One week – 23 tonnes: What next for world’s top gold ETF

On Thursday, gold regained some of its footing after 10 straight down days that saw it reach the lowest levels since March 2010.

Futures contracts in New York with August delivery dates closed at $1,094.10 an ounce, up a couple of dollars from yesterday’s close, bringing to an end the metal’s worst losing streak since 1996.

Gold’s gap down this week has been blamed on large investors like hedge funds using dubious trading strategies to knock out gold bulls, more so than on any change in fundamentals.

But that has not stopped spooked retail investors from exiting the market in droves, pulling millions of ounces from once popular gold-backed exchange traded funds.

Top physical gold-backed ETF – SPDR Gold Shares (NYSEARCA: GLD) – suffered outflows of 2.7 tonnes on Thursday, bringing the tally since Wednesday last week to more than than 23 tonnes or $2.1 billion worth of bullion.

Once the largest ETF in the world, in June GLD dropped out of the top ten and with the latest outflows total assets under management has declined to $24.1 billion, more than $50 billion below its 2011 peak.

GLD dwarfs other physically-backed exchange traded gold products holding more than 40% of the global total at 684.6 tonnes or 22m ounces.

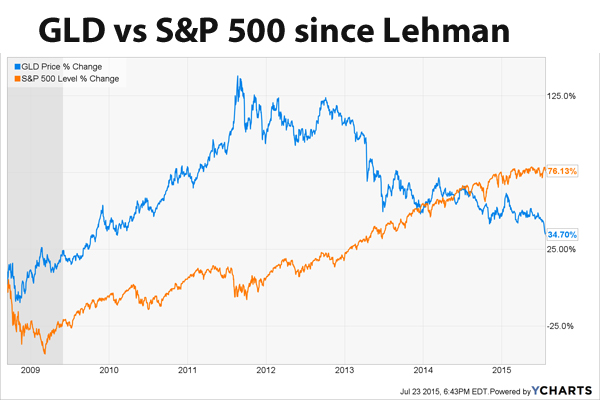

Holdings have now fallen to the the lowest since 19 September 2008. The collapse of Wall Street investment bank Lehman Brothers sparked the global financial crisis occurred September 15 that year.

GLD buyers would snap up 141 tonnes before the end of that month as investors around the world scrambled for a safe haven.

But now that in the words of Federal Reserve Chair Janet Yellen, the US has now made substantial progress in “healing from the trauma of the financial crisis” GLD is seeking a new role.

Industry website ETF.com recently asked Will Rhind, chief executive officer of the World Gold Council, given that the “crisis premium” is fading what gold and GLD could do for investor portfolios:

ETF.com: Let’s talk about GLD. Help me frame GLD for the post-QE world—what is GLD’s place over the long haul?

Rhind: Taking a step back, the gold market, like a lot of commodity markets, is cyclical in nature. We had 10 years of a bull market for gold prices in terms of rising emerging market demand. It was a principal catalyst, and then it was supercharged by the financial crisis. And now we’re in a period where that price has come off the last few years, and we’re in a tougher period for the gold market.

Looking forward, GLD is a fund, but it’s also a franchise. It’s still the marquee product for an investment in gold. It’s still the largest physical gold fund in the world. But demand for GLD, like gold, is cyclical too. So while we certainly believe GLD has a place in any diversified portfolio, there are a lot of investors who look at gold through a very cyclical lens and who either have a very low allocation to gold right now or no allocation.

As risk or attitude to risk changes in the market—as we hopefully get a rate rise that perhaps signals the final end of the bull market in bonds, and a start of an asset-allocation shift out of fixed income into other asset classes—we think gold will be a beneficiary of that, as people look to move assets out of bonds.

ETF.com: Are you talking about an “equitization of cash” of sorts that’s also a way to soldier through this volatile transition period of rising rates?

Rhind: It’s more of a reshuffling of the asset allocation in a portfolio. So if somebody has no allocation to gold—let’s just say for argument’s sake that somebody has an equity portfolio, 60/40 bonds and equities, and we get into a rising-interest-rate environment.

That’s not going to be positive for bonds, and while I’m not suggesting people are going to sell all their bond portfolio, they maybe cut that from 40 to 35, or from 40 to 30. And what’s the beneficiary of that 5 or 10 percent in terms of reallocated, reweighted assets? We would like to think gold could be a beneficiary of some or all of that reallocation.

Number one for a day (or two)

Gold ETFs were credited for a big portion of gold’s uninterrupted 12-year bull run, because ETFs make it so easy to invest in the yellow metal. (And to cash out as gold’s 2013 annus horribilis so clearly showed.)

While launched a full 18 months after the first physically backed gold ETF was created in Australia, GLD quickly dominated the market.

GLD was listed on 18 November 2004 and enjoyed a pretty good first day. Investors bought just over 8 tonnes or 260,000 ounces of gold affording the fund a net asset value of $115 million.

A mere two days later it would cross the $1 billion mark and by the time Thanksgiving arrived the following week gold bugs had snapped up more than 100 tonnes. The 1,000 tonne market would be crossed in February 2009.

On August 22, 2011 when gold was hitting record highs above $1,900 an ounce GLD became the largest ETF in the world briefly surpassing the venerable SPDR S&P 500 trust (assets today equal $180 billion) at a net asset value of $77.5 billion.

Gold holdings in the trust would peak more than a year later in December 2012 at 1,353 tonnes or 43.5 million ounces, representing half the ETF gold held around the world.

Global ETFs hit a record 2,632 tonnes or 93 million ounces of gold at the time.

All of that came crashing down in 2013 as the gold price plummeted and investors pulled 552 tonnes from the fund. The extent of the panic was evident by the fact that GLD had only 17 days of inflows during the entire year.

After a few false dawns in 2014 GLD recored a second year of net redemptions. Before the carnage of this week GLD was in positive territory for 2015.

More News

{{ commodity.name }}

{{ post.title }}

{{ post.date }}

Comments

Matt

ETF’s were a disaster in the Oil and Gas market and will be in the Gold market as well.