide from less than 2% a year ago and in China in March it captured almost a third of the market based on total battery capacity deployed, according to the Adamas battery capacity tracker.

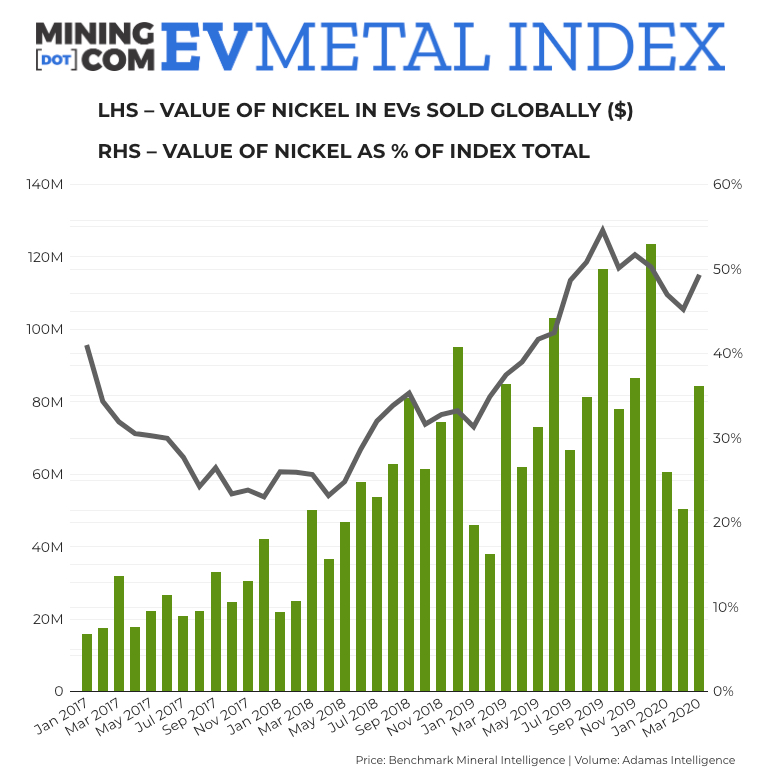

The Nickel Subindex overcame the price slump entirely with the value of nickel in batteries of newly-sold EVs around the world increasing by 15.6% in the first quarter versus Q1 2019.

That’s thanks to a 77% surge in deployment to over 6,000 tonnes in March, making up for a nickel sulphate price down 30% from its peak above $4,400 a tonne in September.

Outlook

Recovery in the Chinese auto market looks increasingly V-shaped.

An abrupt change to incentives mid-2019 knee-capped the EV market in China, but Beijing has since brought certainty to the subsidy regime for what it terms new energy vehicles (NEVs). Some provinces have instituted their own schemes and auto manufacturing is destined to be a favoured recipient of stimulus to kickstart China’s post-covid recovery.

In the US and Europe, EVs may escape the worst of the overall auto downturn, which even before the pandemic looked set for a dismal year. Europe’s green car incentives remain generous and a cash-for-clunkers program favouring EVs may well be on the cards.

Raw material prices, however, are destined for more distress.

Lithium prices look most vulnerable with covid-19 disruptions in major producing countries Chile, Argentina and Australia doing little to alleviate global oversupply.

Benchmark lowered its lithium demand projections by 9% to just under 316,000 tonnes on the back of a slowdown in battery manufacture and traditional end markets including glass, ceramics, and lubricants.

Benchmark’s covid-19 impact assessment lowered its 2020 demand projections for cobalt by 8.6% to 121,000 tonnes with a declining and small market surplus to end-2022.

Graphite forecast was lowered by 10.2% to 749,000 tonnes with the market deficit emerging only in 2023 from an earlier estimate of undersupply next year.

Nickel sulphate demand is expected to reach 169,000 tonnes this year and the market to remain in surplus through 2023, despite further delays to projects in Indonesia producing nickel suitable for the battery market.

The London-HQed company lowered its expected EV penetration rate for this year to 2.7% from 3.1%. That’s the equivalent of 550,000 fewer units in 2020 than previous projections.

Simon Moores, Managing Director of Benchmark Mineral Intelligence will present the keynote: The Global Battery Arms Race: What Next? at the company’s online EV Supply Chain Festival.

The sessions are free, dates are: World Tour East, Tuesday 26 May, 8am London and World Tour West, Wednesday 27 May, 4pm London.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments